- 0xResearch

- Posts

- ⚜️Return to fundamentals?

⚜️Return to fundamentals?

Token buybacks and price multiples are back in vogue

Brought to you by:

Crypto fundamentals are back in, the L1 premium is dying and the fat app thesis is returning. All music to the ears of fundamentals-oriented investors. Ethereum’s governance and foundation are making moves.

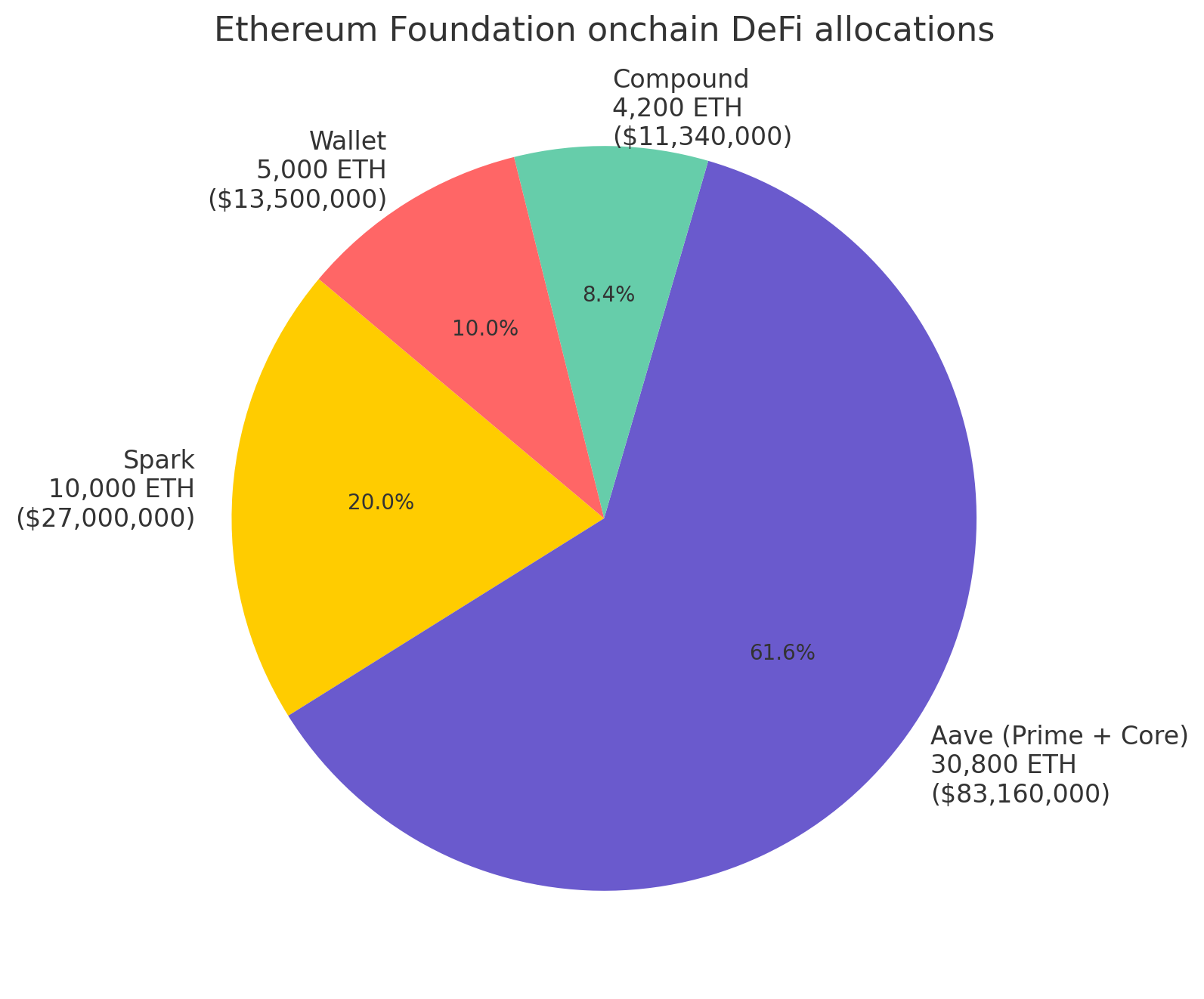

The EF starts DeFi portfolio:

Data source: DeBank

The Ethereum Foundation (EF) now has 50,000 ETH (~$135M) deployed across select DeFi protocols and its Safe 3-of-5 multisig wallet, marking a shift towards greater onchain engagement.

The deposits, all made on Feb. 13, breakdown as follows:

Aave (Prime + Core): 30,800 ETH (~$83.16M) – 61.6%

Spark: 10,000 ETH (~$27M) – 20.0%

Compound: 4,200 ETH (~$11.34M) – 8.4%

Wallet: 5,000 ETH (~$13.5M) – 10.0%

The move follows criticism last month that EF members were not sufficiently active onchain. In response, EF committed to deploying treasury funds into DeFi rather than relying solely on offchain custody, and it has now followed through.

With Aave holding the largest share, this allocation is extremely conservative, but does signal the EF’s support for Ethereum’s DeFi ecosystem.

Will this shift lead to still greater EF participation in DeFi dapps? In total, the EF holds about 292,000 ETH in its treasury as of its most recent report, representing over 99% of its crypto holdings.

Brought to you by:

SKALE, the gas-free invisible blockchain, is “Built Different” for mass adoption: high-throughput, scalable, and fair. As a network of interoperable EVM-compatible L1s, SKALE’s user experience focus has accelerated a strong ecosystem across gaming, AI, and more. Due to SKALE’s gas-free nature, blockchain can be integrated invisibly, creating accessible Web2-like experiences for users and developers.

SKALE has:

Over 50M UAWs

9 Games on the Epic Games Store

Saved Users over $9.5B on Gas Fees

Dive in to learn more.

The return of crypto fundamentals

The permissionless nature of crypto means anyone with a computer and internet connection can have a bag. That makes it really hard to value tokens.

Price-to-sales multiples of L1s like Cardano or Ripple trade at absurd four to five figure ranges, far above actual value-generating L1s like Solana (32x) and Ethereum (227x).

Then there are tokens like OM (who?) that are clocking in the highest price gains of 47.6% since the industry’s biggest liquidation earlier this month.

The best advice I can give crypto founders right now is to find the $OM market maker and hire them.

— Lai Yuen (Former .eth) (@0xlaiyuen)

5:31 AM • Feb 10, 2025

No rational explanation exists. It’s all narrative and “speculative premiums.”

But is that going to stop investors from trying to formally value tokens? No, because there is a lot of money to be made from unearthing the gems.

In the short history of this industry, investors have tried to value L1s with a variety of now-abandoned tools like the stock-to-flow model, total-value-locked to market cap ratios or proof-of-stake staking cash flow yields.

The latest shift in investor sentiment around token valuations is doubling down on an emphasis on the importance of fundamentals.

Maelstrom fund points to Vertex perps DEX, arguing that markets are “underestimating” the DEX’s growth and that it “should” be trading at a 200% to 300% greater valuation in line with its peers.

1kxnetwork fund’s recently published Ronin chain thesis points to the gaming chain’s deflationary burn of SLP, plus rising daily active users and breakout revenue-generating game Pixels ($20.7 million in 2024).

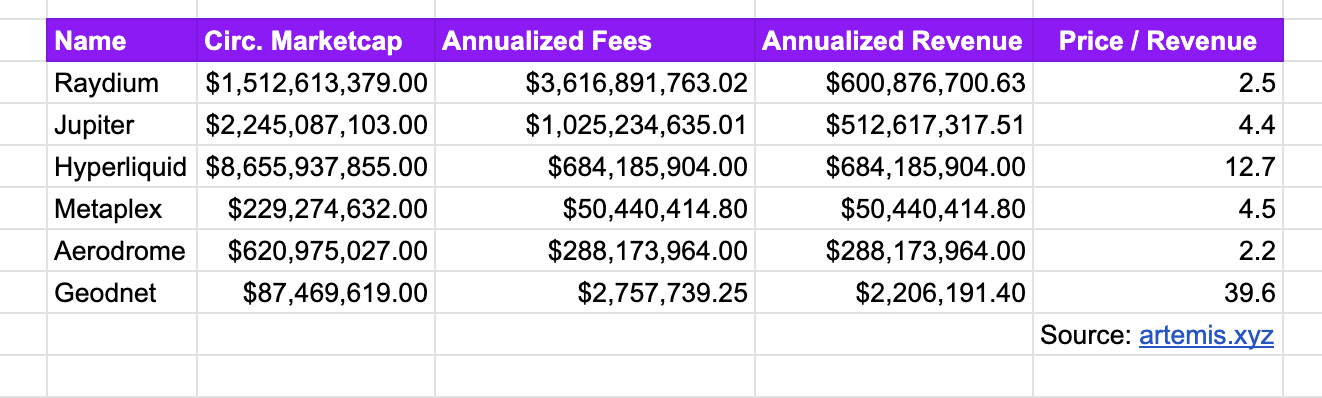

Applications like Raydium, Hyperliquid, Metaplex, GEODNET, and Jupiter are all trading at reasonably “rational” P/S ratios that are based on consistent cash flows and more measurable growth potential.

Source: Artemis

Many of these projects are also engaging in huge token buybacks, often perceived as a “fundamentals-driven” strategy to improve the attractiveness of price multiples.

Jupiter’s token buyback program may quite possibly be the largest (in USD terms) with a commitment of 50% protocol fees. That comes up to a buyback of ~9.4% of JUP’s total circulating supply, based on this rough estimate.

Supporting the point that “fundamentals are back” is also the ugly reality of declining L1/L2 valuations.

The fabled “Layer-1 premium” is slowly evaporating. L1s in the previous cycle like Starknet raised at eye-popping valuations of $8 billion, while newer L1s command less than half of those valuations (Berachain $420 million, Story Protocol $2.25 billion, Celestia $3.5 billion).

The down-only price action of most L1s/L2s in the last 12 months will likely grind future valuation numbers down even further.

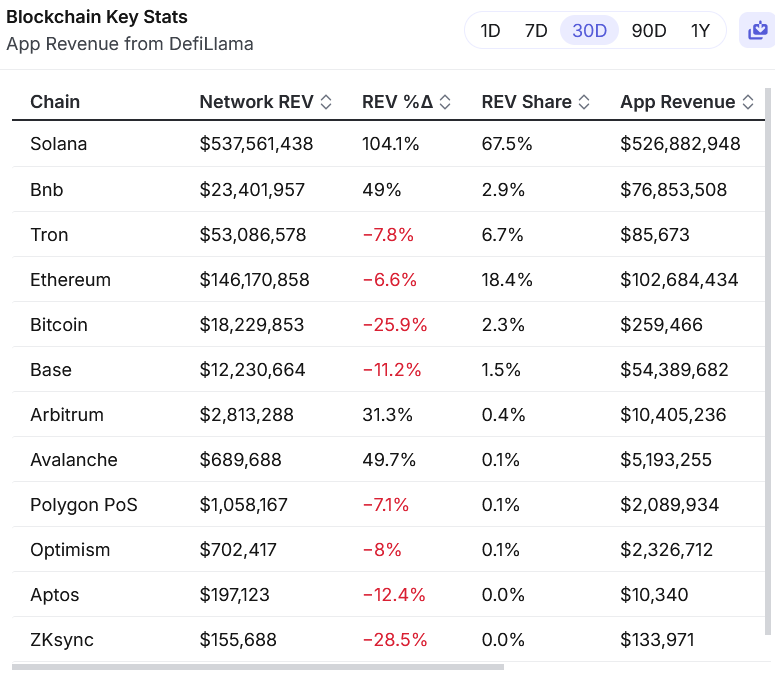

Application revenues are also beginning to outpace the revenues of the underlying L1 and L2 protocols, Blockworks’ Dan Smith points out.

Source: Blockworks Research

This all hinges on the growing disdain of the industry’s infrastructure bloat. The fat protocol thesis is no longer, now is the era of the fat app thesis.

1) Fat Protocol Thesis

.

. <—— we are here

.

2) Fat Application Thesis

.

.

.

3) Fat User Thesis— Jon Charbonneau 🇺🇸 (@jon_charb)

1:23 AM • Feb 14, 2025

Ethereum devs push for faster, more predictable forks

Ethereum’s core developers are rethinking the network’s upgrade cadence, debating a shift toward smaller, more frequent hard forks. On the latest All Core Devs (ACD) call, developers broadly supported the idea of six-month upgrade cycles but acknowledged that reducing timelines beyond that would introduce new coordination challenges. As one participant put it, “The actual bottleneck here is on testing, and I think it’s unreal to expect that we first need to agree among all clients on what we're going to implement before we even spin a devnet.”

To meet this goal, developers emphasized the importance of freezing fork scope early to prevent the kind of last-minute additions that disrupted the Pectra upgrade. But that doesn’t mean developers shouldn’t stay flexible, argued Geth developer Lightclient.

“With Pectra, we continued adding stuff in — just tried to do a lot of stuff in parallel, and it blew up in our face — and now it seems like we're coming back and we're going farther on the other end,” Lightclient said.

He pushed back against the notion that developers should finalize the scope of the next hard for, Fusaka, even before Pectra’s mainnet activation is live.

In contract, Roman Krasiuk, with the Reth team, pushed for earlier scope finalization as key to faster upgrades.

“We would never get to a faster pace if we don't commit ahead of time to the scope — and I agree we can use the all of the time remaining until Pectra lands on mainnet to still finish this discussion.” But once Pectra is shipped, he argues it would be counterproductive to continue discussing unfinished EIPs as potential candidates for Fusaka.

Another contentious discussion revolved around whether execution layer (EL) and consensus layer (CL) forks should be decoupled. While some developers believe separate upgrades could reduce coordination overhead, others warn that it might complicate client implementation and user adoption. This remains an open question.

Meanwhile, discussion over EVM Object Format (EOF) is back. Some Geth team members have long opposed it in Fusaka or at all, arguing that it diverts focus from higher-priority upgrades. “EOF on the EL does not really make much sense given where we are today,” one developer noted, pointing to ongoing developments in ZK EVMs. Others contend that EOF represents a necessary evolution in smart contract execution, improving security and efficiency.

Ethereum is such a big project with so many stakeholders, its sometimes unwieldy governance processes will need to adapt. The views of 100-developers on a biweekly call still carry a lot of weight, but over time it is expected to be supplanted by more formalized asynchronous decision-making.

However the sausage gets made, all developers agree to work toward greater predictability in network upgrades

— Macauley Peterson

|

|