- 0xResearch

- Posts

- ⛓️ CEXs are going onchain

Brought to you by:

Remember the DeFi mullet thesis? Fintech in the front, DeFi in the back. Crypto CEXs are fast making this a reality today.

— Donovan

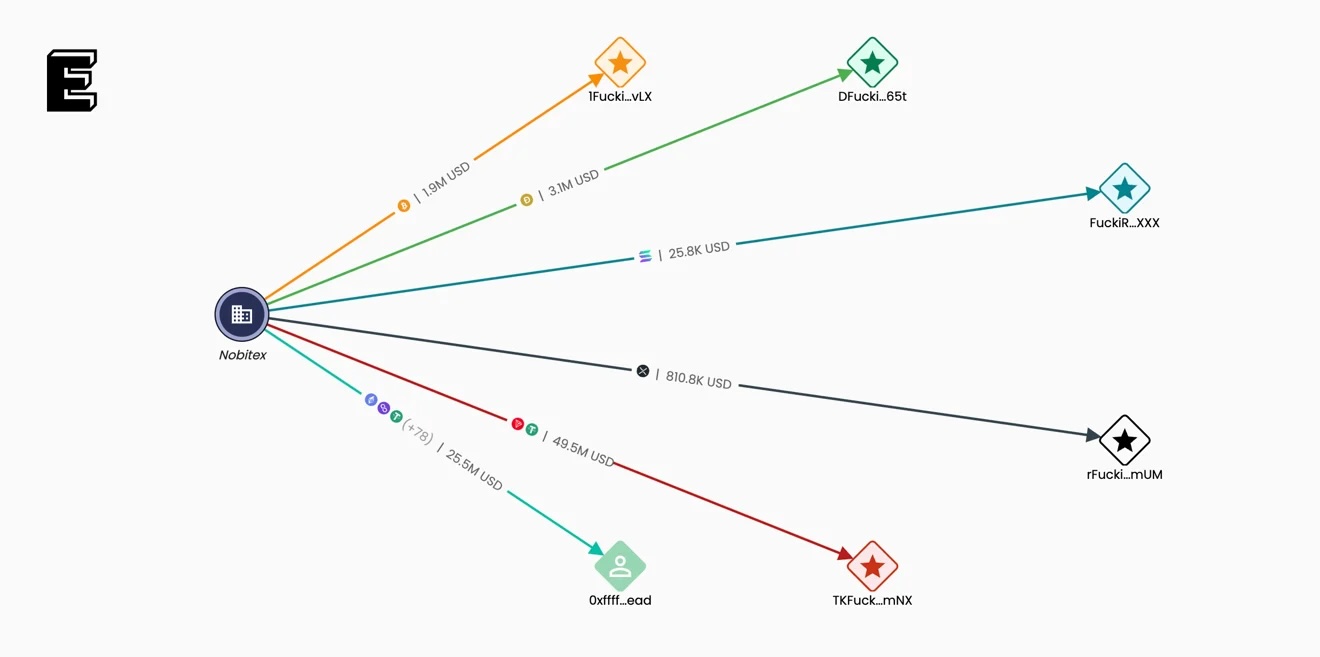

No exit for Nobitex:

Source: Elliptic

In one of the most astonishing exploits in memory, Iranian exchange Nobitex was drained of $81.7M in crypto yesterday. Over $48M in USDT was moved over Tron, but most funds are permanently burned according to Chainalysis and the rest has already been frozen by Tether.

The attackers used vanity addresses such as TKFuckiRGCTerroristsNoBiTEXy2r7mNX, signaling ideological motives. A vanity address is an address that contains a custom, human-readable string (here: “FuckIRGCTerroristsNoBiTEX”). The exchange reportedly has been linked to the IRGC, the Islamic Revolutionary Guard Corps.

But generating such a vanity address while still retaining access to its private key is computationally prohibitive for strings this long. (And it’s not close — we’re talking longer than the length of the universe for a God-tier supercomputer. “Astronomical odds” doesn’t do it justice.)

Thus, the attackers appear to have burned much of the stablecoins. They won’t profit from their efforts.

Elliptic confirms the hack was perpetrated by a pro-Israel group calling itself Gonjeshke Darande, which claimed Nobitex is “vital to the regime’s efforts” and threatened to leak its internal network and source code.

Nobitex’s role in sanctions evasion has long drawn scrutiny, and the exploit underscores the geopolitical risks attached to centralized exchanges in sanctioned jurisdictions.

Brought to you by:

Katana is a DeFi chain built for higher sustainable yield and deep liquidity.

It concentrates liquidity into core applications and channels the chain’s revenue back to the users. Creating a better DeFi experience that benefits the active users on the chain.

Earn KAT tokens: Pre-deposit with turtle club

Enter the DeFi mullet era

Crypto centralized exchanges have been rapidly moving their businesses onchain of late.

And to get there, they’re all leveraging their biggest trump card: distribution.

Case study number one.

Bybit announced Byreal on Sunday, a DEX on Solana that is set to launch later this year. Along with the DEX is also a yield product (Revive Vault) and a token launchpad (Reset Launch).

Byreal will route liquidity from its CEX through a hybrid RFQ (request for quote) + CLMM (concentrated liquidity market maker) model, so onchain users can trade onchain with a CEX’s liquidity depth.

My guess is Bybit users will also be able to access Byreal from the main CEX app.

Case study number two.

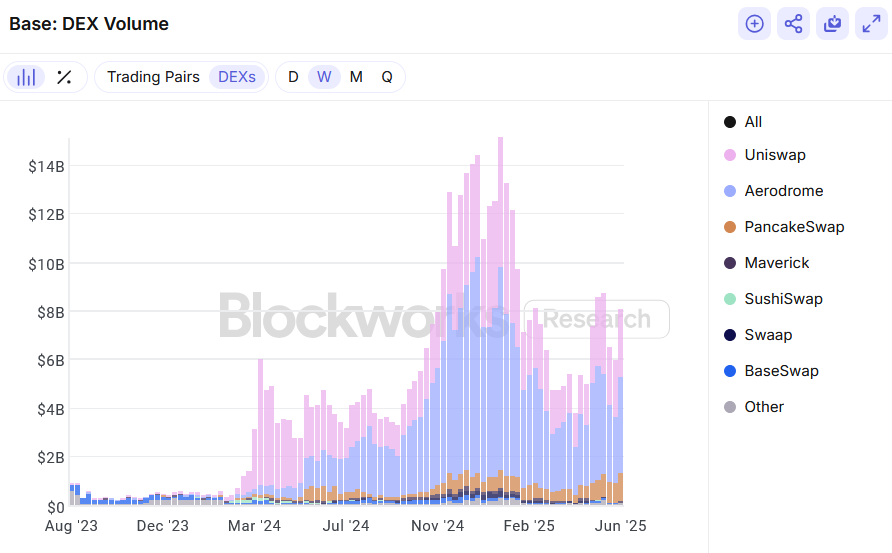

Coinbase announced a few days later the direct integration of Base DEXs onto its exchange business, set to roll out this week. DEXs from other chains will also be integrated eventually.

This opens up gas-less trading access to thousands of altcoins for millions of Coinbase users (though they will still pay the usual CEX trading fee).

It’s a significant tailwind for DEXs on Base, namely its largest one: Aerodrome. The AERO token — which accrues revenues from DEX trading fees — has pumped 52% in price since the announcement.

Source: Blockworks Research

This isn’t Coinbase’s first attempt to push onchain with its distributional advantage. cbBTC, its wrapped bitcoin product was bootstrapped using Coinbase as the main distribution rail.

By integrating Base’s lending markets under the hood, cbBTC holders on Coinbase could easily borrow USDC against their bitcoin collateral without leaving the Coinbase app.

~$100m in bitcoin on @base from @coinbase customers borrowing USDC onchain

this is the first defi mullet product and it's only been a couple months - this flywheel is going to bring billions and billions of capital onchain

— jesse.base.eth (@jessepollak)

3:04 PM • Apr 5, 2025

Case study number three.

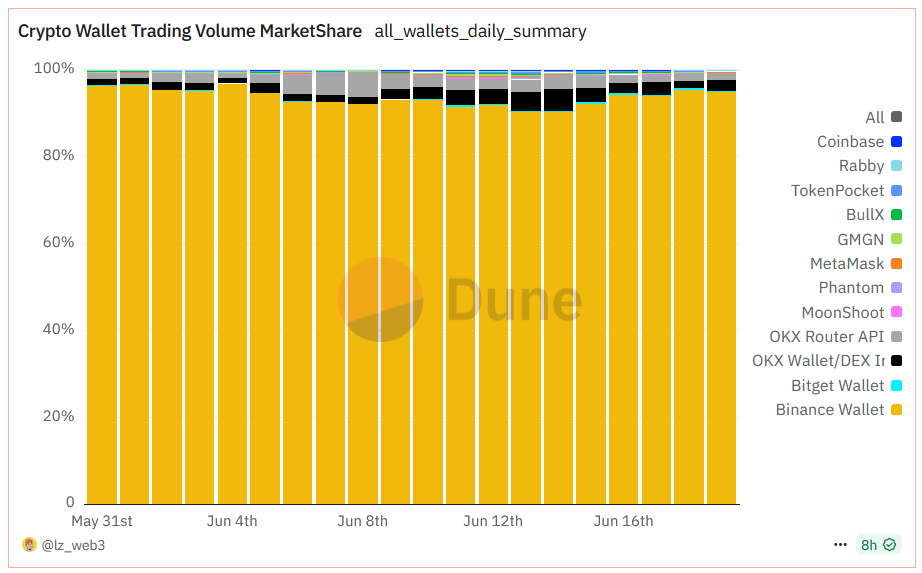

Binance and its extremely complicated Alpha campaign, which has been running since May.

Within Alpha are dozens of “trading competitions” that reward users with “Alpha Points” to trade selected assets, which will in turn entitle you to airdrops. Yet, calling it a competition is misleading — most of these points are handed out based on trading volumes, not P&L criteria.

That’s puzzling until you realize there is a double-pronged strategy at play here.

The first prong is to drive Binance Wallet adoption. Alpha points are eligible only if one trades using its keyless Binance Wallet. This has enabled Binance to absolutely dominate crypto “wallet market share,” as seen below.

Source: Dune

There are two caveats here. For one, the activity isn’t organic.

Second, these aren’t “Binance Wallet” users so much as they are simply “Binance CEX” users.

Traders still pay the Binance CEX trading fee, so the revenue capture is different from that of a MetaMask user paying a fee for using its in-app trading features. Calling it “wallet market share” is probably misleading.

Still, it has allowed Binance to drive adoption for its wallet and potentially funnel users onchain on a piece of infrastructure that they own, which they can monetize later.

The second prong of the strategy behind Binance Alpha is to bolster its own onchain ecosystem on BNB Chain.

Powering the trading of these Alpha tokens under the hood is PancakeSwap, which has exploded in volumes since Alpha kicked off in May.

Source: Blockworks Research

These different strategies convey a clear sign: the onchain economy has come a long way from just a few years ago.

DeFi is now mature and secure enough that centralized entities, which must adhere to regulatory requirements, can confidently integrate DeFi infrastructure into their own compliant technology stacks.

There’s a new way to join the Hype train.

Hyperwave just dropped hwHLP, a liquid token backed by the Hyperliquidity Provider vault (HLP) that lets users earn from market-making and liquidations on Hypercore.

It’s a liquid receipt token that can be further deployed across HyperEVM in DEX LPs or yield strategies.

Intrigued? Let’s take a look:

Hyperwave’s hwHLP provides exposure to trading fees and liquidation revenue generated on Hypercore, Hyperliquid’s central limit order book. Users deposit USDT0 or USDe and receive hwHLP. According to Hyperwave’s limited documentation, hwHLP is intended to enable broader participation in strategies typically reserved for privileged actors on other platforms.

The protocol has published five audit reports covering the core contracts, including reviews by Spearbit, and Code4rena.

But there’s no free lunch. Hyperwave’s product is governed by a modular contract architecture that includes a RolesAuthority module, which controls permissions for key actions such as deposits, withdrawals, upgrades, and token minting. The identities and configuration of the entities controlling these powers have not been publicly disclosed.

Like many projects using the same BoringVault architecture, Hyperwave employs a Safe multisigs for admin control, so there’s some trust involved. Hyperwave uses a 4/7 Multisig with signers from Swell Labs that are “globally distributed and utilize a variety of multisigs to limit systematic risk amongst signers,” according to a spokesperson.

Also, deposits made today are not withdrawable until July 3, and after that come with a 2-day delay like HLP itself. Strategy-wise, the vault is of course also exposed to the same volatility risk: if Hypercore’s PnL turns negative, holders eat the drawdown.

USDT0 and USDe, the input assets, also carry their own peg and systemic risks, though these are relatively minor. Add in oracle and bridge dependencies (RedStone, Pyth, LayerZero), and hwHLP becomes a high-beta stable proxy with execution and governance tail risks.

Tl;dr — hwHLP could be a powerful new primitive on the HyperEVM, but it will take time to develop some Lindy. So, size like a Degen, not a DAO.

— Macauley

Chess clocks ticking, pull-up bars waiting, dunk tank ready — all hosted by the 0xResearch and Blockworks Research teams.

Expect real arguments, fast plays, and a crowd that knows the difference between conviction and cope.

📅 June 24-26 | Brooklyn

|

|