- 0xResearch

- Posts

- The Price of Trust

Hi all, happy Tuesday!

US equity markets opened the week with a modest bid on Monday, but crypto breadth did not follow.

Today, we also revisit the Kelp-Aave situation one week later, not just from a recovery standpoint, but from what it may reveal about trust in DeFi.

US stocks were treading water near all-time highs and continue to shrug off the protracted stalemate in US-Iran ceasefire negotiations.

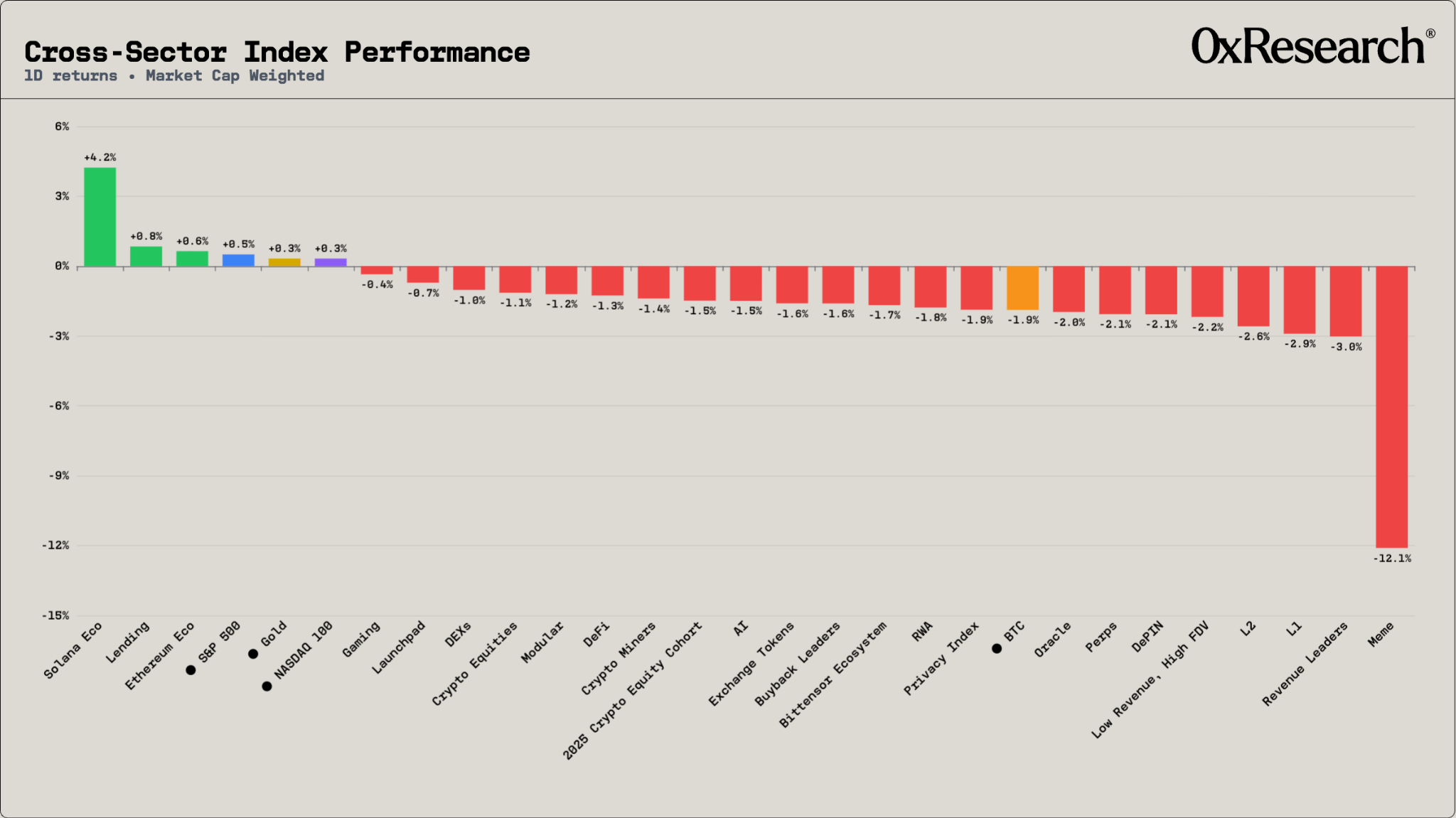

The S&P 500 closed Monday at +0.5%, with the Nasdaq (+0.3%) and gold (+0.3%) eking out similarly modest gains. Bitcoin diverged the other way, finishing -1.9% and underperforming both benchmarks for the second straight session. The broader crypto tape was almost entirely red with one notable exception — Solana Eco (+4.2%). Otherwise, the only sectors above water were Lending (+0.8%) and Ethereum Eco (+0.6%).

Everything else from L1s (-2.9%) to L2s (-2.6%) to Revenue Leaders (-3.0%) closed lower.

Memes were the carnage of the day, collapsing -12.1% — the worst drawdown on the board by a wide margin and a clear signal that the speculative tail of the market got flushed.

The Solana Eco outperformance was, as is often the case, narrowly concentrated. ORCA was the standout component, ripping from roughly -10% in the morning session to an intraday peak near +50% shortly after 14:00 UTC before consolidating around +15% by the close.

The whipsaw action from the Solana DEX token was largely driven by a spike in trading on the Korean exchange Upbit. ORCA has seen similar moves in the past, and they tend to mean-revert over the next few trading sessions, which explains why we see perpetual futures funding rates on ORCA plunging below -1,000% across trading venues.

JUP (+6.0%) and META (+3.7%) also contributed, while the rest of the basket closed flat to modestly down, meaning the sector-level +4.2% print was effectively a one-trick cetacean.

SOL itself has remained range-bound between about $78 and $90 since early February.

A persistence of strength in lending over the past week is worth flagging. The post-rsETH cleanup is continuing apace. Last Monday's note covered the rate dislocations following the KelpDAO / LayerZero exploit, and while elevated utilization hasn't fully normalized, the situation on Aave’s Core Instance on Ethereum is much improved, as both USDT and USDC supply rates have fallen to the 4-5% range with 8-figures of available liquidity.

Speaking of interest rates, the FOMC’s April policy meeting gets underway today in Washington. The market expects no change in the Fed funds rate, putting attention squarely on Jerome Powell’s final press conference as Fed chair tomorrow.

The Price of Trust

A week after the Kelp exploit, it increasingly looks like Aave depositors will be made whole. Contributions from Arbitrum (~30k ETH freeze), Mantle (30k ETH credit facility), Consensys and Joseph Lubin (30k ETH), the Aave DAO (25k ETH proposal), EtherFi (5k ETH), and Stani Kulechov (5k ETH), among others, have come together to backstop losses and restore confidence.

Objectively, this is the best outcome for users.

But it also raises an uncomfortable question around incentives. If users are made whole after large-scale failures, the losses are not eliminated — they are simply absorbed elsewhere. In this case, private actors are stepping in to absorb the loss.

From Aave’s perspective, the proposed 25k ETH contribution is meaningful. It represents almost 60% of its treasury (excluding AAVE) and roughly the equivalent of the past two quarters of revenue. The proposal goes to a vote today, which runs through May 1.

The immediate goal is clear: make users whole. The harder question is what happens after.

Looking at flows, Sunday marked the first day of net positive inflows into Aave (+$39M) since the exploit. But zooming out, the protocol still saw about $16.9B in net outflows from April 18 to April 25, with 38% of its deposit base withdrawn in just eight days.

Few protocols have benefited from the debacle as much as SparkLend, which saw over $2.4B in net deposit inflows over the same period. Spark has historically operated with a more conservative risk framework, delisting rsETH in January and enforcing rate-limited supply and borrow caps that constrain how quickly exposure can scale.

For Aave, it remains to be seen whether making users whole is enough to earn back trust. The real challenge now is whether it can retain its position as the dominant liquidity venue over the coming months.

It’s not just Aave that has been affected. We’re already seeing second-order effects across DeFi.

Ethena’s USDe saw $1.84B in redemptions last week, the second-largest weekly decline in its history. Supply now sits at $3.76B, its lowest level since November 2024. The main driver was that sUSDe loopers were pushed into unprofitable positions as borrow costs spiked well above their yield.

Similarly, EtherFi’s eETH has seen ~$300M in net outflows over the past seven days. Over the same period, the share of eETH supply wrapped as weETH (to be used across DeFi) has dropped from 95% to 87%, the lowest share since December 2024. That suggests users may be unwinding collateralized positions and reducing DeFi exposure.

If the initial shock was about bad debt, the second-order effect is about confidence.

And confidence, unlike liquidity, may be much harder to rebuild.

— Carlos

a16z crypto argues that stablecoins are increasingly becoming local payment infrastructure, not just cross-border dollar rails. The piece says regulation has accelerated adoption (the GENIUS Act in the US and MiCA in Europe), while data shows stablecoin commerce is broadening beyond trading into real payments, with rising merchant/card activity, higher velocity, and an estimated $350-550B of stablecoin payments last year. It also highlights that payment flows are becoming more domestic, not less: intra-country transactions have grown from about half of payment volume in early 2024 to nearly three-quarters by early 2026, while local-currency stablecoins like BRLA are gaining traction through integrations such as Brazil’s PIX. The takeaway is that stablecoins are still global by design but increasingly local in practice, evolving into general-purpose payment rails rather than just remittance or FX tools.

Joe Cho from Blockworks published a report on PreStocks arguing that tokenized pre-IPO equities are gaining traction, with PreStocks emerging as a leading Solana venue for continuous retail access to names like SpaceX, OpenAI, Anthropic, and Neuralink. The report highlights roughly $890M in cumulative volume and 1.9M trades since launch and argues that the platform is increasingly functioning as a real-time price discovery venue for these assets. At the same time, it notes that thin liquidity and a slow redemption process can create sizable premiums to offchain secondary marks, leaving the product with meaningful structural and liquidity risk.

Aerodrome Finance is the dominant DEX on Base. Launched in August 2023 by Dromos Labs, the protocol was designed from inception to serve as Base's primary liquidity layer. Its product suite spans a constant-product AMM for stable and volatile asset pairs, and Slipstream, a concentrated liquidity module closely derived from Uniswap V3 that allows LPs to deploy capital within defined price ranges for improved capital efficiency.

Aerodrome holds ~$240M in TVL, with cumulative fees since launch exceeding $322M.

The protocol is preparing a major architectural upgrade, Aero/MetaDEX03, targeting a Q2 2026 launch that will merge Aerodrome and Velodrome into a unified cross-chain DEX and introduce MEV internalization as a new revenue stream.