- 0xResearch

- Posts

- TAO under pressure

TAO under pressure

Plus, Western Union’s stablecoin bet explained

Sam Schubert & Kunal Doshi

April 10, 2026

Hi, everyone. The spotlight today was on Bittensor, where TAO saw a sharp drawdown amid a growing dispute over governance and control within the ecosystem. What started as internal friction has quickly evolved into a broader debate around decentralization, and markets are reacting accordingly.

In parallel, Western Union is making a push into stablecoins, a move that could reshape how legacy payment networks plug into crypto. We break down both stories below.

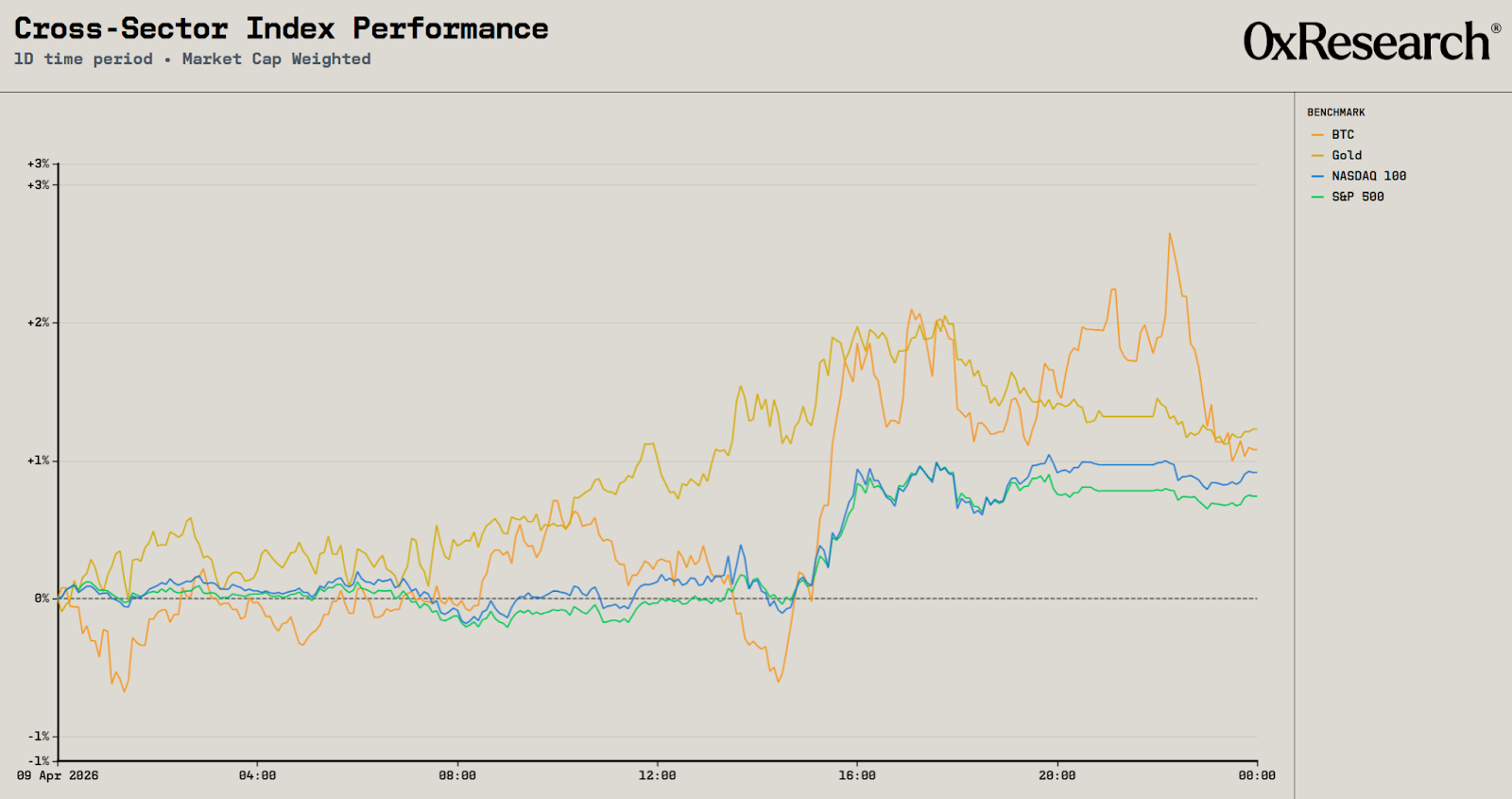

It was a strong day across markets, with all four major benchmarks ending in the green. Gains were led by gold and BTC, up 1.23% and 1.08%, respectively, followed by the tech-heavy Nasdaq and S&P 500, which rose 0.91% and 0.74%.

Despite the positive price action, macro uncertainty remains elevated. The two-week ceasefire is already showing signs of strain, as Israel continues strikes in Lebanon and Iran warns that the agreement could collapse if tensions escalate further. Shipping activity through the Strait of Hormuz remains constrained, keeping crude oil prices elevated near the $100 mark.

Fed minutes from the March meeting added to the uncertainty. A growing number of policymakers signalled that rate hikes may still be required to combat inflation, particularly if energy prices remain high due to the conflict. At the same time, others maintained that a prolonged conflict could weigh on growth enough to justify rate cuts. The result is a market still grappling with a highly uncertain policy path.

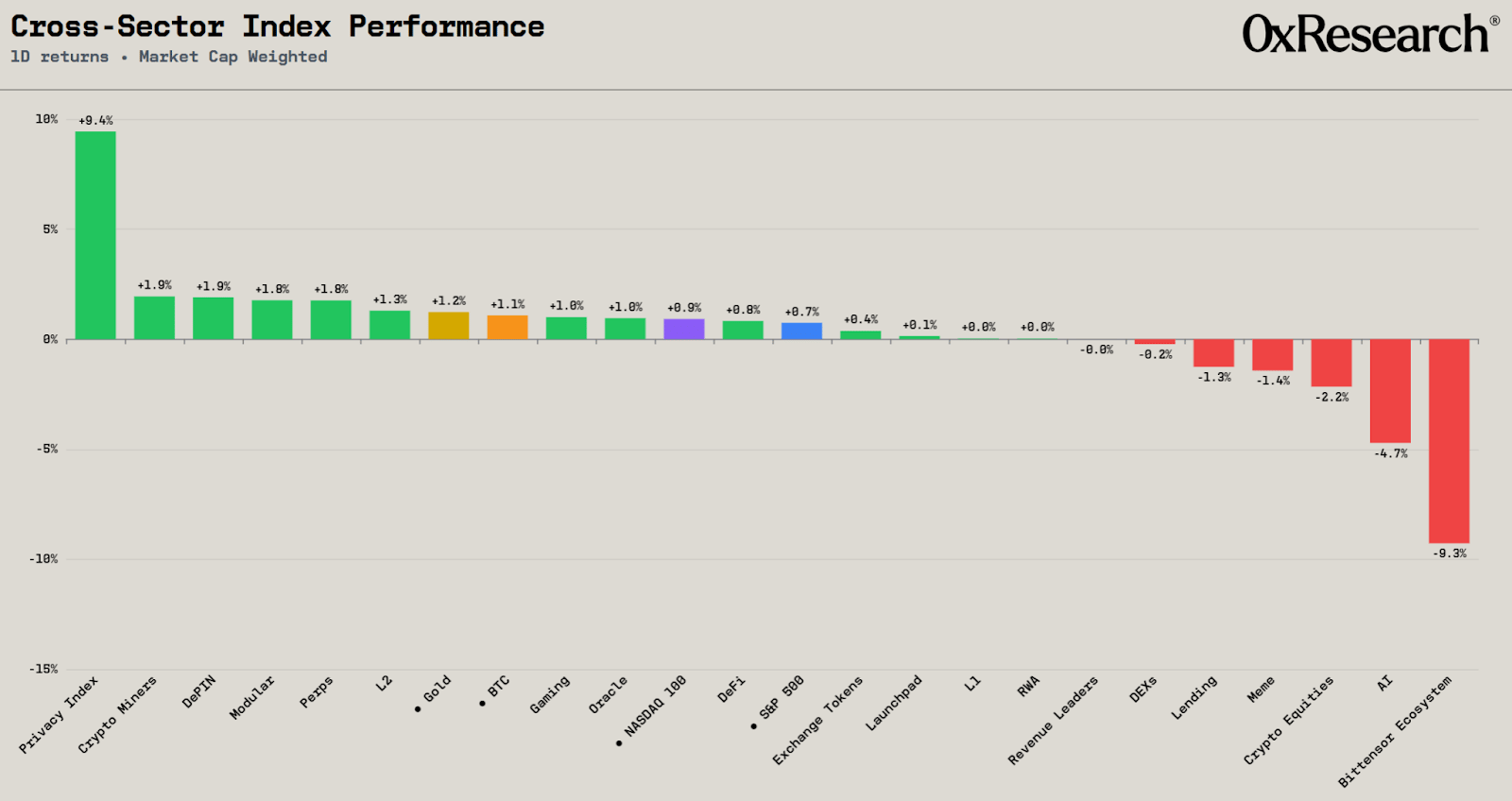

On the sector front, Privacy led the market, up 9.4% on the day. This was largely driven by ZEC, which surged 14% and accounts for 35% of the index.

The move appears to be driven by a short squeeze, with sustained negative funding indicating crowded short positioning. Funding rates for ZEC remain deeply negative at −48% annualized on Hyperliquid, suggesting the squeeze could extend if market strength continues.

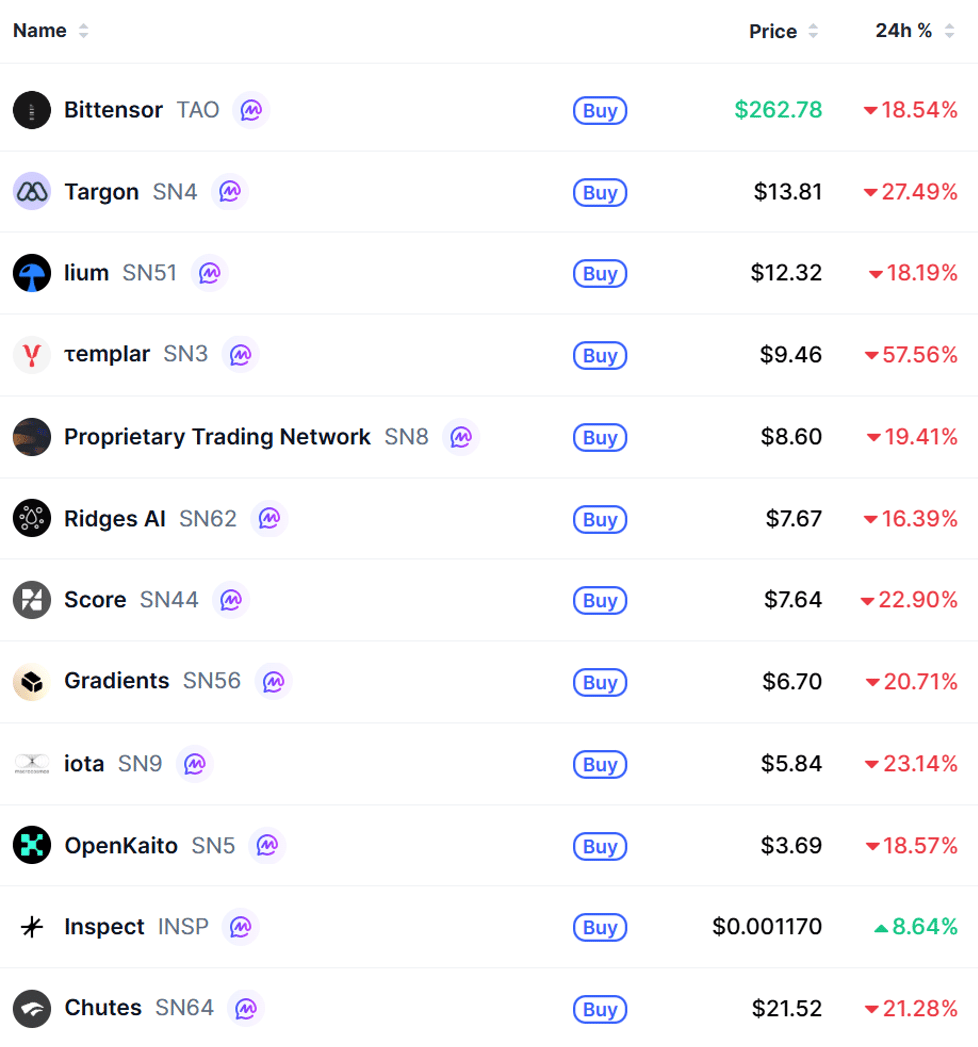

Among the laggards, AI and the Bittensor Ecosystem were down −4.7% and −9.3%, respectively. TAO fell −18.3% over the last 24 hours following internal conflicts within the ecosystem.

The drawdown comes amid a public fallout between Covenant AI, one of the largest contributors to decentralized AI training on Bittensor, and the network’s core leadership. Covenant AI announced its departure, citing concerns around centralization. They pointed to actions such as suspending subnet emissions, deprecating infrastructure, and influencing market dynamics as evidence that control remains concentrated rather than distributed.

These claims were met with pushback from other ecosystem participants, who defended leadership and highlighted the support historically provided to subnet teams. The situation has since evolved into a broader debate around governance, control, and whether Bittensor’s current structure aligns with its decentralization narrative.

While it’s still early to determine the long-term impact, the episode has clearly dented confidence in the ecosystem, and that is now being reflected in price action across TAO and related subnet tokens.

— Kunal

Western Union’s stablecoin bet

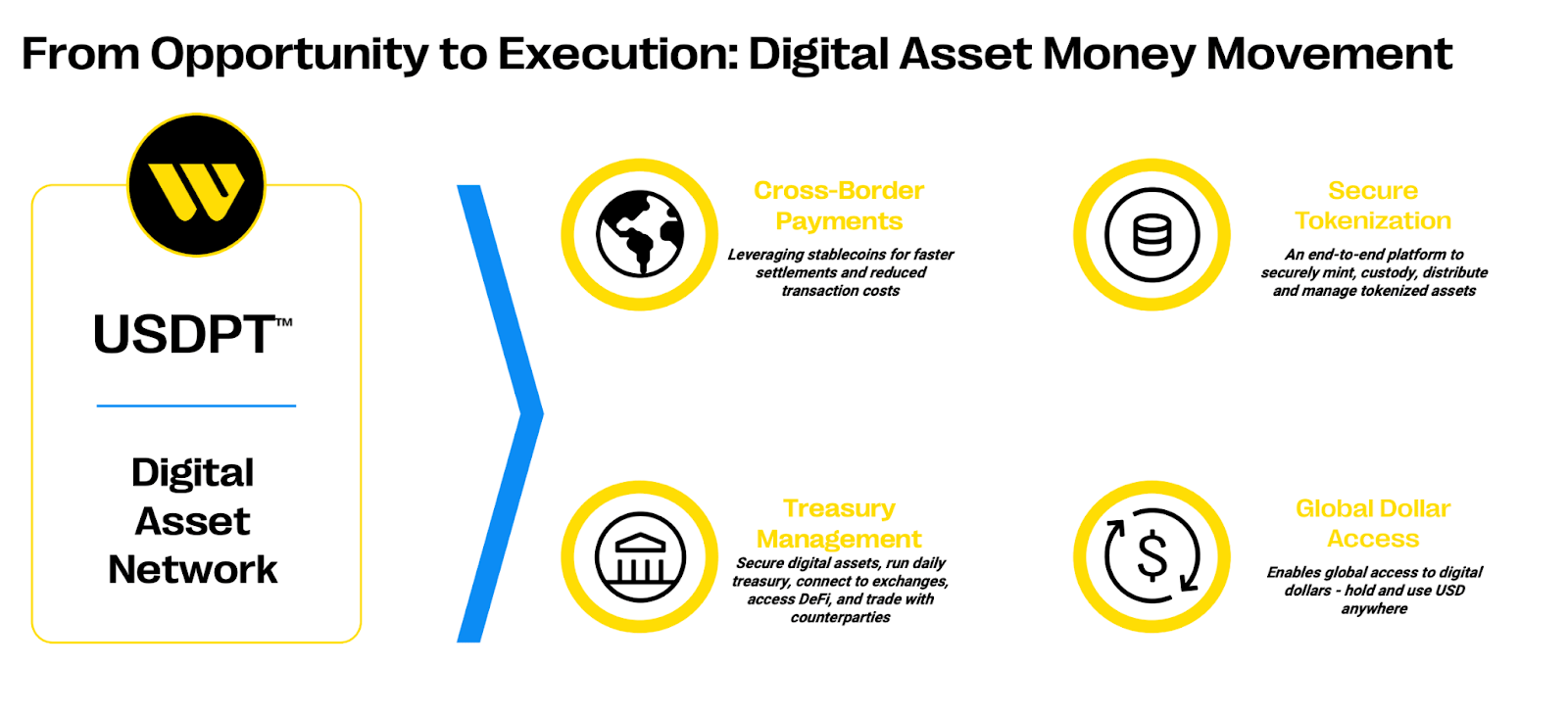

Western Union (WU) announced USDPT, a dollar-pegged stablecoin built on Solana and issued through Anchorage Digital Bank, anticipated by summer. The stock trades at ~5x earnings with a 10%+ dividend yield. The market is pricing this as more of a value trap, but it is potentially one of the most interesting distribution-meets-crypto setups in payments.

WU moves money cross-border for consumers, primarily migrant workers sending remittances home. A sender walks into one of WU’s hundreds of thousands of agent locations (or uses the app), pays a fee plus an FX spread, and the recipient collects cash or receives a deposit on the other end. Revenue was $4.05B in FY2025 across ~300 million transactions in 200+ countries.

The top line has declined 3% to 4% annually as the business transitions away from legacy retail toward digital and adjacent services, but adjusted EPS has held flat at ~$1.75 for three years; WU has been cutting costs faster than revenue falls.

USDPT could make WU’s $3.45B of settlement balances more productive. Today, those balances are held primarily for liquidity and payout readiness. Under the GENIUS Act, stablecoin reserves must be backed by cash and similarly liquid assets, including short-dated Treasurys.

Stablecoins can lower the cost of moving money across borders, but they do not solve the “last mile” problem. Someone still needs to handle compliance across 200+ countries, convert between fiat and digital, and get cash into the hands of recipients in emerging markets. WU already does all of that through hundreds of thousands of retail locations globally. Few companies have a comparable physical payout network, and building one from scratch would cost billions and take years.

Recent GENIUS Act rulemaking is likely a net positive for WU. It raises the compliance burden around stablecoins, which may slow rollout at the margin, but it also increases the value of WU’s existing compliance, distribution, and cash-out infrastructure. Because USDPT is being issued through Anchorage Digital Bank, WU gets exposure to stablecoin economics through a federally regulated structure, while its Digital Asset Network should become more valuable as wallets and platforms seek compliant fiat off-ramps.

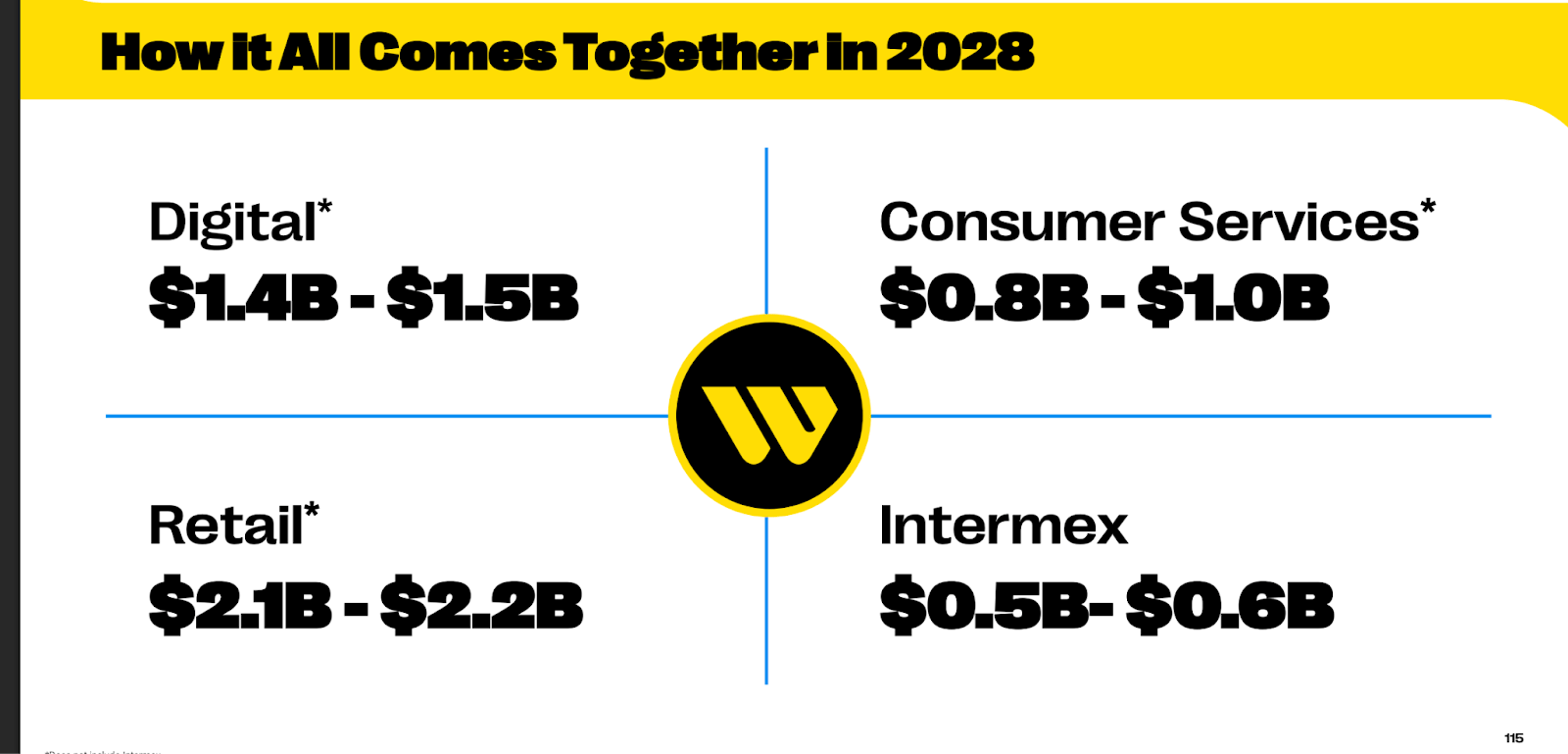

Beneath the crypto angle, the core business is bifurcating. Digital transactions grew 13% in Q4 2025 and now represent 39% of consumer money transfer volume. Consumer Services hit $543M in FY2025 revenue, growing 26% adjusted. The $500M Intermex acquisition (closing Q2 2026) adds 6 million LatAm-focused customers who become immediate targets for digital cross-sell and eventually USDPT.

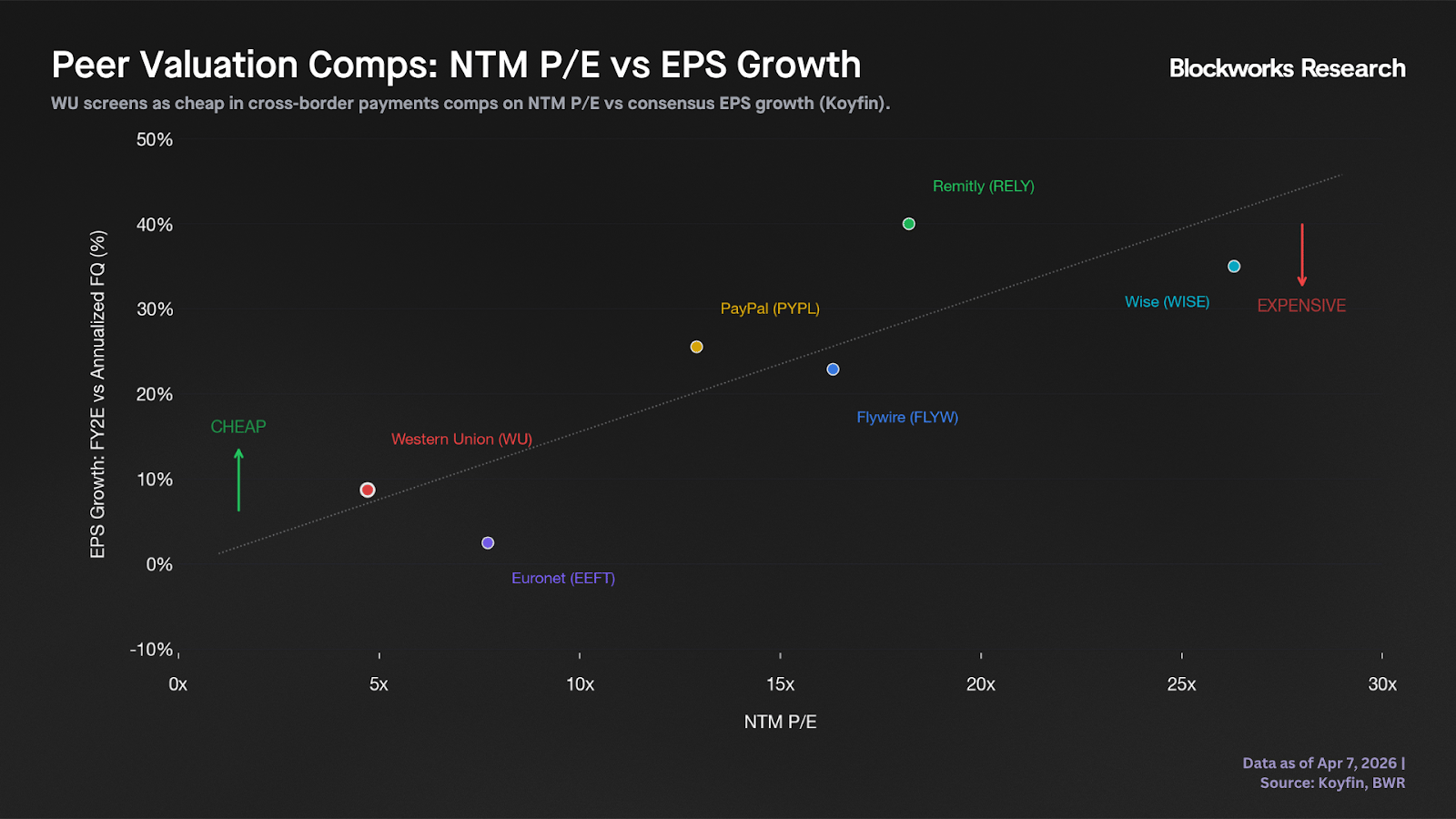

Revenue has been declining for three years, which is why the stock trades at <5x PE. But if the new growth segments and digital-asset infrastructure collectively bend the top line back toward growth, WU stops being a dividend play and starts looking more like a digital-payments infrastructure company. Peers in the space trade can trade well above 10x. Even a modest re-rate coupled with EPS growth presents meaningful upside from here.

— Sam

Lucas Bruder, founder and CEO of Jito Labs, argues that “MEV” as a term is functionally useless and should be retired in favor of Transaction Ordering Value (TOV). The piece traces the acronym’s drift from “miner extractable value” in the proof-of-work era to the catch-all “maximal extractable value,” a category error that conflates benign arbitrage with malicious extraction like sandwich attacks.

Bruder’s core claim: Blockspace is a finite resource, and base fees, priority fees, and tips are the market clearing itself, not distortions. On Solana specifically, the absence of a public mempool, private transaction routing, Jito’s Block Assembly Marketplace with trusted execution environments, and multiple concurrent proposers have curtailed predatory strategies to a small fraction of blockspace activity. He frames the remaining discourse as antiquated, calling out speakers at the recent Digital Assets Summit who cited MEV as evidence that permissionless chains can’t support traditional financial instruments.

The report argues that adding leverage to prediction markets is a meaningful but structurally complex opportunity, where success depends less on demand and more on market design and risk management. It outlines four main models — lending pools, venue native margin, synthetic desks, and perps — each with different tradeoffs in how they handle liquidation, pricing, and capital sourcing.

While the revenue potential is real, with base-case estimates around $15M annually and driven mostly by financing income, the core constraint is not user demand but fragile market microstructure, including jump risk, liquidity gaps, and unreliable pricing during stress. The key conclusion is that leverage will emerge, but scaling it requires fixing venue architecture itself rather than layering financial engineering on top of flawed market structures.

Introducing Blockworks Investor Relations, an IR platform built for onchain businesses.

The latest Blockworks offering brings together analytics, a branded investor relations site, and integrated advisory support into a single platform. The result is a more efficient way to share your story, build trust with investors, and engage a global audience from day one.

Check out our cofounder Michael Ippolito's keynote at DAS NYC launching the new IR platform.