- 0xResearch

- Posts

- Mastercard wants the rails

Hey all, happy Tuesday!

BTC outperformed equities on the March 23 close, but the more durable signal sat below the benchmark table. While AI, gaming, and DePIN led the day’s rebound, Mastercard’s move for BVNK, PayPal's wider PYUSD rollout, and DTCC's interoperability push all pointed to the same place: Stablecoin and tokenization infrastructure is moving inside mainstream finance.

What traders bought and what incumbents are buying are not quite the same thing. Today’s issue covers the uneven bounce and why the rails are becoming the real institutional battleground.

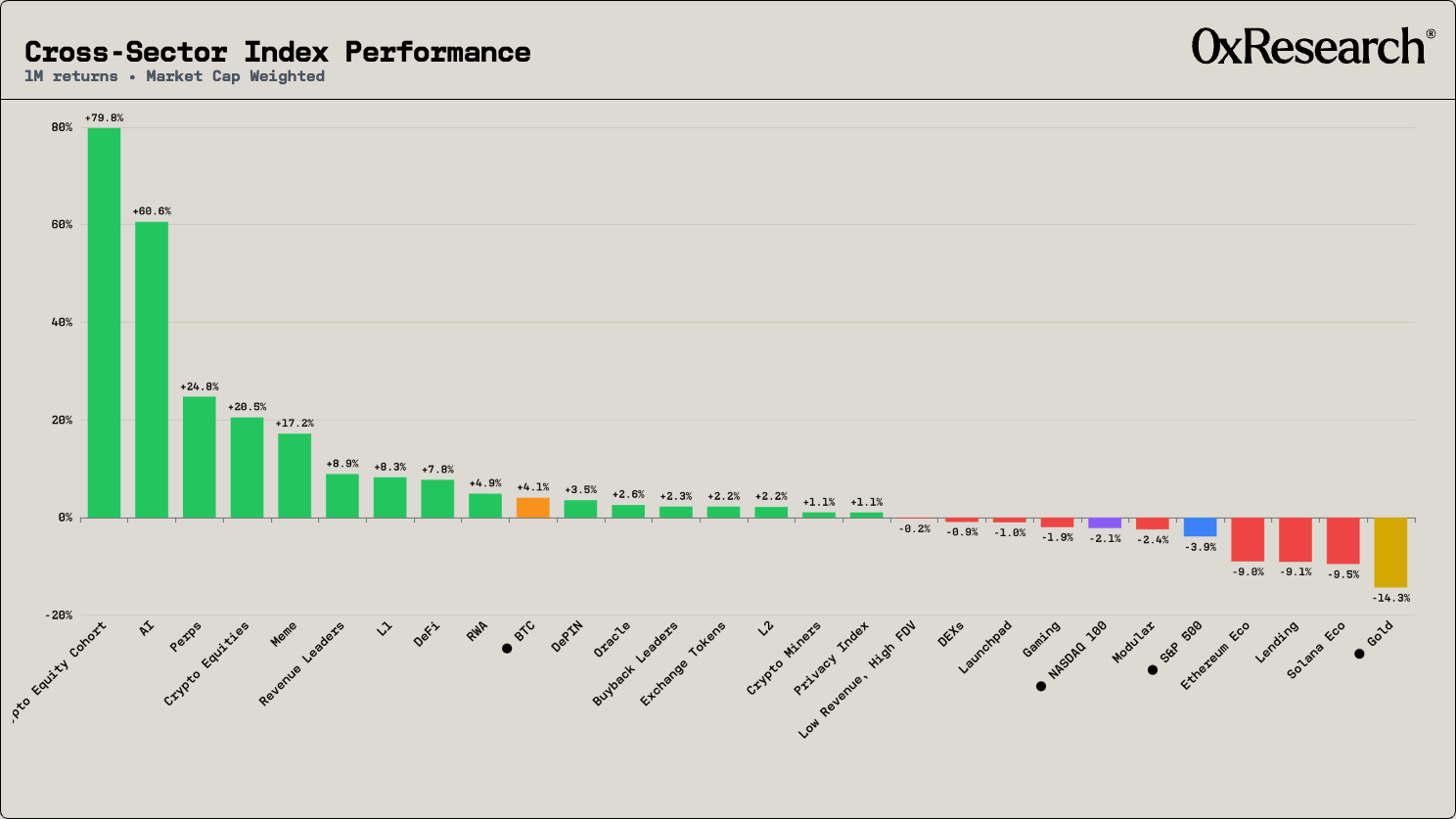

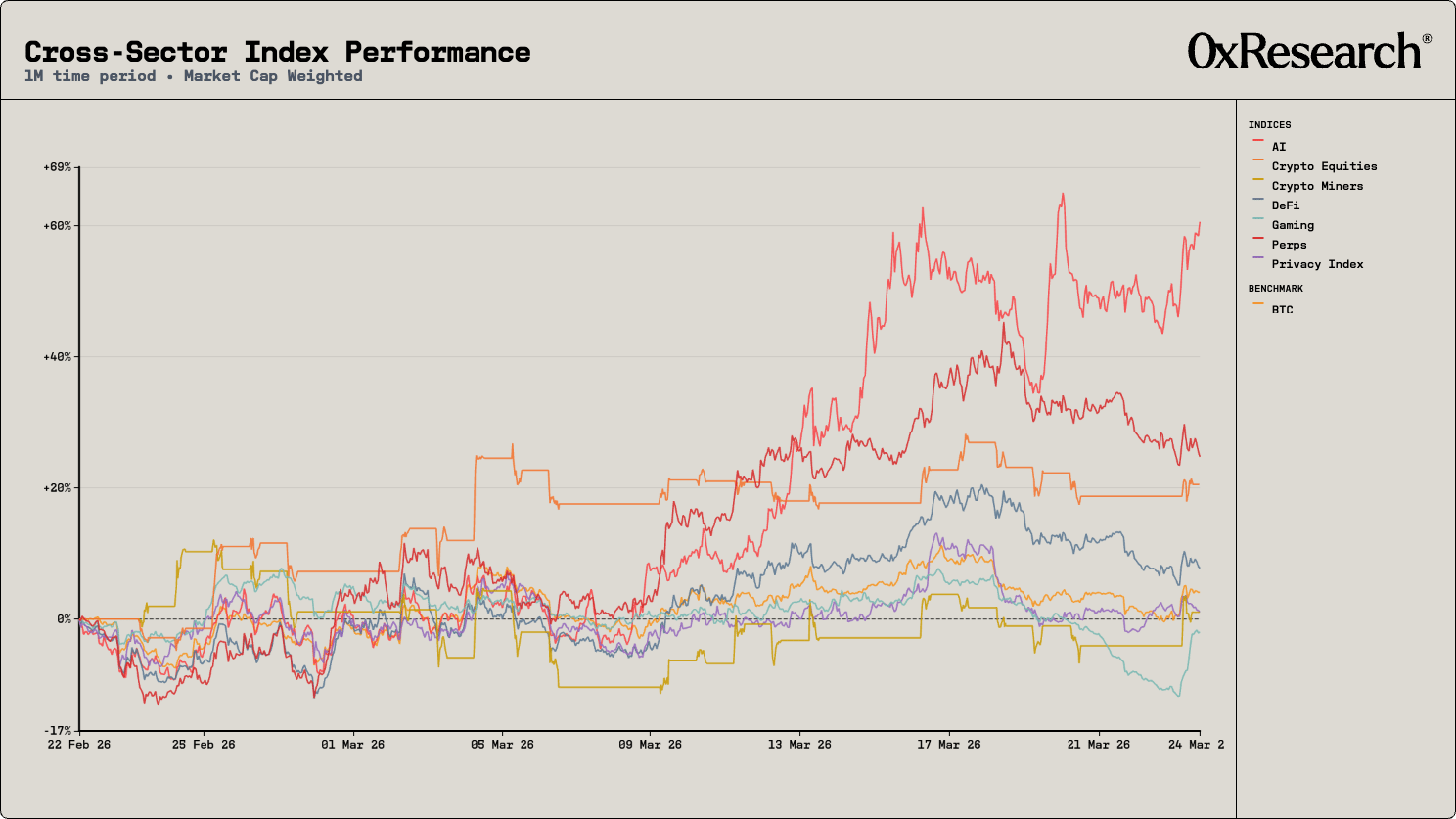

BTC outperformed every major benchmark on the March 23 close, finishing up +4.4% versus QQQ +1.8%, SPY +1.5%, and flat gold. That’s a clean enough headline on its own, but the more useful signal was what happened under the surface: The bid was broad enough to feel constructive, yet the leadership was far from uniform. That kept the session from reading like a clean all-in risk chase.

The strongest pockets of crypto beta sat in AI Top 10 (+11.6%), Gaming Top 20 (+9.9%), and DePIN Top 20 (+7.3%). That tells you traders were willing to pay for duration and narrative beta again, but not indiscriminately. 21 of 24 BWR sectors finished green, so this was not a narrow majors-only move. Still, the laggards matter just as much as the winners.

Perp Index was the worst-performing sector on the day at -3.0%, followed by Privacy Index (-0.9%) and DeFi Top 20 (-0.4%). That is a notable reversal from the recent run of perps-heavy and AI-heavy storylines that have dominated recent newsletter copy. Even the more equity-linked sleeves of crypto failed to fully keep pace, with Crypto Equities up just +1.5% and Crypto Miners up +2.1%, both well behind BTC and nowhere near the best token cohorts.

The cleanest read is that Monday's move rewarded long-duration token beta more than it rewarded the recent market darlings or the balance-sheet proxies. If that bid broadens from here, the next session should see DeFi, perps, and crypto equities start to catch up. If it does not, this will look less like the start of a clean market-wide rotation and more like a sharp but selective catch-up rally.

— Daniel

Mastercard wants the rails

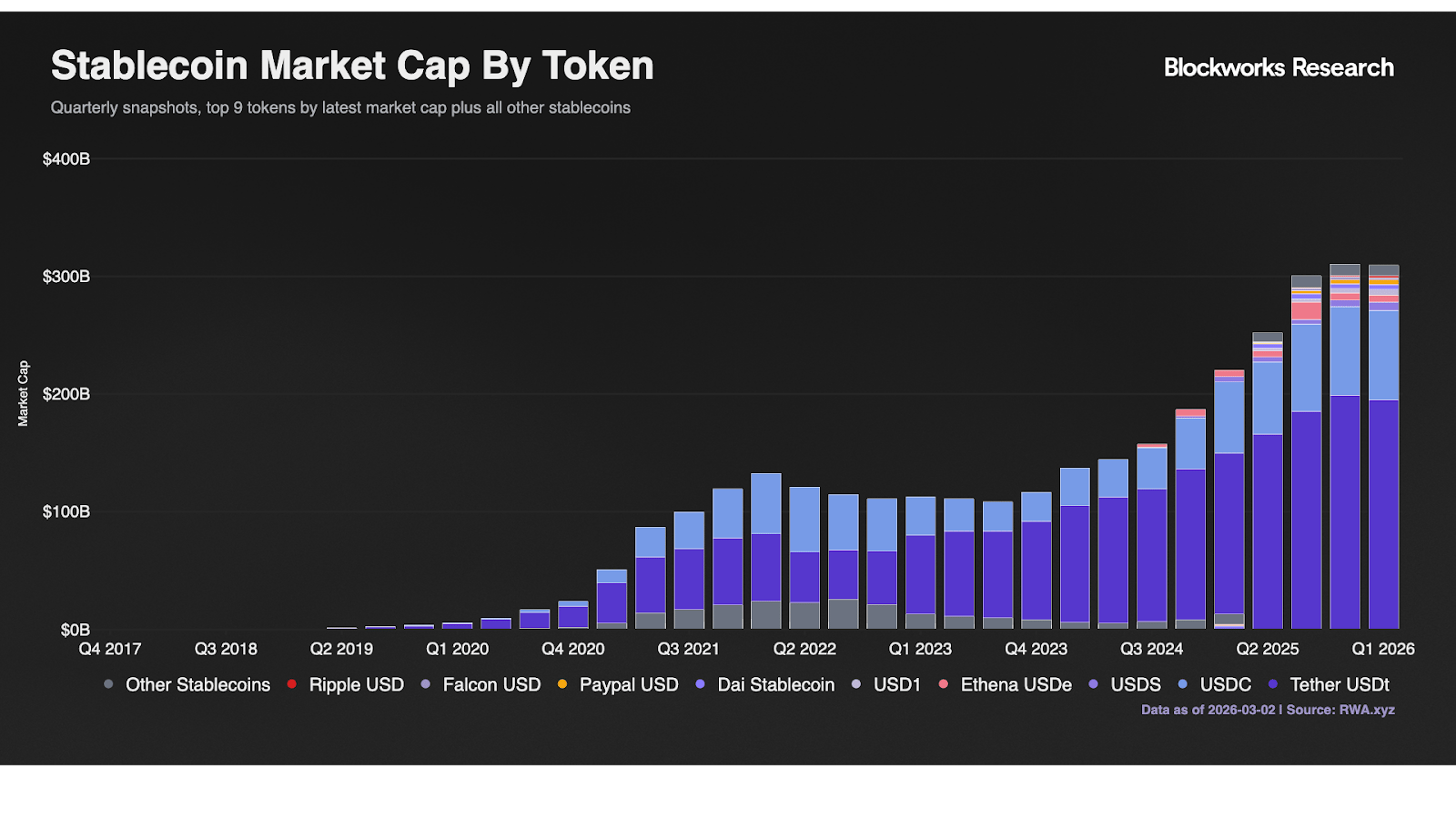

Mastercard’s agreement to acquire BVNK is the clearest sign yet that the next institutional crypto push is not just about wrapping BTC for mainstream investors; it is about owning the infrastructure that moves digital dollars. Mastercard agreed on March 17, 2026, to buy BVNK for up to $1.8B, and the company's framing was unusually direct: Stablecoins, tokenized deposits, and tokenized assets are all becoming large enough to matter to mainstream payments. Mastercard said digital-currency payment use cases reached at least $350B in 2025.

BVNK matters because it’s not a trading venue or a treasury company. It’s payments plumbing. Mastercard highlighted the fact that BVNK's platform enables sending and receiving payments across 130+ countries and across major blockchain networks. That’s a very different bet from another ETF filing or another treasury allocation headline. Mastercard is effectively saying the bigger opportunity sits lower in the stack — at the layer where money movement, merchant acceptance, payouts, remittances, and B2B flows get stitched together. Stablecoin supply is effectively at all-time highs; a deal like this reinforces the idea we’re still in the early stages of this transition.

PayPal’s recent PYUSD expansion reinforces that point from the distribution side. Extending PYUSD into 70 markets beyond the US is interesting, not because it proves stablecoins are “winning” some ideological debate, but because it shows a mainstream consumer-fintech platform believes stablecoins belong inside the product, rather than outside. If Mastercard is buying infrastructure and PayPal is widening distribution, the takeaway is that incumbents increasingly want stablecoins to live inside their own user experience and compliance perimeter.

The same logic is now showing up in capital-markets plumbing. DTCC, alongside Clearstream, Euroclear, and BCG, used a March white paper to argue that interoperability is the main bottleneck for digital asset securities. That is an important shift in tone. The conversation is moving away from whether tokenized markets are real and toward what kind of neutral infrastructure they need to scale. Specifically, the DAS-to-fiat currency settlement process will face multiple interop frictions across different stages and participants.

That also changes who the market should watch. A card network can attack merchant acceptance and payouts. A fintech wallet can own consumer distribution. A market utility can shape the standards for tokenized securities settlement. Those are different choke points, but they all sit on the same map.

Although Mastercard’s BVNK deal is one discrete event, it captures a broader transition: Incumbents are moving from crypto exposure to crypto rails. They don’t need to become crypto maximalists to do that. They just need to decide that stablecoin settlement, tokenized cash, and onchain distribution are too important to leave to third parties.

— Daniel

Justin Drake frames post-quantum security as a near-term design problem rather than a distant science-fiction tail risk. The strongest part of the conversation is not the alarm around Bitcoin's dormant coins, but the concrete roadmap. Drake says Ethereum could finish its post-quantum work by 2029, ahead of his personal 2032 estimate for a cryptographically relevant quantum machine. That makes the episode useful because it treats quantum less as a talking point and more as an engineering and governance problem that both Ethereum and Bitcoin will eventually have to answer.

In his recent book The Making of a Permabear, co-authored with Edward Chancellor, Jeremy Grantham reflects on his career and the hard-won investment lessons learned along the way. The conversation traces his journey from a frugal upbringing in wartime Yorkshire, where he developed a love for numbers and investing, through founding Batterymarch and GMO, the golden era of value investing, and the painful lessons of the dot-com bubble. It also covers his framework for identifying bubbles, the challenges of career risk, his views on the current AI boom, and his major philanthropic work on environmental issues paired with the foundation’s investment strategy.

Jonathan Wellum’s case is that investors should stop treating the current tape as a normal pullback and start thinking in terms of a broader retrenchment driven by higher energy costs, sticky inflation, rising rates, and a highly indebted global economy. That does not make it a crypto-specific piece, but it is timely and relevant because it explains why Monday's relief move may not settle the bigger macro question. The practical value here is his emphasis on position sizing, liquidity, and avoiding reactive trading when the fundamental backdrop is still deteriorating.

Ask ten investors what a neobank is and you'll get roughly the same answer: an app with digital-first, mobile-only, bank-like functions. Ask ten consumers which app they actually use and the answers get a lot more interesting.

The central question for stablecoin-first neobanks is how to expand beyond the crypto-native base. Neobanks that succeed will likely be defined less by feature sets than by who owns the user’s primary relationship with money.

This report groups the neobank landscape into three origin-based archetypes, analyzes the moats and unit economics of each, and discusses leading apps like Chime, KAST, MercadoPago, Nubank, Revolut, SoFi and more.