- 0xResearch

- Posts

- Sky's Quiet Climb

Hi all, happy Tuesday!

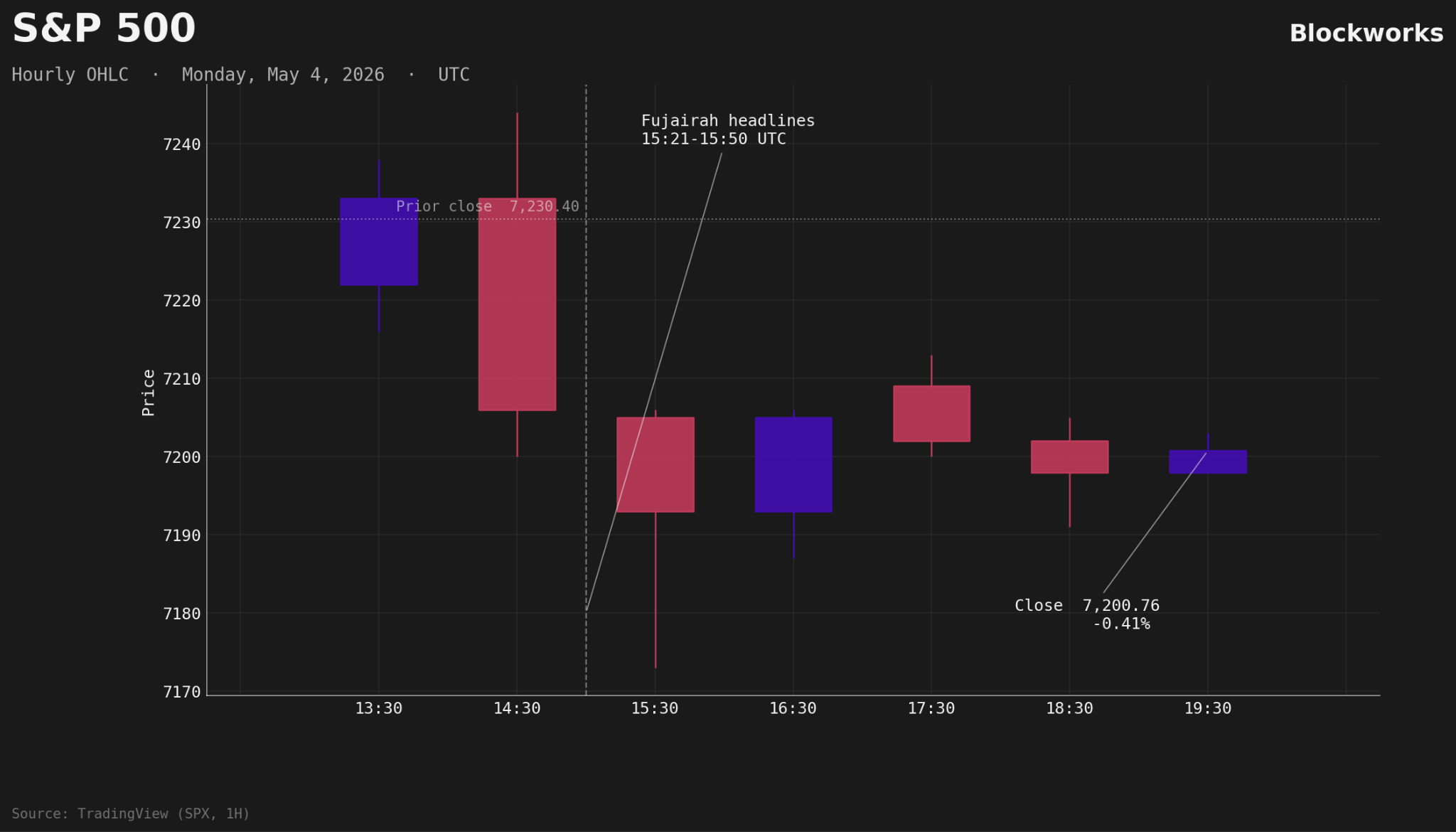

A fresh round of hostility over the Strait of Hormuz sparked a broad-based selloff early on Monday, but US equities caught a modest bid into the close.

Today, we also dig into Sky, one of DeFi's most under-discussed growth stories, and why USDS supply keeps climbing even as the savings rate has come down.

The first attack on the UAE since the April 8 US-Iran ceasefire — a coordinated Iranian missile and drone barrage on the Fujairah oil hub — soured what had begun as a constructive session for risk assets.

The S&P 500 closed -0.41% and the Nasdaq finished marginally lower at -0.19%.

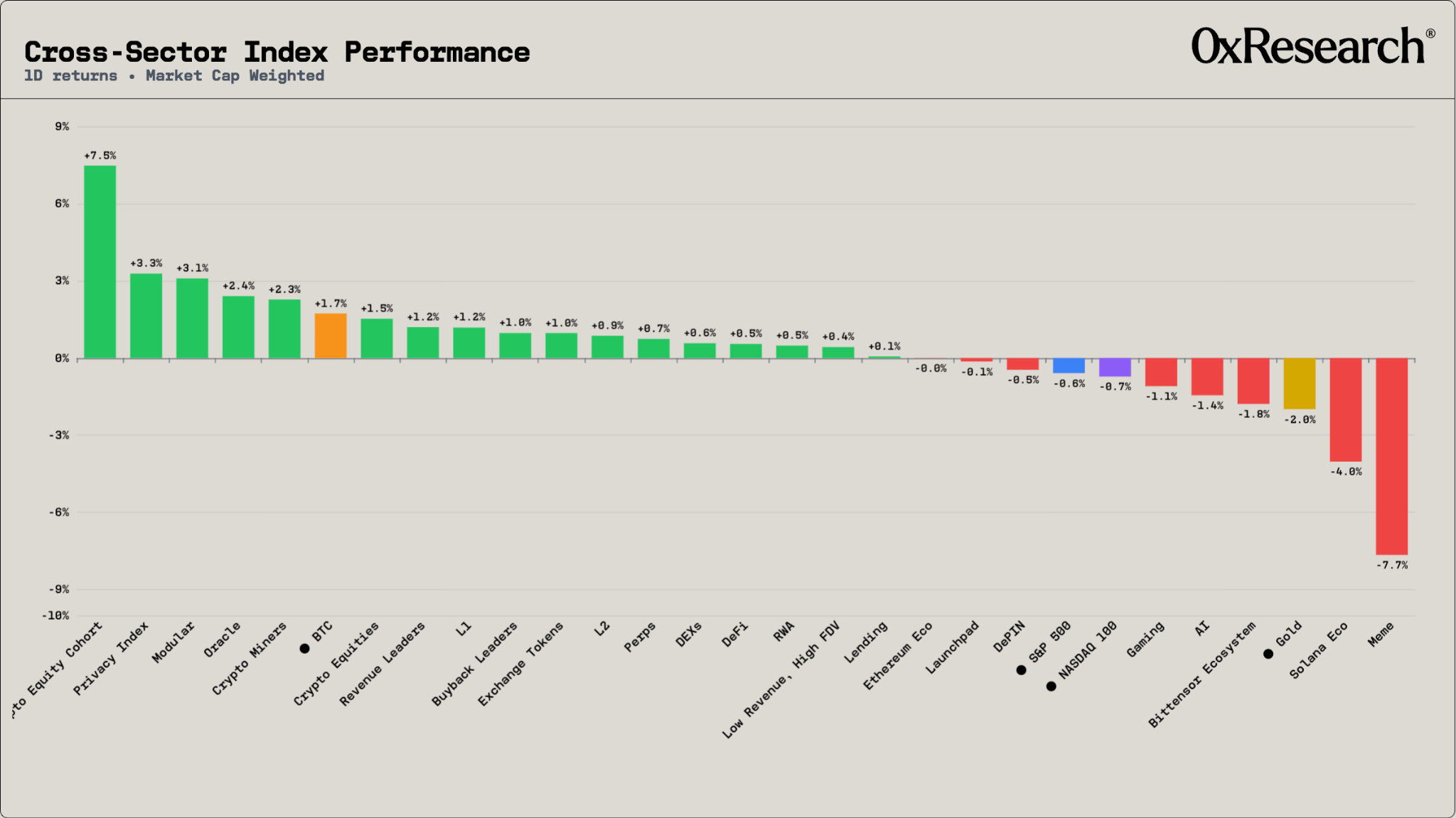

Circle (CRCL), however, bucked the day’s trend, surging 9%, propelling our Crypto Equities indices higher.

Bitcoin held up better than equities as well: BTC edged up over $80,000 — its highest print since January — before finishing the day just below, yet still solidly in breakout territory. Gold, counterintuitively, fell 0.63% to roughly $4,583/oz despite the geopolitical headlines, as a firmer dollar and rising Treasury yields pulled bullion lower.

That sucking sound you can almost hear when looking at the price action yesterday corresponds to a fresh round of Iranian attacks on Fujairah, the UAE port on the Gulf of Oman that is the emirates’ primary means to bypass the Strait of Hormuz. Damage assessments are underway after a large fire following the attack that injured at least three people.

Spot Brent Crude Oil briefly touched $120 per barrel, matching its April 30 peak.

The dollar and yield strength that pressured gold, despite the geopolitical risk, suggest rate expectations and inflation framing remain the dominant drivers for traditional safe-haven flows, irrespective of headlines. Bitcoin's relative resilience — closing above Sunday's level on a day that equities and gold both fell — is consistent with the corporate-demand thesis we discussed yesterday, but we’ll need more data before we can call it a trend.

— Macauley

Sky’s Quiet Climb

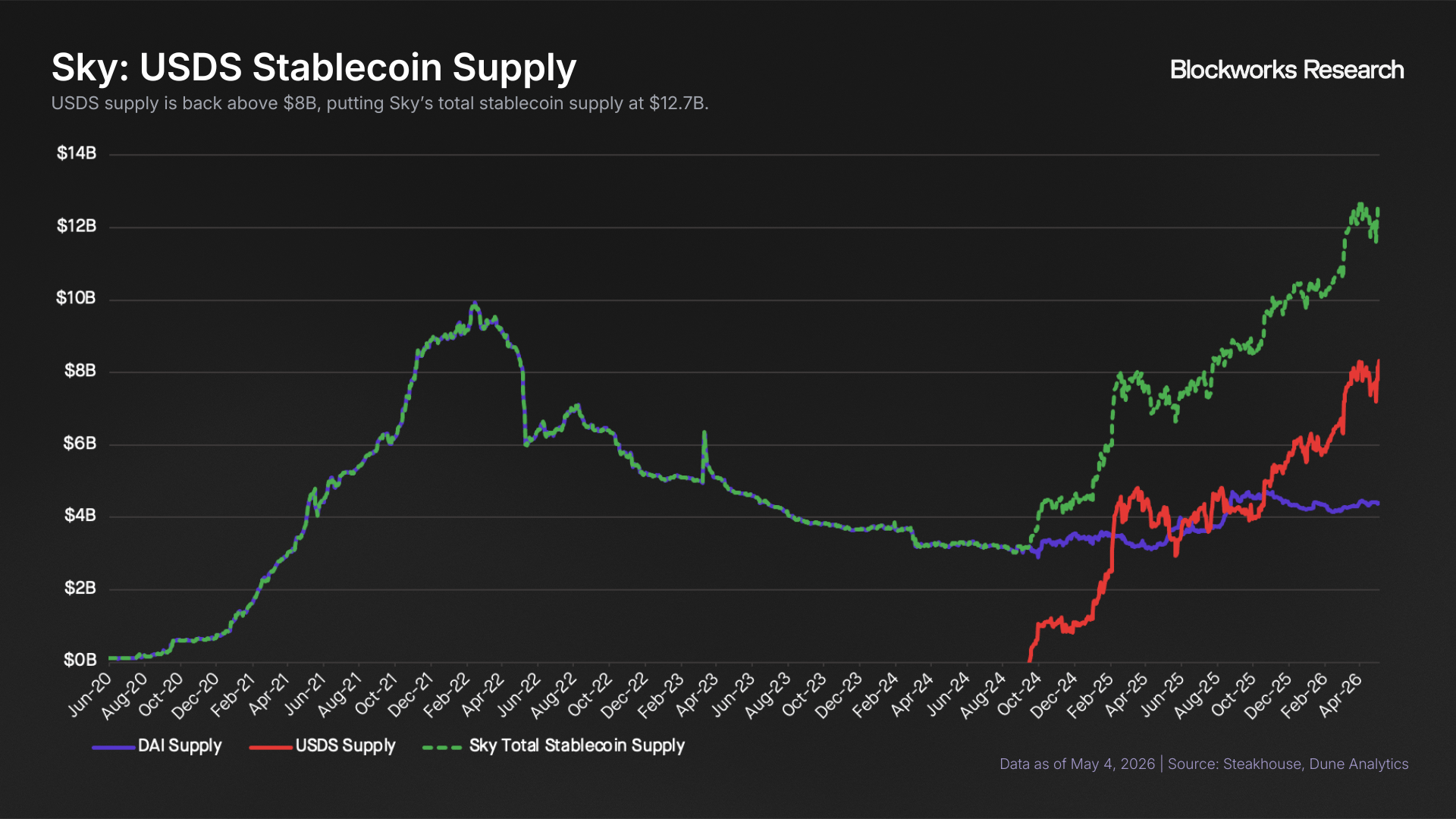

Sky remains one of the most under-discussed growth stories in DeFi. USDS supply has increased by $2.65B (47%) year-to-date, showing meaningful progress in an otherwise risk-off market. With total stablecoin supply at $12.7B, Sky is the third-largest stablecoin issuer behind Tether and Circle.

Sky's primary lever for generating demand for USDS is the Sky Savings Rate (SSR), a native yield USDS holders can access without any lockup. Users deposit USDS and receive sUSDS, a yield-bearing token whose value accrues against USDS over time that remains transferable and composable across DeFi.

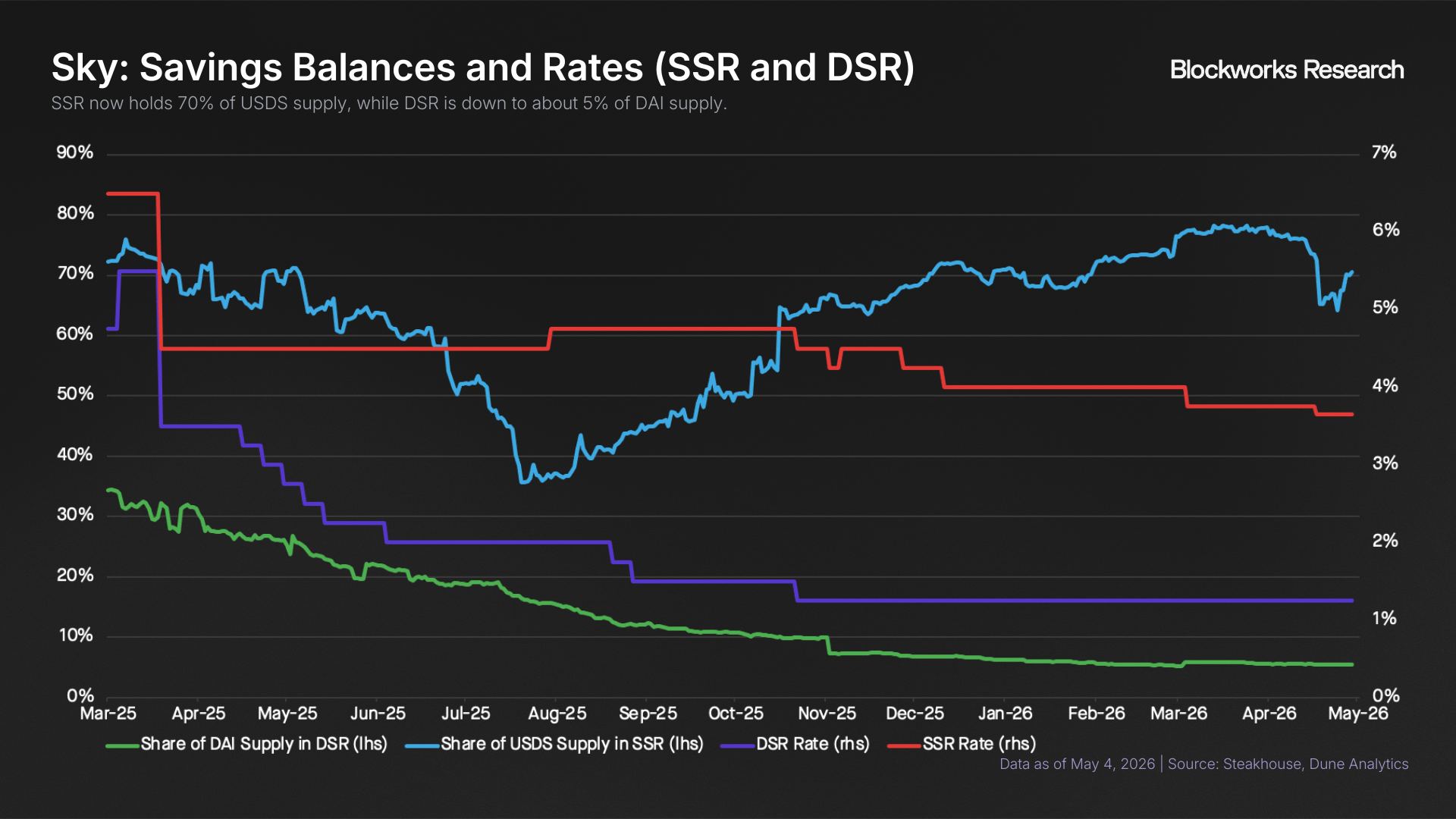

Alongside the SSR, Sky continues to operate the legacy Dai Savings Rate (DSR) for DAI holders who deposit into sDAI. Both rates are set by Sky governance in the same parameter votes, but the SSR is consistently maintained above the DSR (3.65% vs. 1.25%) as an incentive for DAI holders to migrate to USDS.

About $5.87B (70.5%) of USDS supply is deposited in the SSR vs. only $240M (5.5%) of DAI's supply. Even as SSR rates have been lowered 110 bps from 4.75% in Q4 2025 to 3.65%, the percentage of USDS supply locked in the savings product has increased from 50% at the beginning of October 2025 to 70.5% today.

The lesser-known side of Sky is its capital allocation model, which is what generates the yield paid to sUSDS holders. Sky is designed to remain a relatively simple base layer that sets the governance and risk framework — known as the Atlas — while growth and decision-making are pushed outward to independent capital allocators called Agents.

Within the rules of that framework, Agents compete to borrow USDS from Sky and deploy it into yield strategies. They pay Sky a wholesale cost of capital known as the Base Rate (currently 3.95%) and retain 100% of the spread earned above it. As of today, there is $7.94B of USDS debt outstanding across the three Agents: Spark ($4.20B, 53%), Grove ($3.13B, 39%), and Obex ($608M, 8%).

What’s interesting about Sky’s growth is that several competing yield-bearing instruments, like syrupUSDC and syrupUSDT, have offered higher yields over the past six months, yet Sky has not lagged.

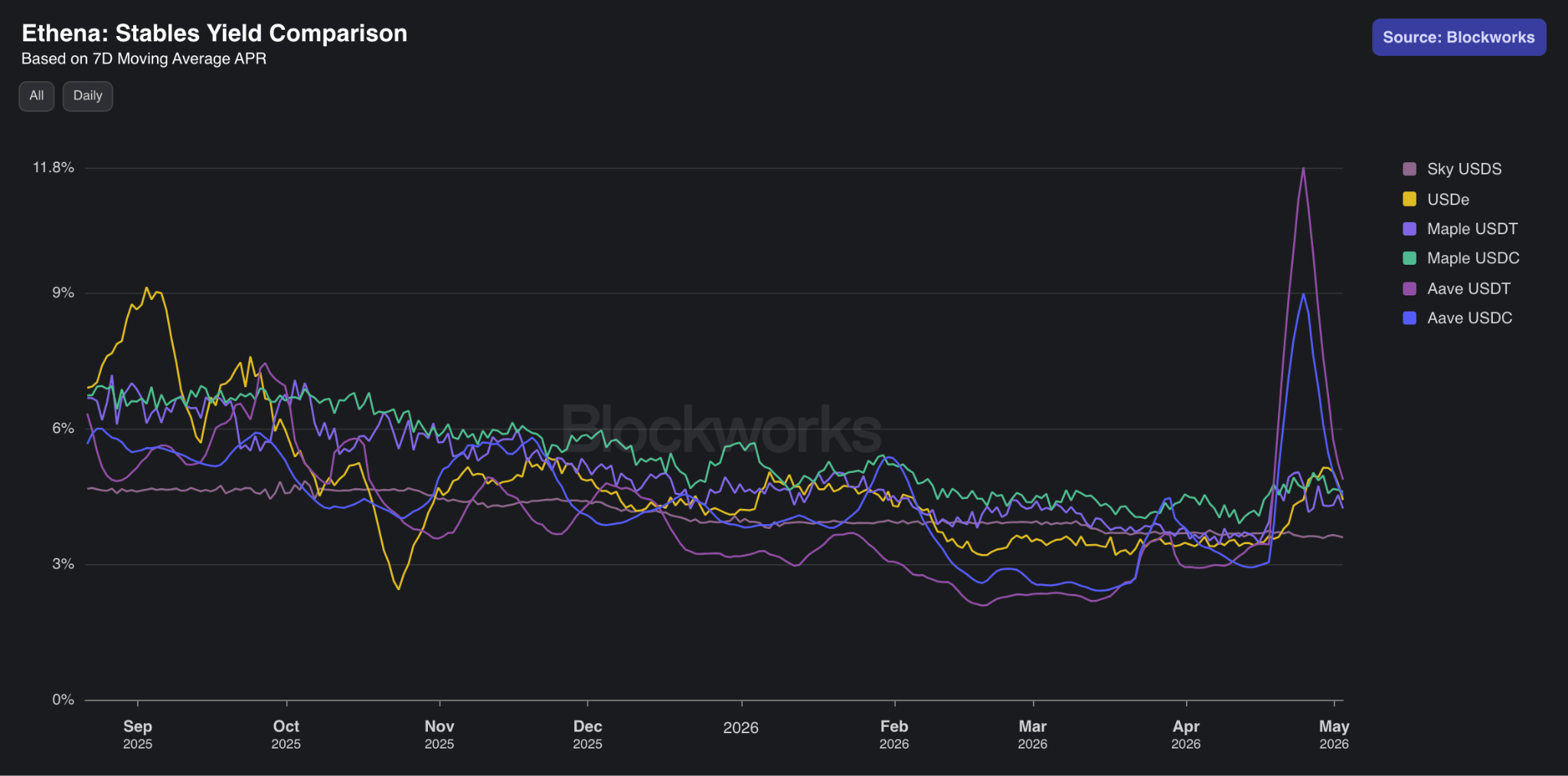

One explanation may be yield stability. As the chart below shows, sUSDS yield has been significantly more stable than other stablecoin yields, most notably sUSDe. That stability may be something the market values.

Today, sUSDS yields less than Maple, Ethena, and Aave, so it will be interesting to see whether growth can continue despite the lower headline rate.

— Carlos

Ann Miura-Ko argues that most companies calling themselves “AI-pilled” are only using AI for personal productivity, rather than operating as truly AI-native organizations. To make that distinction precise, she lays out a six-level framework from L0 (AI as theater) to L5 (a virtually self-driving organization), judged by four questions: what AI can see, what it can do, who can extend the system, and how the org chart has actually changed. The core claim is that real AI-native companies don’t just layer copilots onto a 2023 org structure; they rebuild around shared machine-readable context, cross-functional agents, non-engineers shipping internal tools, and eventually systems that can notice, decide, act, and learn with humans mostly setting strategy, taste, and risk boundaries.

Patryk from Serotonin published a piece on onchain credit, mapping the ecosystem across four main layers: credit issuance, capital allocation, infrastructure, and risk management. He also outlines 19 subcategories spanning more than 160 startups, protocols, and institutions. The piece argues that onchain credit is no longer just tokenized private credit funds or crypto-backed lending, but a full stack that includes institutional funds, tokenized offchain credit, onchain origination models, curators, yield-bearing products, money markets, tokenization rails, liquidity providers, tranching, and more. The broader point is that onchain credit is evolving into a real financial system with specialized participants across origination, funding, plumbing, and risk transfer — and that the next phase of growth depends on deeper liquidity, better composability, and more mature risk infrastructure.