- 0xResearch

- Posts

- Sky’s Balance Sheet Bet

Hi all, happy Tuesday! Equities opened the week at fresh highs, crypto equities sharply outperformed, and crypto ETF flows remained constructive.

Today, we continue our deep dive on Sky by looking inside its balance sheet: what backs USDS growth, how capital is being allocated, and what the model says about Sky’s position as a credit issuer.

The S&P 500 (+0.19%) and Nasdaq Composite (+0.10%) both closed at fresh record highs Monday, with the broad index settling at about 7,413 and the Nasdaq Composite at 26,274. Its first close above 7,400 for the S&P.

The rally came despite President Trump declaring what's left of the US-Iran cease-fire "on life support" after rejecting Tehran's latest peace counteroffer over the weekend.

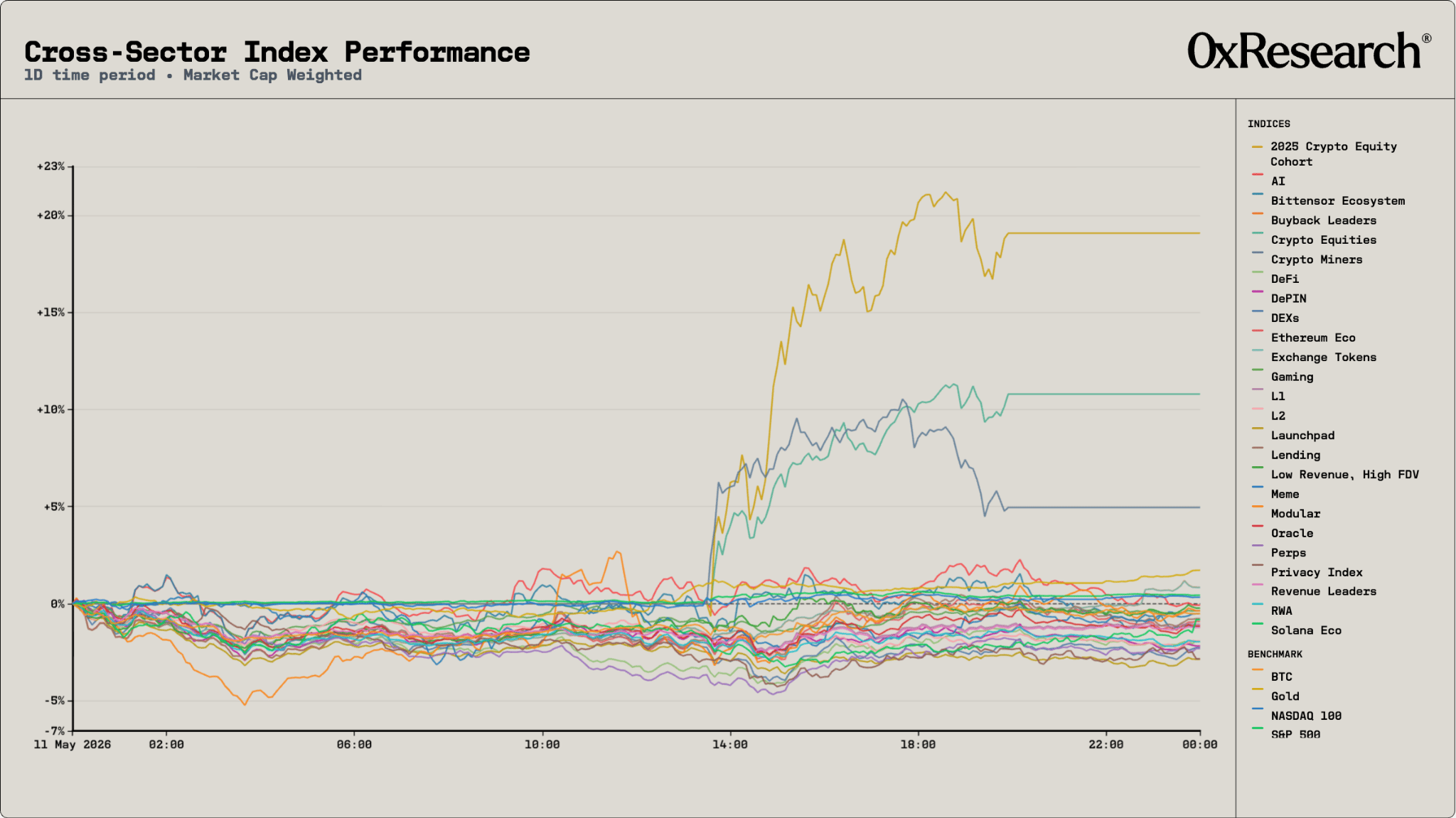

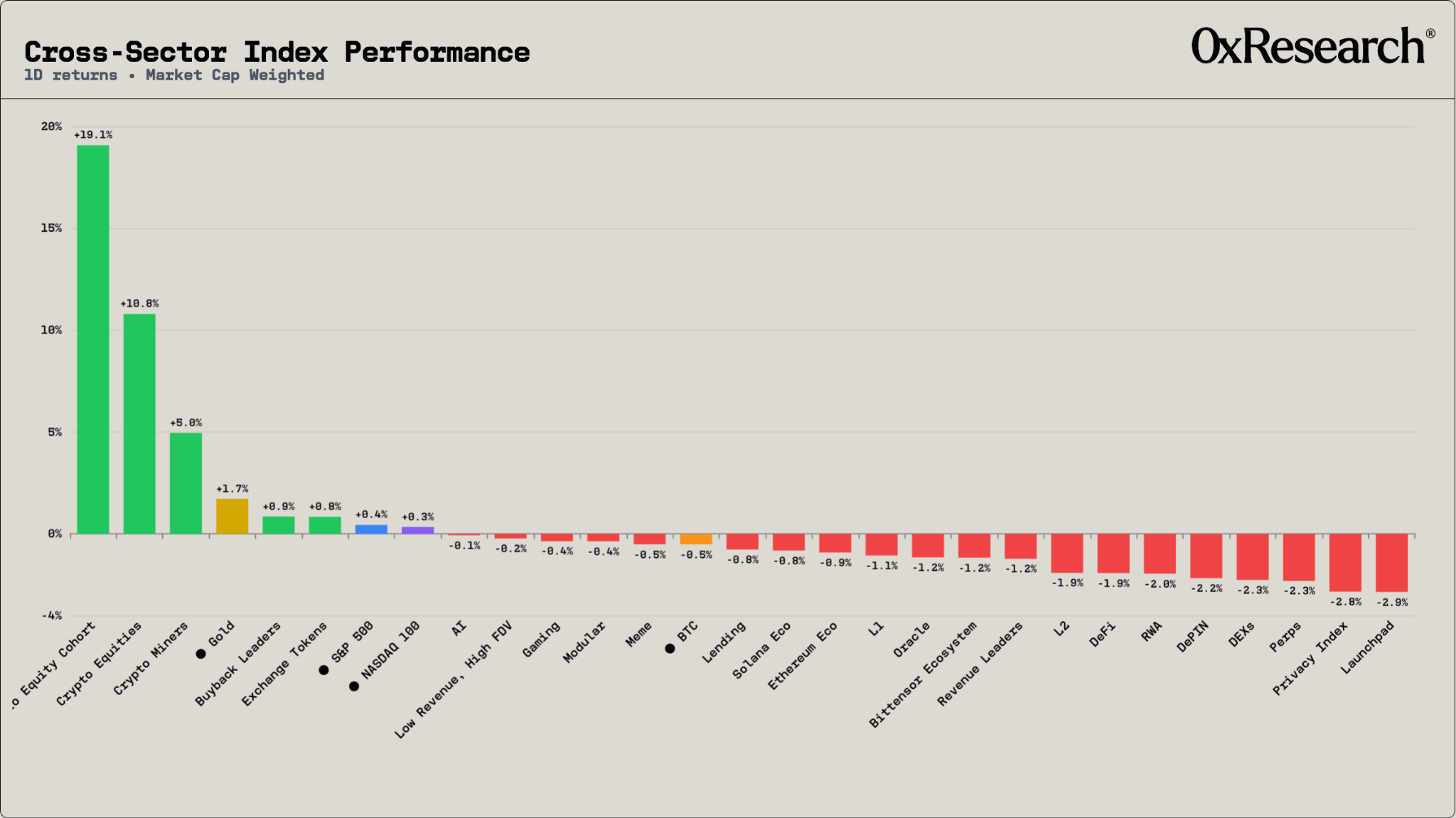

Crypto equities were the standout, with our 2025 Crypto Equity Cohort (+19.1%) on the day — leagues ahead of every crypto-native sector index, most of which finished in the red.

Circle (CRCL) drove the move, closing roughly +22% after the company posted record Q1 revenue of $694 million and reiterated that USDC circulation reached $77 billion.

The bigger catalyst, though, is Thursday: the Senate Banking Committee will hold its long-awaited markup of the Digital Asset Market Clarity Act at 10:30 am with the Tillis-Alsobrooks compromise preserving usage-based stablecoin rewards while banning passive, deposit-style yield. The compromise removes the overhang that's haunted Circle since Coinbase pulled support for the bill in January — though the banking lobby is still actively trying to tighten the language.

Crypto miners (+5.0%) and the broader Crypto Equities Index +10.8% (shown above) rounded out the equity-led rally, while BTC drifted -0.5% and most token sectors finished -1% to -3%. The divergence is notable: equities priced in policy progress, while tokens themselves traded sideways-to-lower.

Adding context from the flows side, CoinShares' latest Fund Flows Report showed digital asset investment products pulled in $857.9M last week — a sixth consecutive week of inflows, with total AuM rising to $160B. Bitcoin led at $706.1M, but other tokens participated materially: SOL ($47.6M), XRP ($39.6M), and ETH ($77.1M) all saw meaningful inflows as BTC broke back above $80,000 mid-week on the CLARITY Act stablecoin compromise.

Regarding stocks, it’s worth flagging the mechanical layer underneath this resilience amid the geopolitical risk: S&P 500 call options volume hit a record $2.6 trillion in notional value last week. The dynamic — call buying forcing dealers into negative gamma and mechanically into futures and equities to stay delta-neutral — offers a non-fundamental explanation for why headlines like a "life support" ceasefire keep failing to dent record highs.

It’s notable that SPX closed at 7,412.84, trading right through the 7,400 call wall where heavy open interest typically caps moves. That shows momentum is strong, but in principle the same machinery that's amplified the upside works in reverse on the unwind: when call premiums get too rich to keep buying, or a catalyst stalls momentum, dealers flip from buying to selling with equal force.

— Macauley

Inside Sky’s Balance Sheet

Last week, we argued that Sky is one of the most underdiscussed growth stories in DeFi, breaking down USDS supply growth, the Sky Savings Rate, and the Agent model driving demand for sUSDS.

This week, we’ll take an inside look at what is backing that growth.

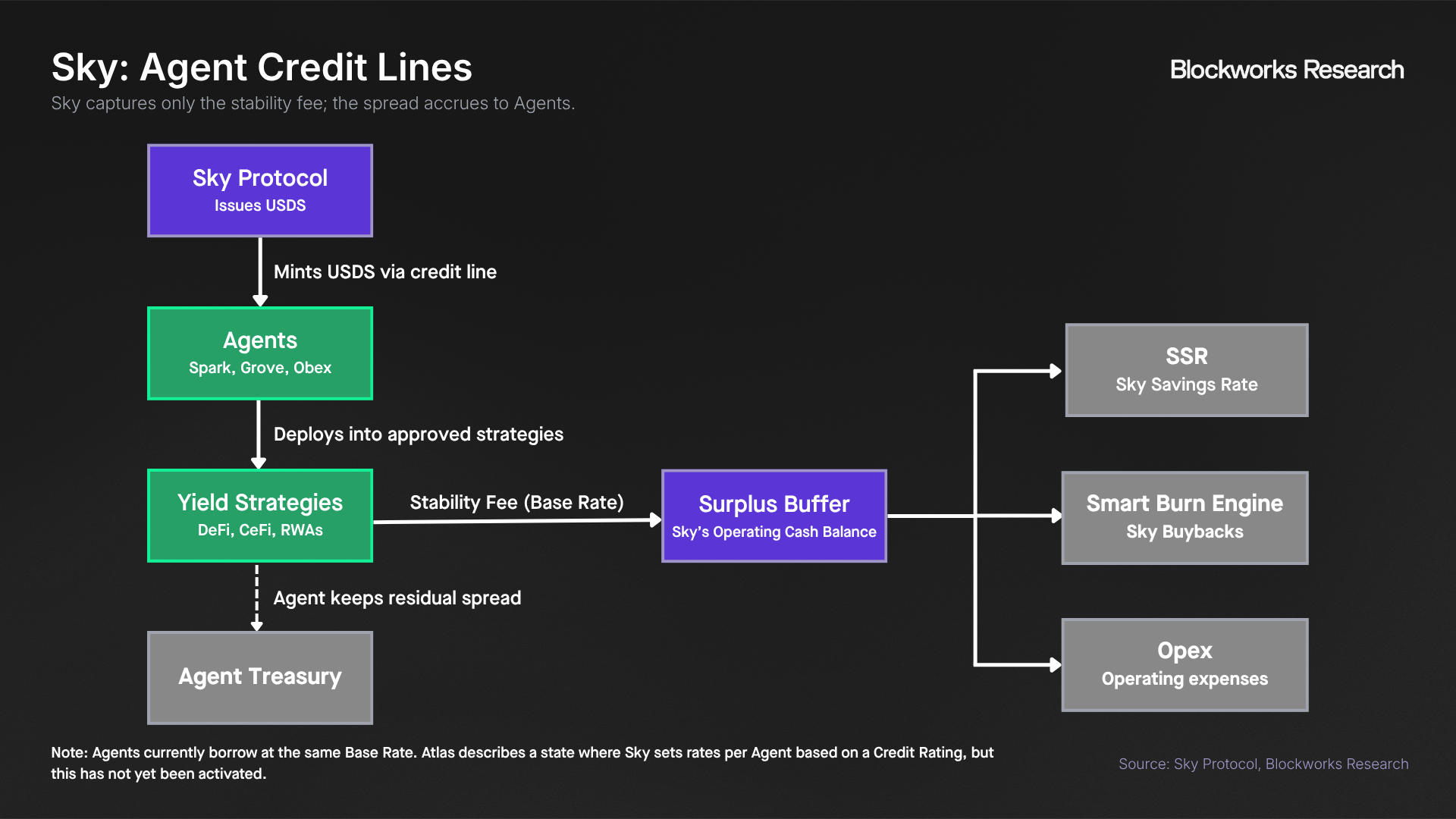

Sky should be viewed as a credit issuer. It issues stablecoin liabilities in the form of USDS and DAI, pays yield to attract deposits, and allocates capital through independent capital allocators that borrow from Sky at a wholesale rate and deploy into yield strategies.

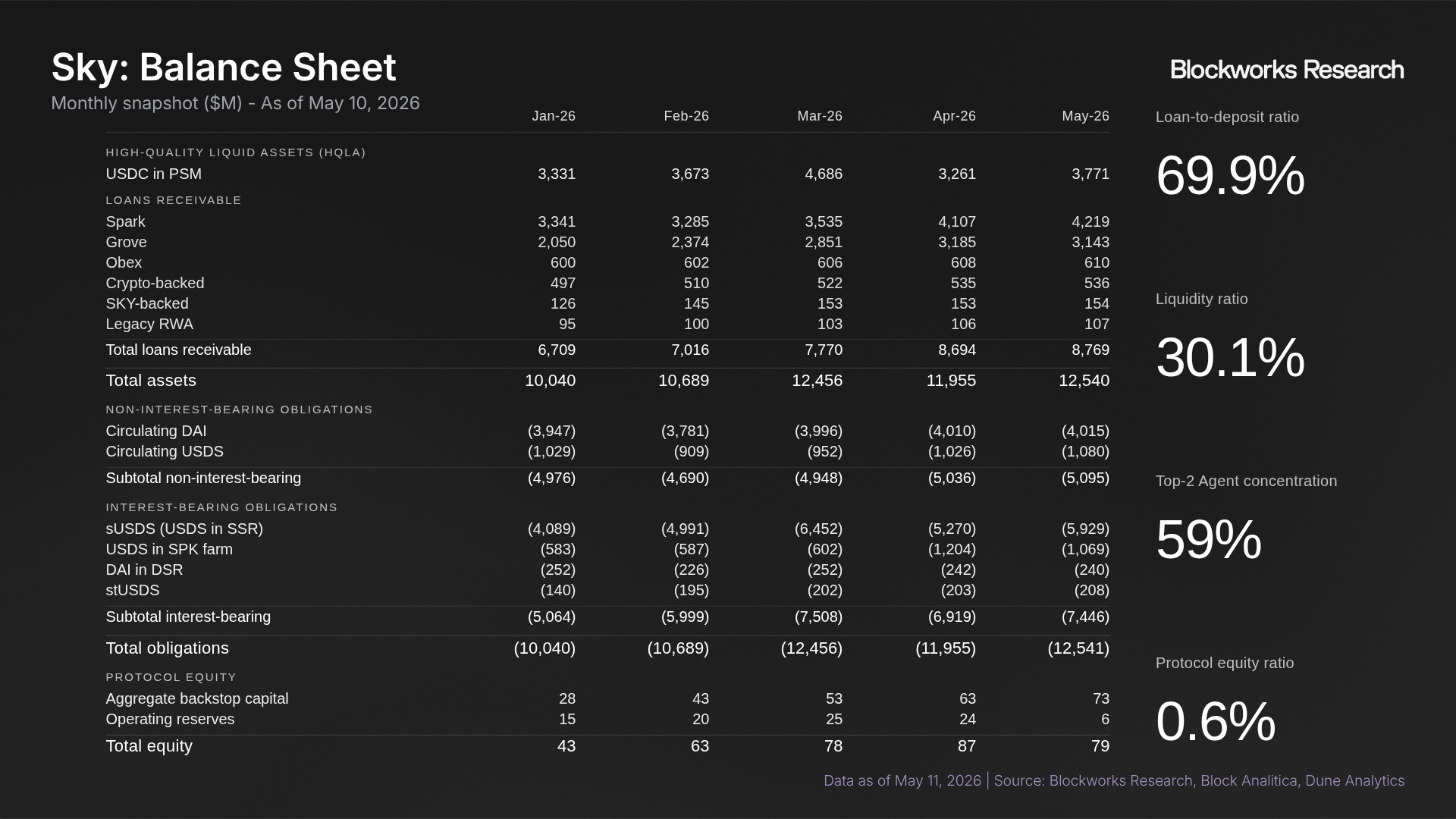

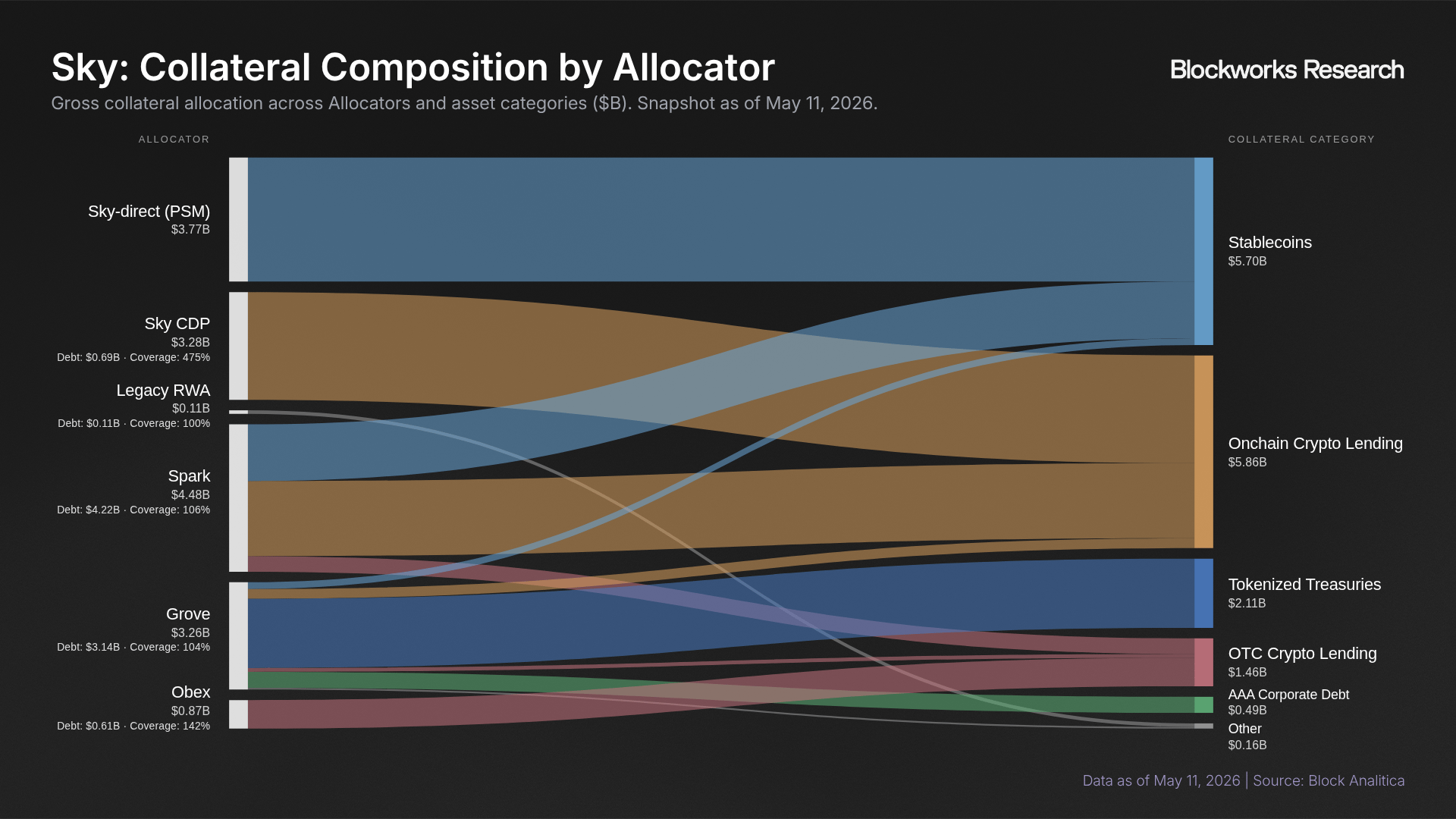

As of May 10, Sky had $12.6B of assets. Roughly 69% of stablecoin obligations fund a concentrated loan book, while the remaining 31% is backed by PSM USDC reserves. In banking terms, the PSM functions as Sky’s high-quality liquid asset base: it enables direct 1:1 USDS-USDC conversions at the protocol level and also generates income through Coinbase Prime’s yield-share on USDC reserves.

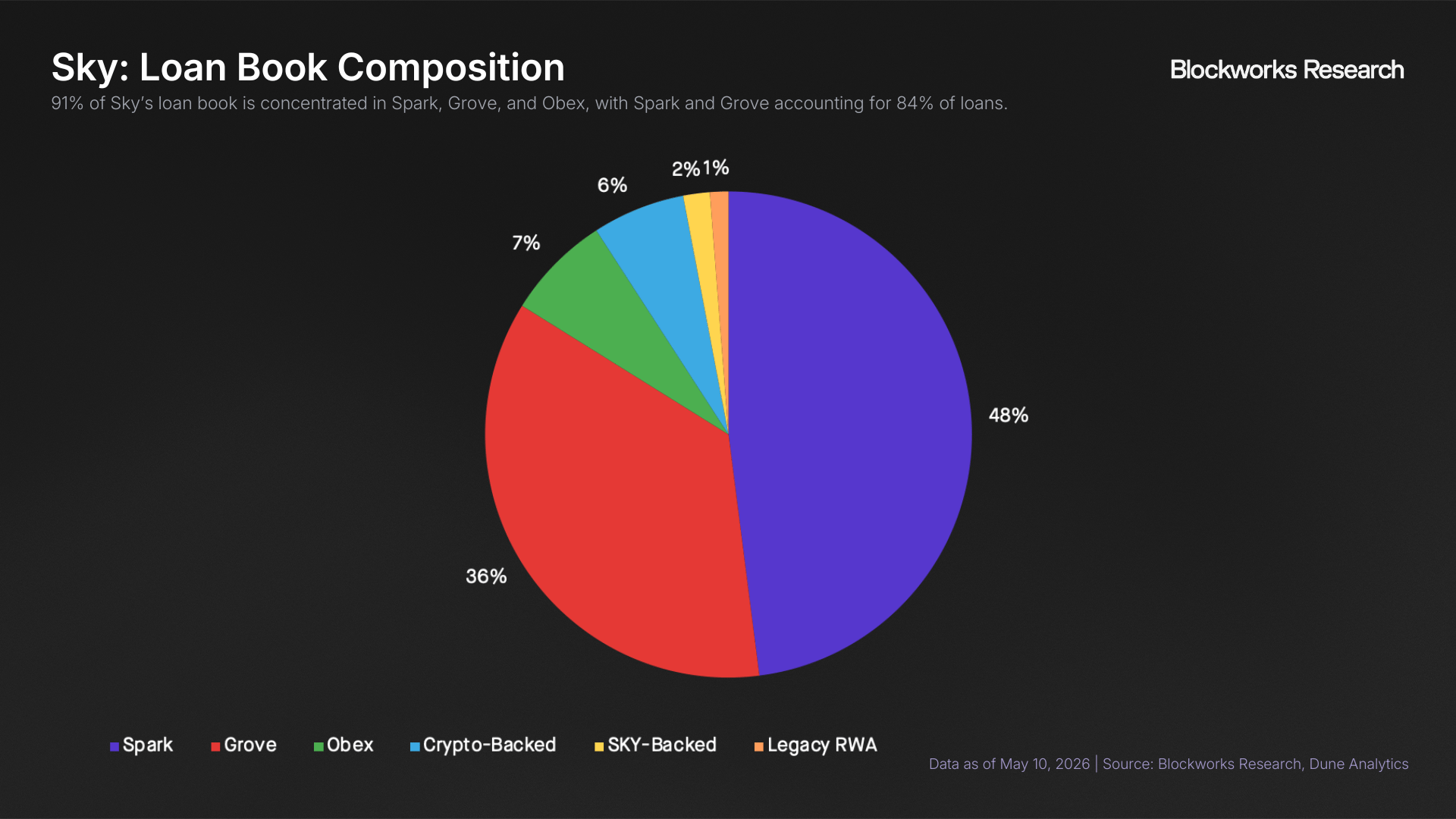

The loan book is dominated by the Agent network (originally known as “Sky stars”). Spark, Grove, and Obex account for $7.9B of outstanding USDS debt, or 91% of Sky’s loans receivable. Spark remains the largest allocator, actively managing capital across SparkLend, DeFi venues, and institutional lending channels. Grove focuses on institutional credit and tokenized RWAs, while Obex acts as an incubator for external capital allocators such as Maple, Securitize, Centrifuge, Better, River, Daylight, USDai, and TVL Capital.

This makes Sky’s growth materially different from a simple stablecoin expansion story. USDS supply growth is effectively tied to Sky’s ability to source attractive, risk-adjusted yield opportunities through its Agents. The upside is that the model can scale beyond what a single protocol team could underwrite internally. The tradeoff is that Sky’s balance sheet becomes more dependent on the quality of its capital allocators, their deployment mandates, and the risk controls enforced by governance.

On the surface, Sky’s capital position looks thin. Protocol-level equity is only about 0.5% of obligations. But that headline number understates the system’s actual loss-absorption capacity. Across the system, $15.9B of underlying collateral backs $12.6B of stablecoin obligations, implying 126% gross coverage. Coverage varies by allocator: Sky-direct collateral stands at 156%, Obex at 142%, Spark at 107%, and Grove at 104%.

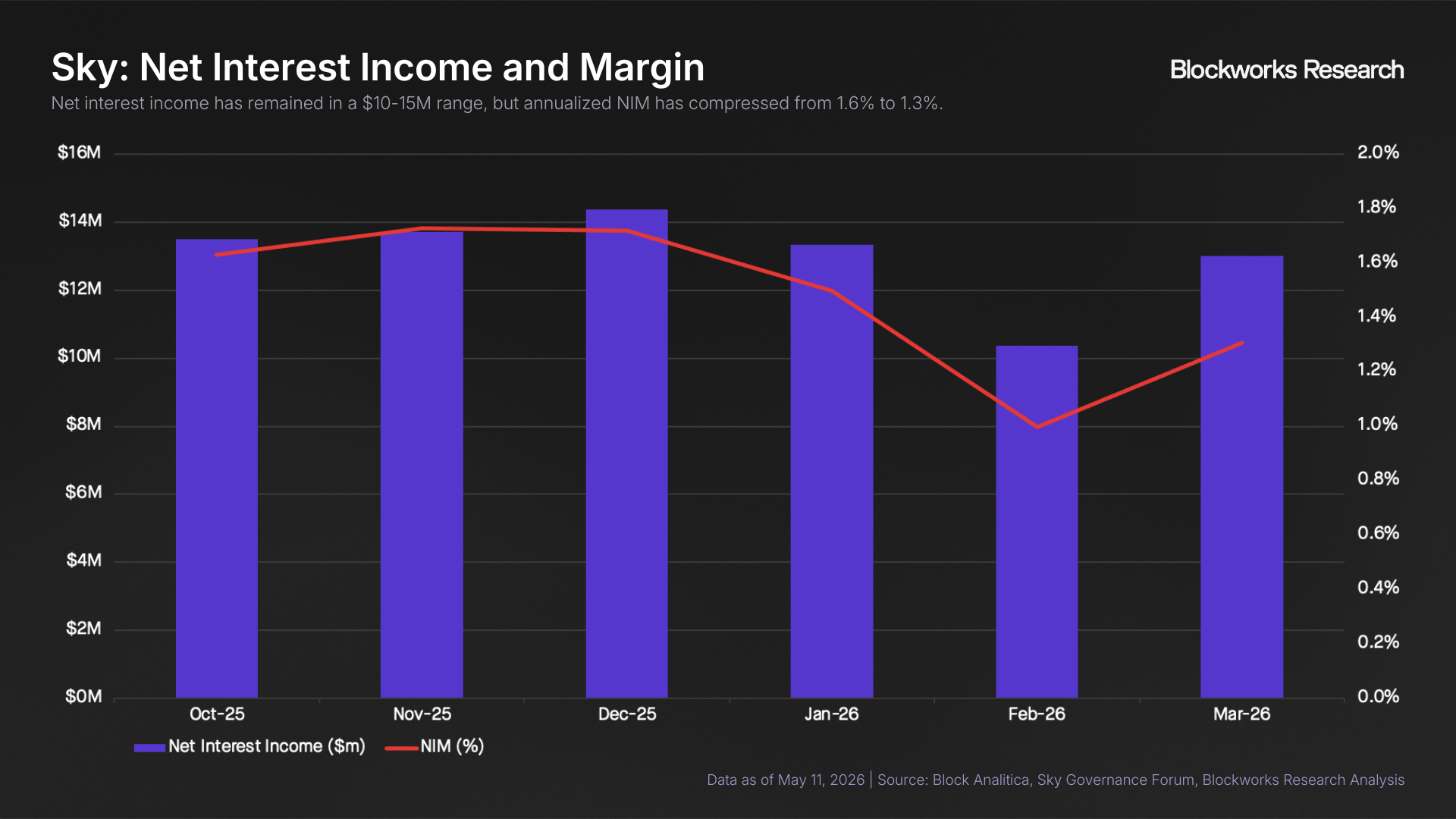

The most interesting part of this setup is the tradeoff Sky is making. It is using attractive stablecoin yields to grow the USDS supply, but that growth only creates value if capital can be redeployed at a sufficient spread. Over the past six months, Sky generated $33.2M in average monthly gross interest income, while net interest income remained in the $10-15M range. However, annualized net interest margin compressed from 1.6% to 1.3% as Sky absorbed deposits faster than capital allocators could redeploy them at attractive spreads.

The protocol has successfully grown stablecoin supply in a risk-off market, but growth has become somewhat yield-dilutive in the near term. If Agents can continue scaling deployments without materially increasing risk, Sky’s earnings power should improve as idle liquidity gets put to work.

For now, Sky’s story is no longer just about USDS growth. It is about whether DeFi’s largest decentralized stablecoin issuer can evolve into a credible onchain credit system: one with diversified capital allocators, transparent liquidity reserves, and enforceable risk limits.

— Carlos

Circle’s ARC whitepaper presents Arc as a public L1 designed to be the internet’s “Economic OS”: a shared financial platform where stablecoins, tokenized assets, payments, lending, and markets run on one composable stack with deterministic settlement, configurable privacy, and stablecoin-native fees. ARC is framed as the network’s native coordination asset, tying together five functions: staking/economic alignment, governance, fee capture, platform utility, and an expanding utility surface across Circle and partner products.

The paper emphasizes a gradual transition from a permissioned validator set under Circle’s stewardship toward a PoS model with tokenholder governance over economic parameters, while keeping some operational and compliance decisions centralized at first. Economically, ARC starts with a 10B token supply, a decaying inflation model, protocol-level conversion of fees into ARC for distribution plus burn, and an initial allocation of 60% ecosystem, 25% Circle, 15% long-term reserve. The broader thesis is that blockchains, stablecoins, and regulatory progress have finally aligned to make a shared economic operating system viable, and Arc is Circle’s attempt to become that foundational coordination layer.

Eric and Hayden from Jito join Lightspeed to discuss Solana Accelerate, the launch of Jito’s Maker Prioritization Plugin, and broader efforts to improve Solana’s market structure through more deterministic transaction scheduling. The discussion also covers validator incentives, BAM architecture, plugin experimentation, perpetuals and prediction markets, tokenized assets, and why user experience and distribution will be critical for driving onchain trading adoption.