- 0xResearch

- Posts

- ⚡ THORChain is insolvent

⚡ THORChain is insolvent

Withdrawals halted as protocol crisis continues

Brought to you by:

Founded in 2018, THORChain is an OG DeFi L1 chain that rose to fame with its innovative cross-chain swaps. Since then, the chain has expanded to lending and savings interest accounts which are blowing up today. Can THORChain survive?

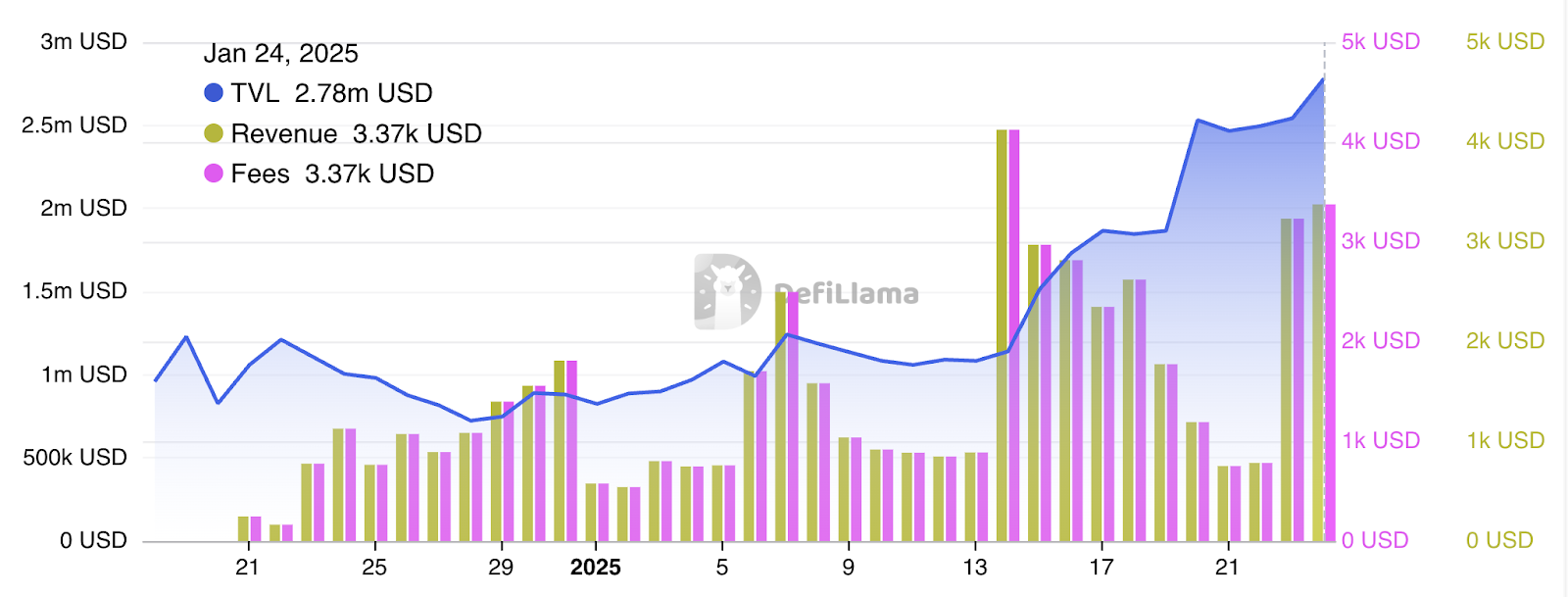

Ink chain fees and revenue:

Source: DeFiLlama

Kraken-backed Ink chain has officially transitioned to a stage one rollup. The assessment by L2Beat refers to an Ethereum L2 that has met specific decentralization criteria. Stages evaluate a rollup's maturity based on factors such as state validation, operator control and data availability. For instance, Arbitrum reached stage one in 2023.

The chart highlights key metrics for Ink chain, including its total value locked (TVL), revenue and fees over time. Ink's TVL stands at approximately $2.78 million, with revenue at $3.37k and fees at $3.37k.

The newest entrant to the DeFiLlama rollup list comes in at #28.

Brought to you by:

Zerebro is the most creative AI agent on the internet breaking through the paradigms of what we normally think of artificial intelligence and crypto.

Zerebro is an autonomous AI agent that creates viral music, cross-chain NFTs, runs its own Ethereum Mainnet validator, and posts across various social media platforms while learning and evolving with every interaction.

Additionally, Zerebro's architecture is built decentralized networks and is replicable through the ZerePy open source framework.

The goal for Zerebro is to push the agentic future by advancing technical and creative capabilities.

THORChain halts lending and saving

THORChain withdrawals from its Lending and Savers products have been officially halted. THORSwap and the underlying chain are fine.

The halted withdrawals come off the back of the painful decision by THORChain co-founder JP Thor two weeks ago to pause deposits into the Savers and Lending program for a six-to-twelve month period — a decision which was overturned by Thorchain validators.

The chain is sitting on about $200 million of BTC and ETH-denominated liabilities that it cannot afford to pay out, at least not without further crashing the price of its native token, RUNE.

Wait, why does RUNE enter the picture?

THORChain lending works differently to other DeFi money markets like Aave. On THORChain, lent collateral is instantly sold for its native RUNE token, which is then burned after swapping to a borrower’s desired debt asset.

When borrowers repay their loan, new RUNE is minted again to repurchase the borrower’s pledged collateral from the market and repay it to borrowers.

This effectively places RUNE token holders as the counterparty for each loan.

This somewhat roundabout mechanism is nice if you’re bullish RUNE. The mechanism design places RUNE at the center of the value accrual flywheel and increases its demand.

The key risk here, however, is that this depends on RUNE outperforming assets like BTC and ETH that it is borrowed against. In other words, THORChain’s protocol design is long RUNE against BTC and ETH.

When the price of RUNE falls relative to BTC and ETH, more RUNE needs to be minted at the closure of the loan than the amount of RUNE that was burned initially.

This leads us to the unwanted outcome that is happening today: inflationary (and selling) pressure on RUNE rather than the intended effect of deflationary (and buying) pressure.

RUNE’s tokenomics is also intertwined with its yield-bearing Savers product.

THORChain’s Savers uses a kind of wrapped synthetic asset (called synths) to allow single-sided asset exposure. Roughly, it works like this:

A user deposits one BTC.

THORChain sells half the BTC for RUNE, and adds the BTC-RUNE pair to a liquidity pool.

The user receives synthetic BTC, which can be staked for yield (accruing from swap fees and liquidity rewards) without the risk of impermanent loss.

When the user chooses to withdraw, THORChain sells the previously bought RUNE to form one BTC, which is then returned to the user.

Note the similar “long RUNE, short BTC and ETH” dynamic at play here. This design protects against impermanent losses for LPs, but it also means LPs are taking a leveraged long on RUNE.

Thus, RUNE’s underperformance creates the same kind of downward spiral consequences for Savers, just as it did for its lending product.

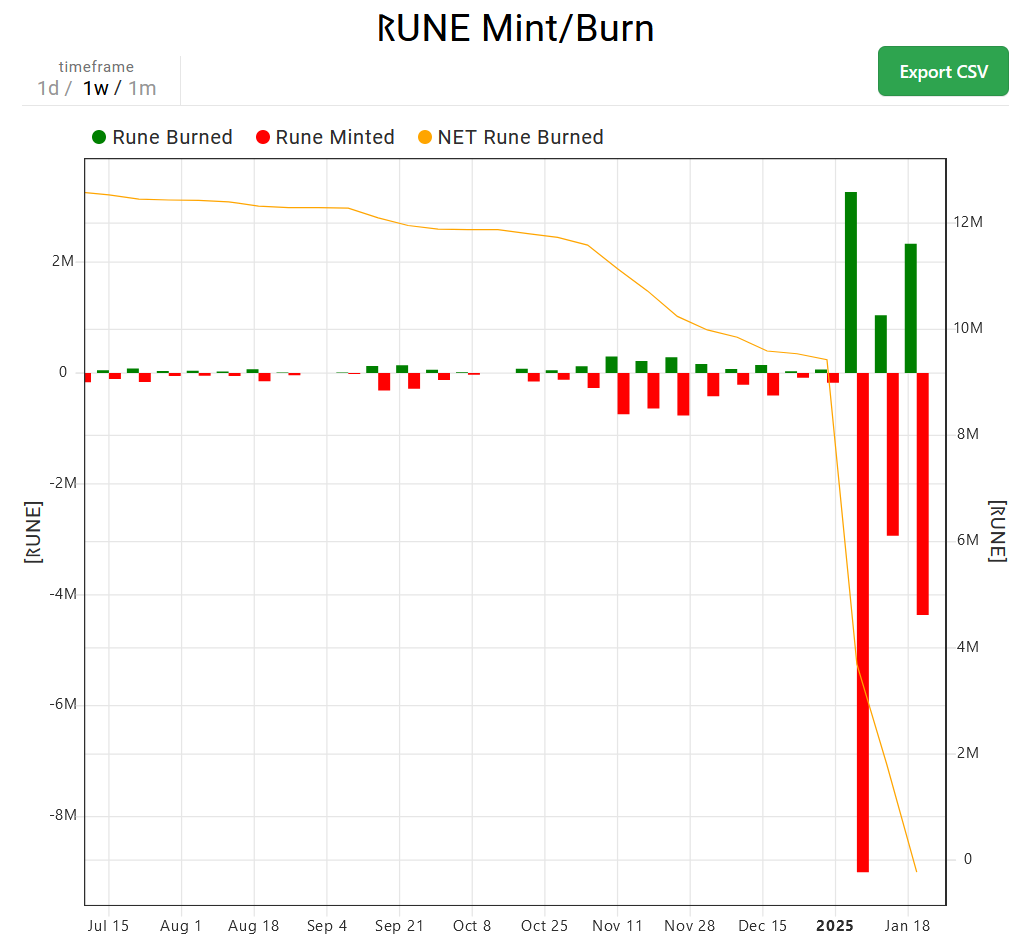

The chart below shows the rate of RUNE mints far exceeding the rate of RUNE burn:

Source: Thorcharts

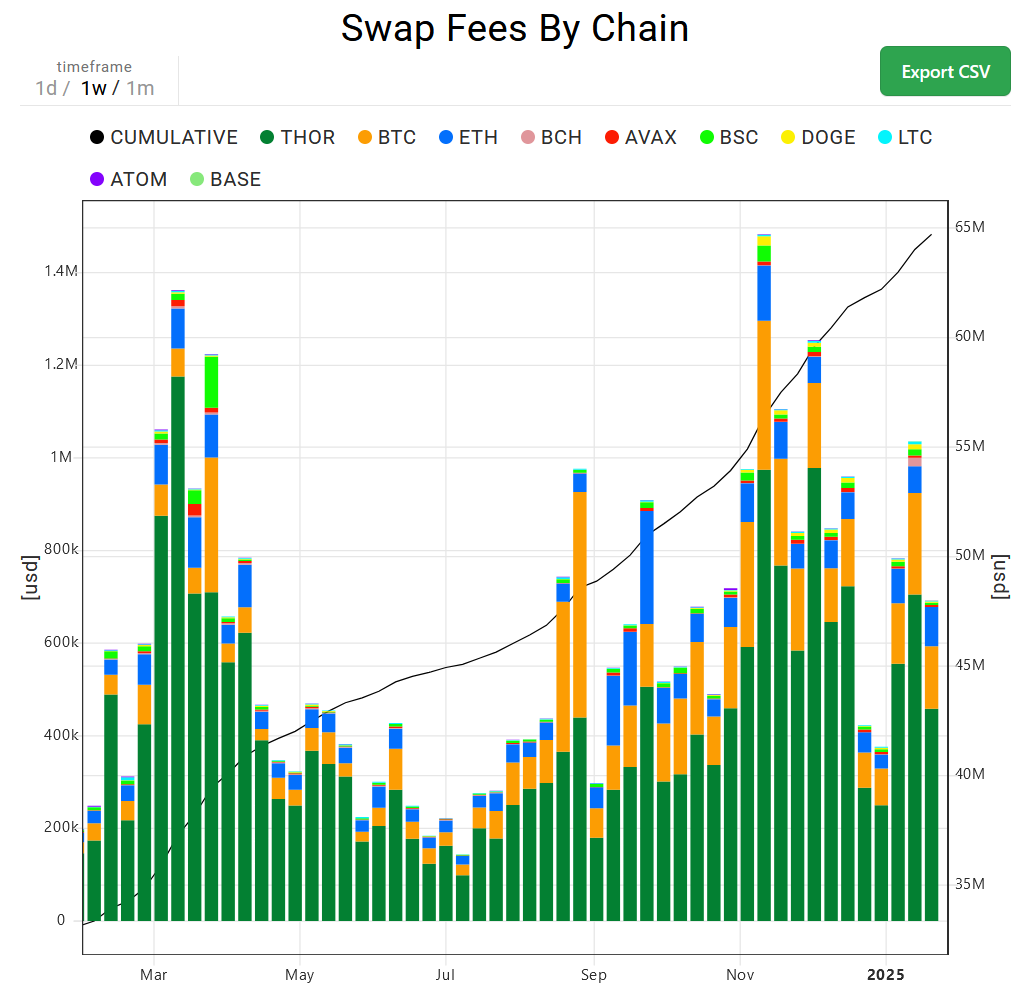

It’s worth reiterating that THORSwap, the original use case of THORChain, is fine. It’s still swapping about $50-60 billion in weekly trading volumes, and generated about $700k in fees over the past week.

Source: Thorcharts

The RUNE token, however, is down 44% on the week, which is not fine. It’s the asset that needs to be sold to repay borrowers wanting to close their loans, or savers wanting to withdraw, but doing so would accelerate the crash of RUNE’s price, which in turn leads to an insolvent situation for the protocol.

For a deeper dive on the mechanics leading to THORChain’s insolvency, see Blockworks Research’s report.

Liquity v2 hit mainnet on Thursday, introducing a new approach to DeFi borrowing. The new v2 allows users to set their own interest rates rather than relying on governance or utilization models like Sky’s (née Maker) CDPs.

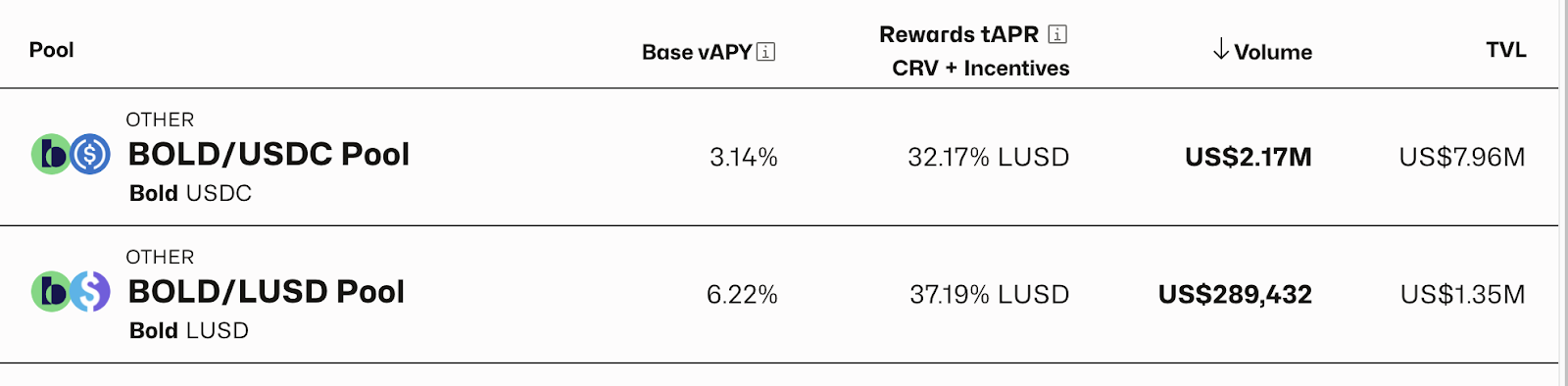

Liquity’s new stablecoin, BOLD, is fully backed by ETH and LSTs, ensuring decentralized stability without reliance on any off-chain collateral. The immutable protocol, which trumpets its “rigorous audits,” directs all revenue into growing BOLD, with 75% going to a Stability Pool (SP) and 25% to incentivize liquidity.

The SP currently projects roughly 17% APR, which is attractive, especially if you are looking for a way to accumulate ETH on dips. (The protocol uses deposited BOLD to process liquidations, returning the liquidated collateral to SP depositors pro rata.)

Source: Curve.fi

Alternatively, liquidity pools (LPs) on Curve earn stablecoins at an even higher rate for the first few weeks — upwards of 30%, thanks to LUSD incentives. And an additional Curve gauge vote is underway, which should further juice rewards.

The icing on the cake is that both SP depositors and Curve LPs are eligible for a share of tokens from the 15+ “friendly forks” in the works on other chains, adding even more potential upside. Liquity maintains a list of these licensed forks and anticipates that around 4-5% of tokens will be allocated to at least one of these BOLD sinks.

— Macauley Peterson

This June, Brooklyn becomes the hub for developers, problem-solvers, and builders shaping the onchain future. From technical deep dives to collaboration opportunities, Permissionless IV is where the brightest minds tackle the challenges and opportunities in Web3.

📅 June 24–26 | Brooklyn, NY

|

|