- 0xResearch

- Posts

- Maple's 2026 catalysts

Maple's 2026 catalysts

Resilient inflows and an onchain securitization vehicle

Daniel Shapiro & Carlos

March 03, 2026

Hi all, happy Tuesday! The week started with a risk-on reset: BTC ripped, gold slipped, and breadth across crypto was unusually wide.

Today, we dive into Maple’s fundamentals following its recent tokenholder call — highlighting resilient inflows, softer loan origination, and a clear roadmap for 2026 catalysts.

BTC surged 4.8% on Monday while gold slipped 0.7%, a 5.5-point reversal from last week’s dynamic, when gold led and BTC lagged. The S&P 500 (+0.9%) and Nasdaq (+1.0%) posted modest gains, meaning crypto outperformed equities by nearly 4x. After Friday’s panic bid into safe havens on Iran strike headlines, Monday’s session suggests markets are pricing a contained conflict rather than a broadening one.

The macro calendar was quiet, but the backdrop was not. Oil remains elevated after last week’s 8.5% surge, and PPI already surprised hot (0.5% vs. 0.3% consensus). Yet equities and crypto rallied through it. The implication: Unless Hormuz disruptions escalate further, traders are treating the geopolitical premium as fully priced for now.

Breadth across crypto was the standout. All 24 BWR sector indices closed green, with Crypto Equity Cohort 2025 leading at +10.4%, followed by Lending (+7.7%) and ETH Top 10 (+7.7%). Even the weakest sectors, Gaming (+1.9%) and Modular (+1.9%), held positive. That kind of unanimity is rare after a week when most baskets fell 3−6%.

The quality tilt within the green is worth noting. Lending, DeFi (+5.6%) and Revenue Top 10 (+4.7%) all outpaced speculative baskets like Meme (+2.6%) and DePIN (+2.4%). Capital rotated into fundamentals rather than narrative. The spread between the best and worst sectors was 8.5 points, wide enough to suggest conviction rather than indiscriminate short covering. If BTC can sustain above $69,000 and gold continues to fade, this looks like the start of a broader risk re-engagement rather than a dead-cat bounce. Watch whether Tuesday’s session confirms the breadth or narrows back to a handful of names.

— Daniel

Maple: Resilient inflows, upcoming catalysts

Last Thursday, Maple hosted its Q1 tokenholder update, highlighting early-year traction and key catalysts for Q2 and the rest of 2026. While SYRUP is down ~28% year-to-date, it remains the only token in our Lending index with positive year-over-year performance (~70%) alongside Sky. That divergence makes this a good moment to revisit Maple with a data-backed look at its fundamentals.

Maple’s AUM has fallen to $3.8 billion, down 23% from its late-October 2025 peak of $4.97B and down 17% year-to-date. But the headline masks a meaningful split by pool: SyrupUSDC and syrupUSDT inflows have shown notable resilience, while the overall drawdown has been driven largely by asset-price declines (loan collateral) and a near 70% contraction in the Maple Institutional KYC’d, permissioned secured-lending pool.

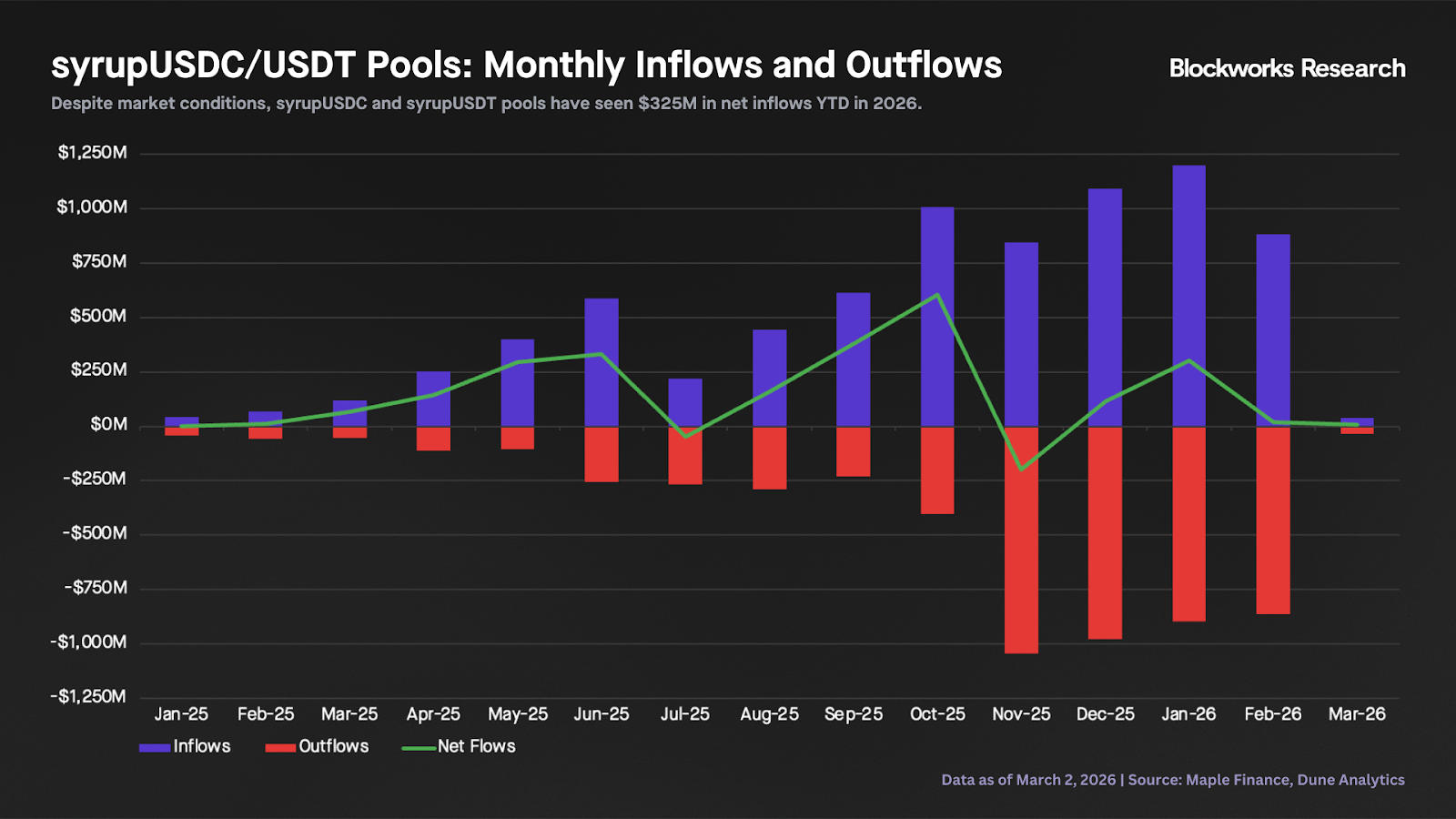

To strip out noise from loan collateral values, we can focus on net flows into the syrupUSDC and syrupUSDT pools. The chart below shows daily inflows and outflows year-to-date. Feb. 5−6 stands out as a clear outlier: Following BTC’s largest daily drawdown since FTX, the pools saw combined net outflows of more than $220 million.

That said, despite the market downturn and heightened volatility, the syrupUSDC and syrupUSDT pools still finished February with positive net inflows of $17M. Year-to-date, they’ve attracted $325M in net inflows in 2026.

Looking ahead, Maple plans to keep strengthening capital sourcing by distributing its yield products (syrupUSDC/USDT) across CeFi and fintech channels. The team said its first exchange-earn program is imminent and that it aims to sign three fintech partners by the end of Q1 2026. While fintech integrations can be slower to close given heavier compliance requirements, they could be a meaningful demand driver, with Maple projecting $500M−$1B of fintech-sourced capital by year-end.

While capital sourcing has remained strong, Maple has struggled on the capital allocation side, with reduced pool utilization. As weaker market conditions have reduced demand for leverage, outstanding loans have fallen nearly 50% year-to-date, from $1.6B to $850M.

In turn, this has pushed syrupUSDC/USDT 30-day trailing APYs to all-time lows. Even so, their yields still sit above stablecoin borrow costs across many DeFi venues, Aave included, as shown in the chart below. That spread matters since it means it’s still profitable to loop syrupUSDC/USDT to earn levered yield. It’s also been a major demand driver, with more than $550M of inflows since Maple’s expansion onto Aave.

In 2026, Maple aims to evolve from being just a lender into a more diversified asset manager. This will enable the protocol to deliver attractive, durable yields across various market environments. To get there, the team plans to build in-house trading capabilities (e.g., stablecoin arbitrage strategies) and expand into securitization. Maple said it is launching its first onchain-originated securitization vehicle in the coming months, where it will arrange and structure the deal and serve as the senior financier. As they replicate the model, this expansion can open the door to a new pool of institutional capital.

— Carlos

Cosmo Jiang and Sam Lehman from Pantera argue that as AI agents become true economic actors, legacy payment rails won’t work for agent-to-agent commerce because they rely on human identity, banking hours, and legal enforcement. They claim blockchains become critical at full autonomy – at which point agents can’t “borrow” a user’s credentials – and point to early signals like OpenClaw’s rise, increased Solana activity, and Coinbase’s x402.

The core drivers are three constraints: verifiable agent identity and portable reputation, programmable micropayments for high-frequency workflows, and deterministic enforcement via smart contracts. They conclude agentic commerce could create massive machine-native settlement flows and become a major tailwind for blockchains.

RWA.xyz published a primer arguing that allocation vaults are becoming the key distribution rail for tokenized assets, because they plug RWAs into DeFi lending in the same way a prime broker’s margin desk plugs collateral into financing. A risk curator underwrites which tokenized assets can be used as collateral, sets parameters, and allocates stablecoin liquidity on top of protocols like Morpho, Kamino, and Aave — unlocking a leverage loop that creates borrowing demand and yield, and can scale via distribution platforms like Coinbase.

Fasanara’s mF-ONE case study illustrates the playbook for private credit: make the token composable, engineer liquidity into the structure, work with a credible risk manager, and define liquidation exit paths upfront as tokenized markets move toward a distribution inflection point.

DAS NYC's lineup is bringing the biggest names in finance to the stage.

Don't miss the institutional gathering of the year — this March 24−26.