- 0xResearch

- Posts

- 🏦 Onchain fractional reserve banking

🏦 Onchain fractional reserve banking

Enter infiniFi

It’s day one of Permissionless and one of us (Macauley) is on the ground.

The other is looking today at infiniFi, the latest DeFi yield app to try fractional reserve banking onchain.

— Donovan

Blockchain tech altering the global economy is no longer a distant hope. With the market projected to grow almost 600% over the next five years, it’s safe to say the blockchain revolution is well underway.

The latest report from Blockworks Research and OKX shows how blockchain is a new alternative, shifting the landscape for 4 major industries: financial services, technology, consumer goods, and entertainment.

These data-driven insights on the future of blockchain are a must-read for degens and empire builders alike.

Fractional reserve banking onchain

Banks take in deposits to invest a portion in riskier, illiquid assets — that’s how they make money.

This “borrow short, lend long” business model is otherwise known as fractional reserve banking. As long as not every depositor wants their money at once, everyone’s happy!

When crisis mode hits and users rush for the exits, the risk models of banks are put to the test.

At the heart of the problem is non-transparency around a bank’s liabilities and available assets. You could theoretically avoid this problem if that information was visible, as you could curate your own risk models.

Enter infiniFi, a new DeFi protocol on Ethereum that aims to replicate the entire stack of fractional reserve banking onchain.

How it works:

Users deposit stablecoins for iUSD receipt stablecoin.

For lower risk yield, stake iUSD for siUSD. This is liquid.

For higher risk yield, lock up iUSD for liUSD. This is illiquid.

Now the “fractional reserve banking” component comes in.

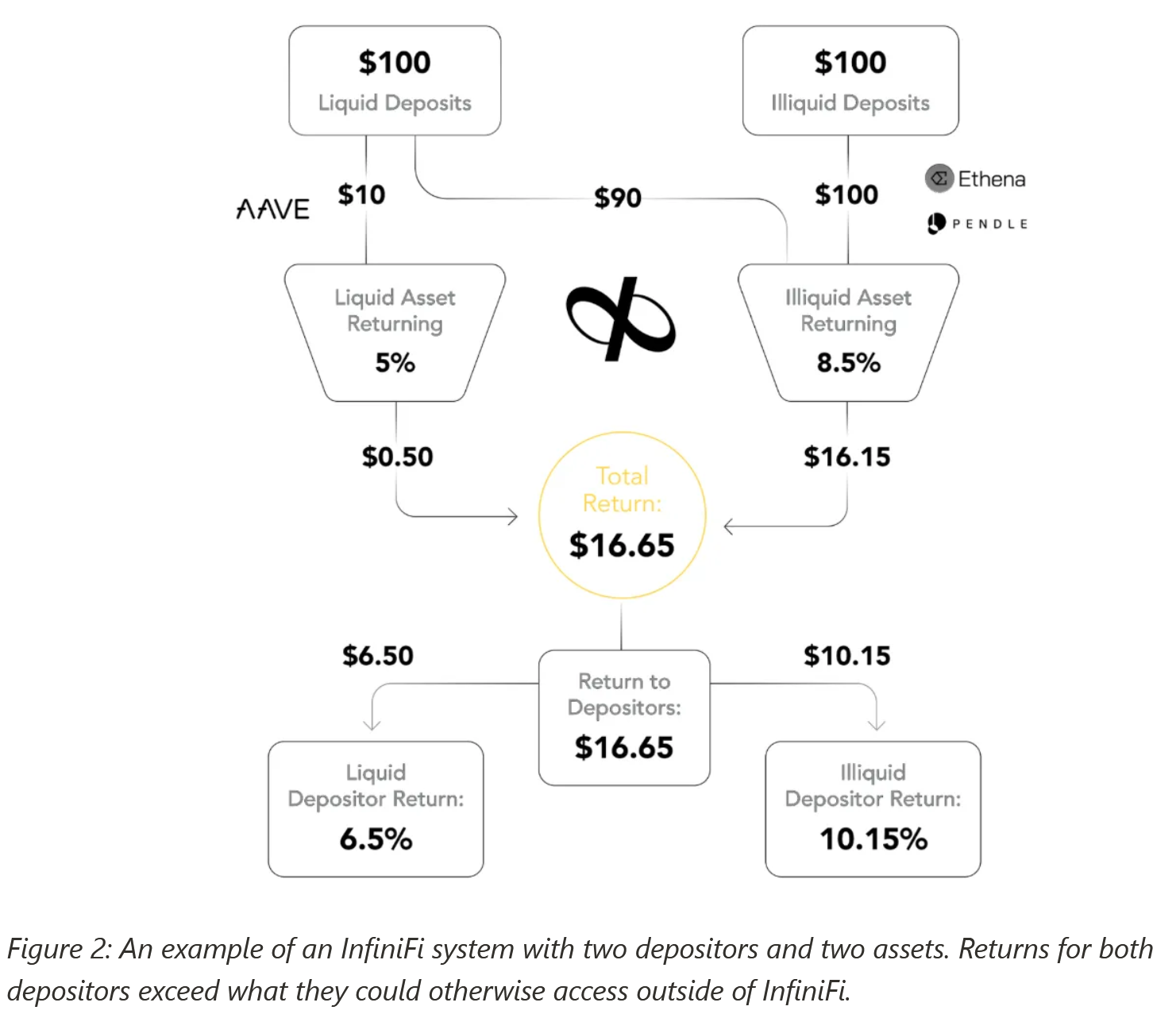

InfiniFi deploys the liUSD liquid tranche capital into lower risk return money markets like Aave or Fluid, while optionally deploying the siUSD illiquid tranche into higher risk return strategies. (Governance will eventually determine these decisions.)

That exact ratio is informed by the demonstrated preferences of depositors and which yield options they select (siUSD vs liUSD).

The positive-sum outcome? InfiniFi gets to distribute amplified yields for both groups of depositors than if they had pursued their strategies individually.

Source: infiniFi

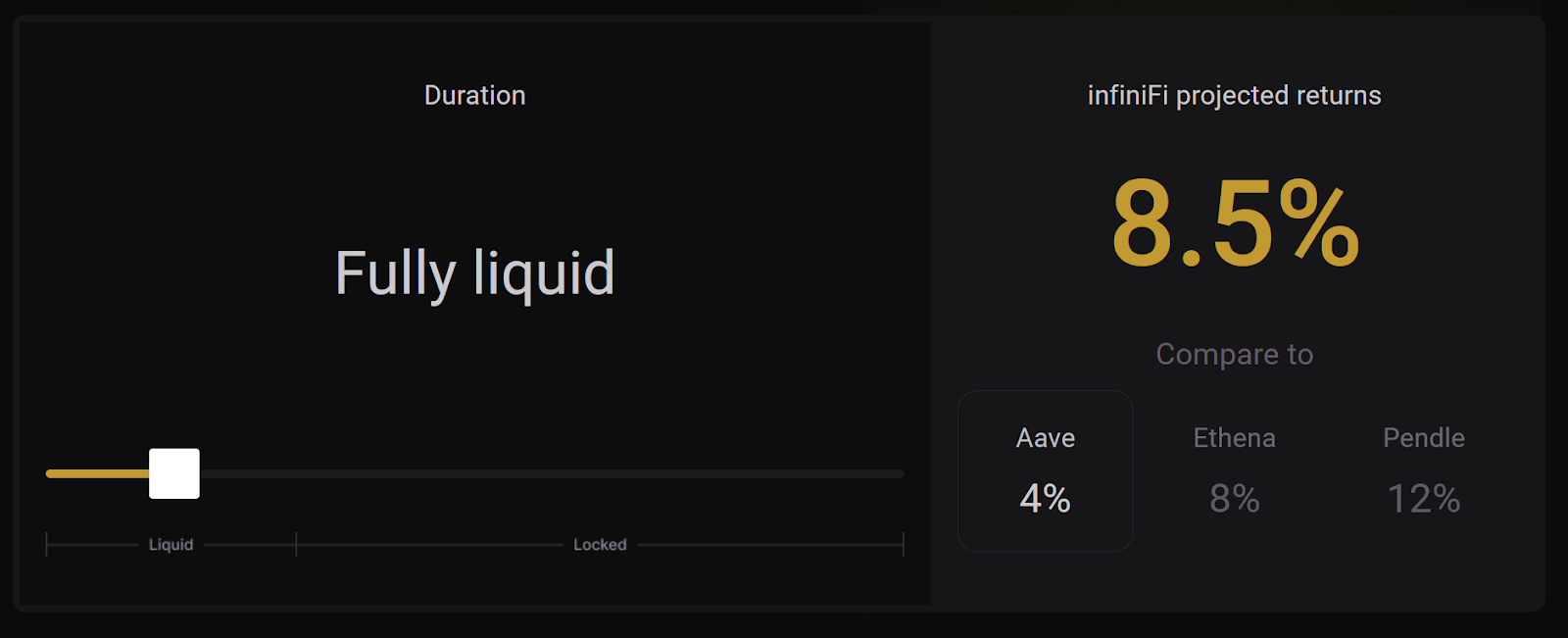

Based on infiniFi’s website, whether you’re opting for a liquid (siUSD) or locked (liUSD) yield, you get a comparatively superior yield than the underlying protocol.

Source: infiniFi

It’s a neat business model.

But what infiniFi is doing in itself — borrowing short and lending long — isn’t all that different from what banks usually do.

The innovation comes from the fact that the entire stack is on the blockchain.

That’s how you, as a user, can sleep easy at night because you know your bank isn’t pulling a Sam Bankman-Fried and pursuing unchecked leverage against the most illiquid assets.

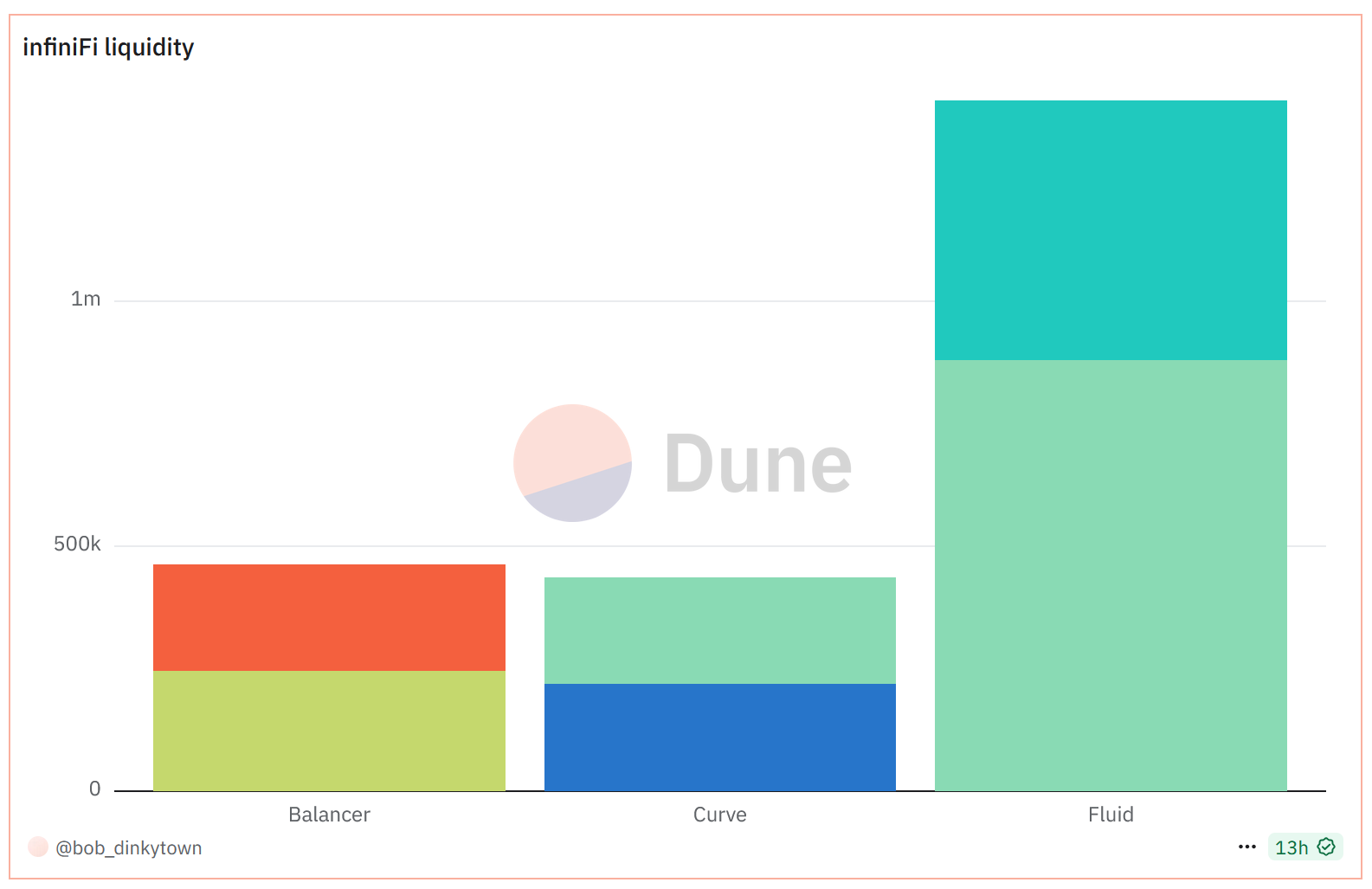

InfiniFi’s reserve composition is completely transparent onchain, so you don’t have to rely on a quarterly call report.

You can easily look up USDC deposits and iUSD tokens minted against it to determine its exact asset-liability mismatch, if any.

You can also examine a breakdown of the protocol’s yield strategies, or whether the protocol is abiding by its liquidity buffers — down to the amount and type of assets they’re made up of.

Source: Dune

In the event of a hack or “bank run,” an explicitly coded loss waterfall will determine who gets paid in order.

The highest-yield and locked liUSD token holders are first in the firing line, absorbing losses first.

SiUSD stakers (lower yield, no lock) are hit only after locked users are wiped. Plain iUSD holders come last.

No one wants to see this happen, but users can at least find some respite in the fact that they won’t have to wait two years like FTX depositors did.

InfiniFi has attracted $33m in TVL and has an ongoing six month points program launched at the start of June.

Are the trenches back?

Dan Smith: From an activity standpoint around volume and revenue for pump.fun, it feels like it’s been pretty consistent. The AMM obviously has accelerated its growth and the bonding curve has been at a homeostasis since late February. So it's like a six-month period now and it’s kind of a new normal. [Pump] is not necessarily “back” — the numbers don't support it being at a new high or new low, really.

Thoughts on X’s development of a Super App?

Ryan Connor: It's very interesting. Messaging is not really a natural place for financial activity; people do not want financial activity within their messaging application — at least historically. It happened for very path dependent reasons for WeChat. I do like the Telegram to TON chain story but there are obviously risks to it, the biggest one being that Telegram doesn’t have users in the wealthiest markets. Telegram is most popular in places where GDP is far less than Western Europe and in the United States, which is the opposite for X, where the audience is very US-centric and Western. It's a little more highbrow and the place where more intellectual or knowledge-based industries tend to have their social conversation and I think that's a much more obvious place to launch financial products than in app messaging.

Live debates. Blitz chess. Pull-up flexing. A dunk tank for bad alpha.

Hosted by the 0xResearch and Blockworks Research teams — plus appearances from Jack Kubinec and Boccaccio.

📍Industry City — Courtyard 7 & 8

📅 June 24-26 | Brooklyn

|

|

Invite. Engage. Reward. 🎁

The 0xResearch referral program lets you pocket the perks when you send others our way. Don’t miss out on your chance to win:

🎟️ 5 referrals: One FREE Permissionless IV ticket