- 0xResearch

- Posts

- Intel “partnership”

GM all, and happy Thursday!

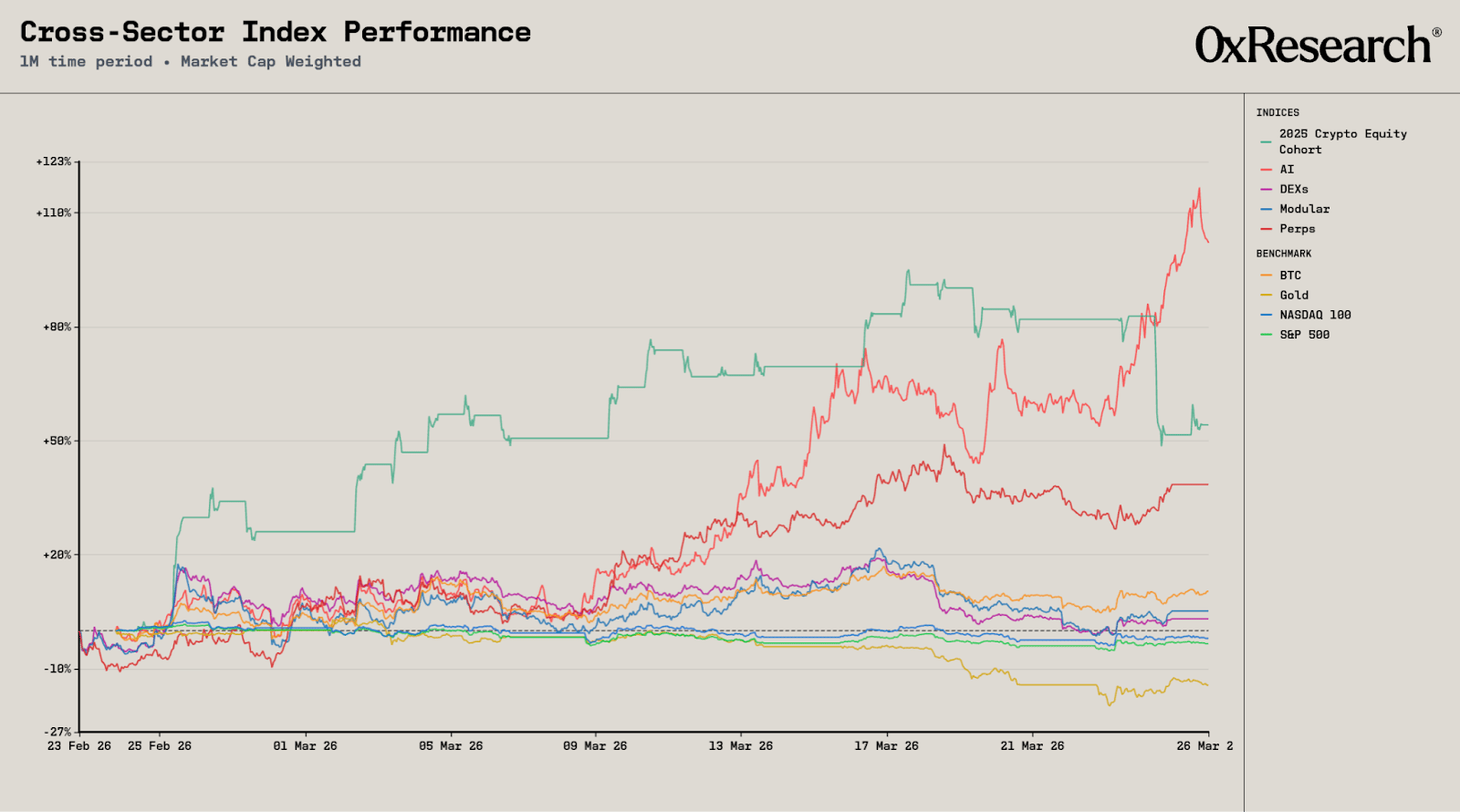

Crypto markets reversed lower overnight, with BTC, ETH and SOL all selling off sharply on the day. Beneath the surface, however, dispersion remains the dominant theme, with a sharp unwind in crypto equities led by CRCL contrasting against continued strength in AI. The market remains narrow, with flows concentrated in select narratives rather than broad-based participation.

At the same time, price action continues to highlight a disconnect between fundamentals and narrative. Targon’s Intel-related announcement drove a significant re-rating in SN4 despite limited evidence of a true partnership, reinforcing that branding and perceived validation can still drive flows.

Bitcoin traded lower on the day, down 3.2% to ~$69.4K, with ETH (−5.4% to $2.07K) and SOL (−5.3% to $87.7) underperforming on a relative basis. The move comes after a muted weekly trend, with BTC roughly flat (−1.5% 7d), while SOL continued to sell off among large caps (−2.6% 7d), suggesting the market is not yet ready for beta rotation back into higher-volatility assets.

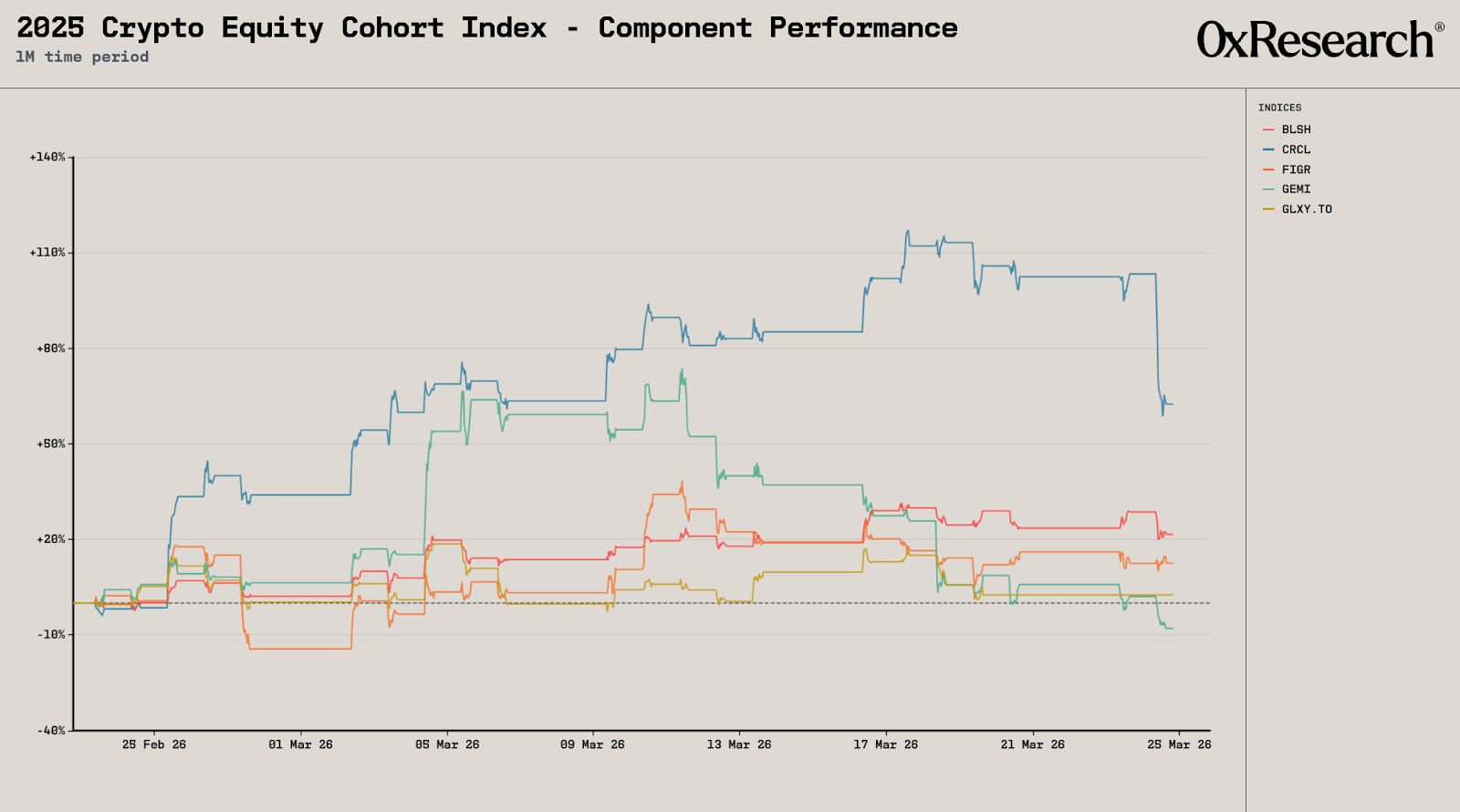

Across sectors, dispersion remained elevated, with a sharp reversal in the 2025 crypto-equity cohort driven primarily by CRCL. Circle had been the dominant contributor to index performance: It peaked above +100% on the month before a sudden drawdown erased a meaningful portion of gains into the final week, dragging the broader cohort lower.

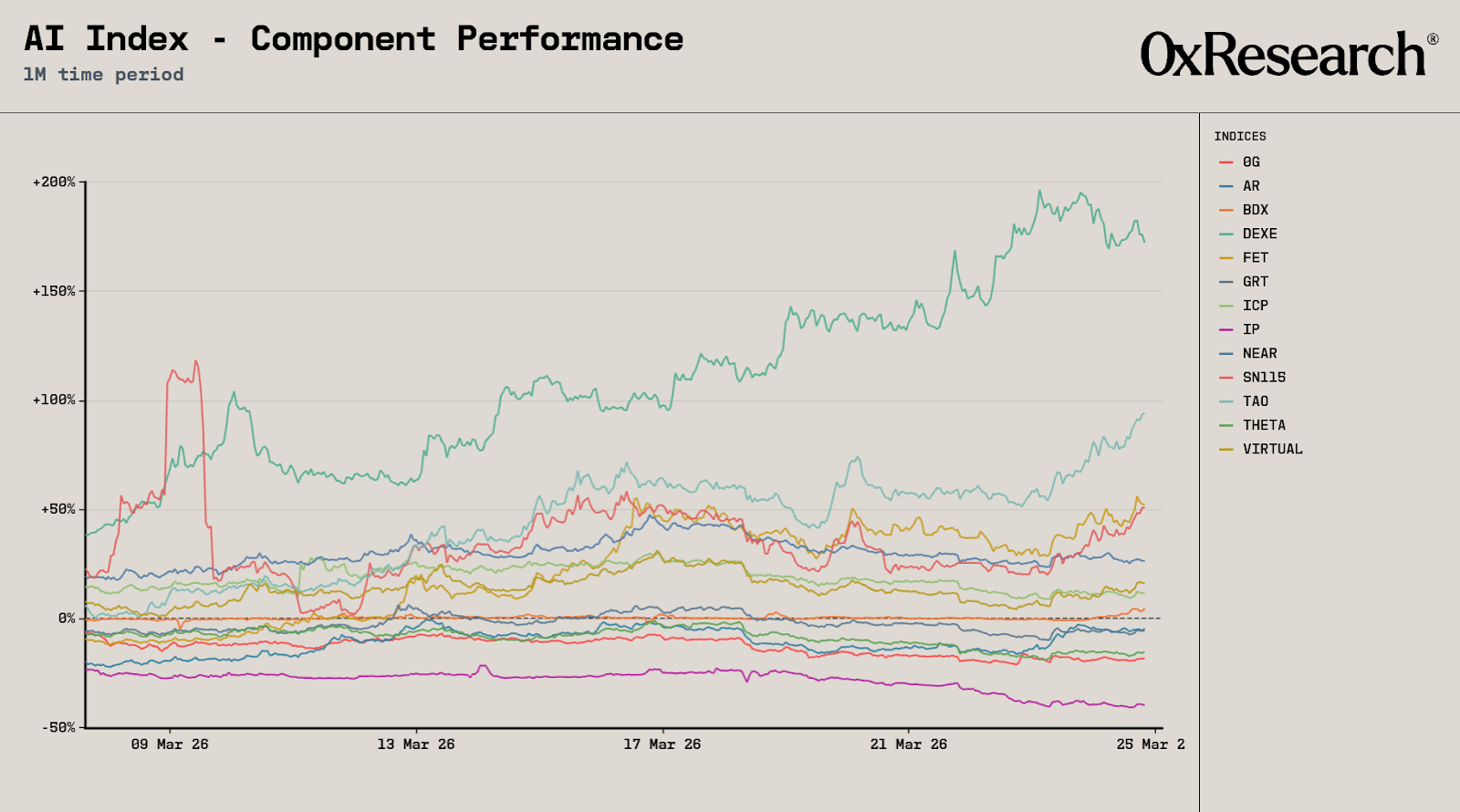

In contrast, the AI index maintained strength, with leading names continuing to trend higher and hold gains despite volatility, reinforcing AI as the primary locus of momentum.

Perps, DEXs and modular sectors showed incremental strength but failed to sustain breakout momentum, reflecting steady but unspectacular trading activity. Meanwhile, gold continued to outperform BTC on a relative basis over the period, and equities maintained a bid, extending the trend of crypto lagging traditional risk despite episodic rallies.

Separately, policy attention on tokenization continues to build, with the House Financial Services Committee holding a hearing yesterday on “Tokenization and the Future of Securities.” Lawmakers focused on regulatory gaps, custody frameworks and market structure, as tokenized RWAs have scaled to ~$26B globally, including over $11B in Treasuries. While institutional infrastructure from players like DTCC, Nasdaq and BlackRock continues to advance, the discussion highlighted the importance of translating backend efficiency gains into tangible value for retail users.

The key takeaway is a market that is stabilizing at the headline level but still lacks breadth underneath. Capital continues to rotate into a narrow set of outperformers, with idiosyncratic drivers like CRCL increasingly dictating index-level moves. A sustained move higher likely requires participation to broaden beyond AI and select equity-linked names into core infrastructure and DeFi. Separately, while tokenization has cleared the institutional-credibility hurdle, broader adoption will depend on whether it can deliver differentiated access and user experience rather than incremental improvements to existing financial rails.

— Nick

Introducing Blockworks Investor Relations, an IR platform built for onchain businesses.

The latest Blockworks offering brings together analytics, a branded investor relations site, and integrated advisory support into a single platform. The result is a more efficient way to share your story, build trust with investors, and engage a global audience from day one.

If you’re building in crypto and want to upgrade your investor relations function, we’d love to work with you. Book a meeting with the Blockworks team to get started.

Narrative inflation vs. reality

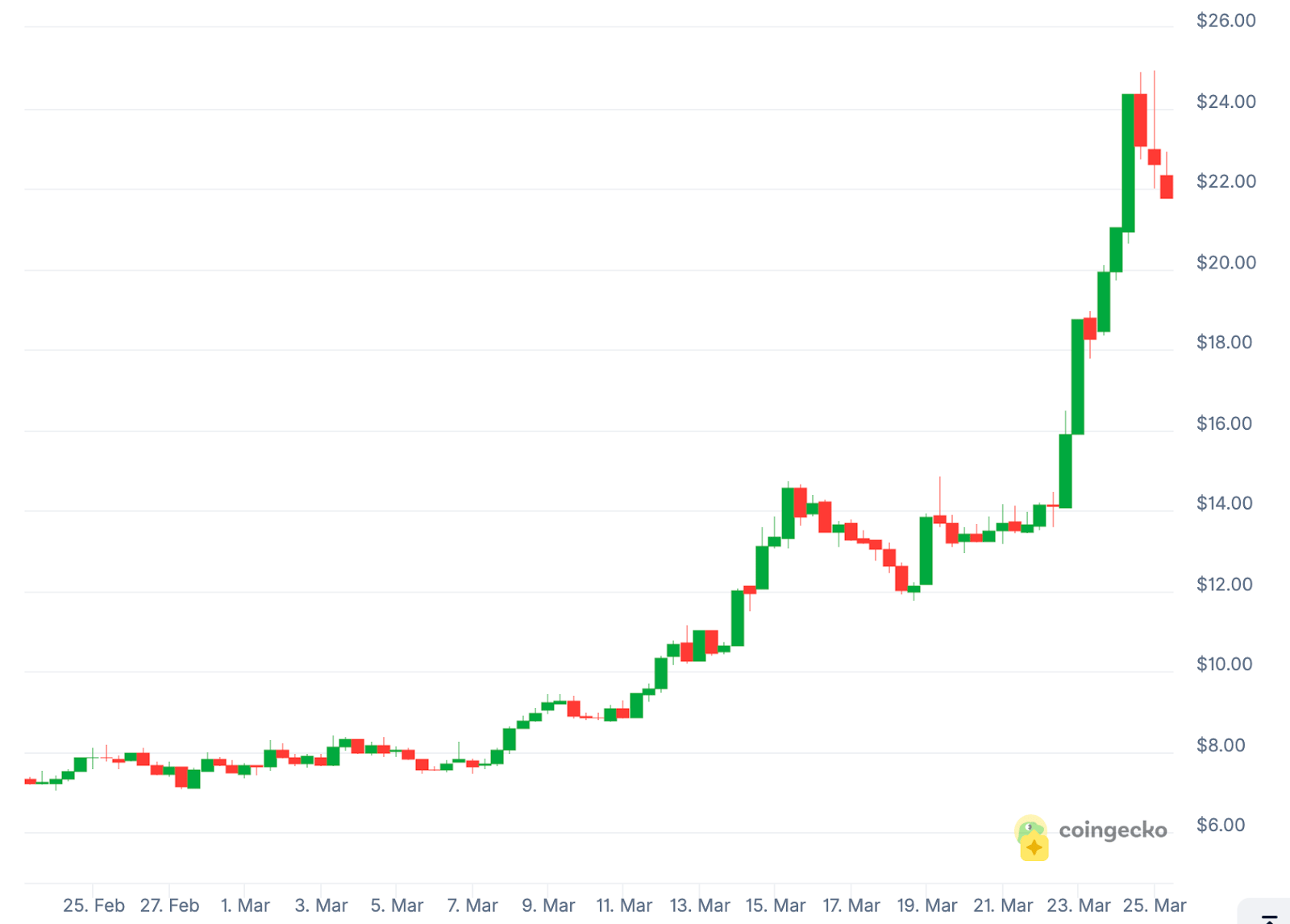

Bittensor subnet Targon recently promoted a whitepaper “written alongside Intel,” framing it as a meaningful partnership. The paper was published on Intel’s community DevRel blog, a distribution channel that regularly features co-authored posts with external teams across enterprise security and infrastructure.

The Intel authors involved have published similar pieces with other projects in near-identical formats, pointing to a standardized developer-outreach pipeline rather than bespoke collaboration. In practice, these posts function as technical amplification and ecosystem support, not commercial alignment or product integration. Positioning them otherwise introduces a gap between perceived endorsement and actual relationship depth.

To be clear, the technical work itself is credible. The paper outlines a decentralized confidential-compute architecture using Intel TDX, Trust Authority, and NVIDIA Confidential Computing to provision encrypted virtual machines on untrusted hardware. The design incorporates attestation workflows, hardware-level isolation, and continuous verification, directly addressing the trust problem in decentralized AI infrastructure. This is a legitimate and non-trivial contribution to the design space.

What stands out, however, is that the market appears largely indifferent to these nuances. Prior to the announcement, SN4 traded at $15.14. It now trades at $21.49, implying a ~42% increase despite the ambiguity around the framing. Price action suggests that narrative momentum and exposure still hold weight over diligence on relationship quality or distribution channels. Crypto continues to conflate brand adjacency with validation, using recognizable names to signal traction.

In a market that has otherwise rotated toward fundamentals, pockets of reflexivity remain, where branding and perceived validation can drive flows independent of underlying substance.

— Nick

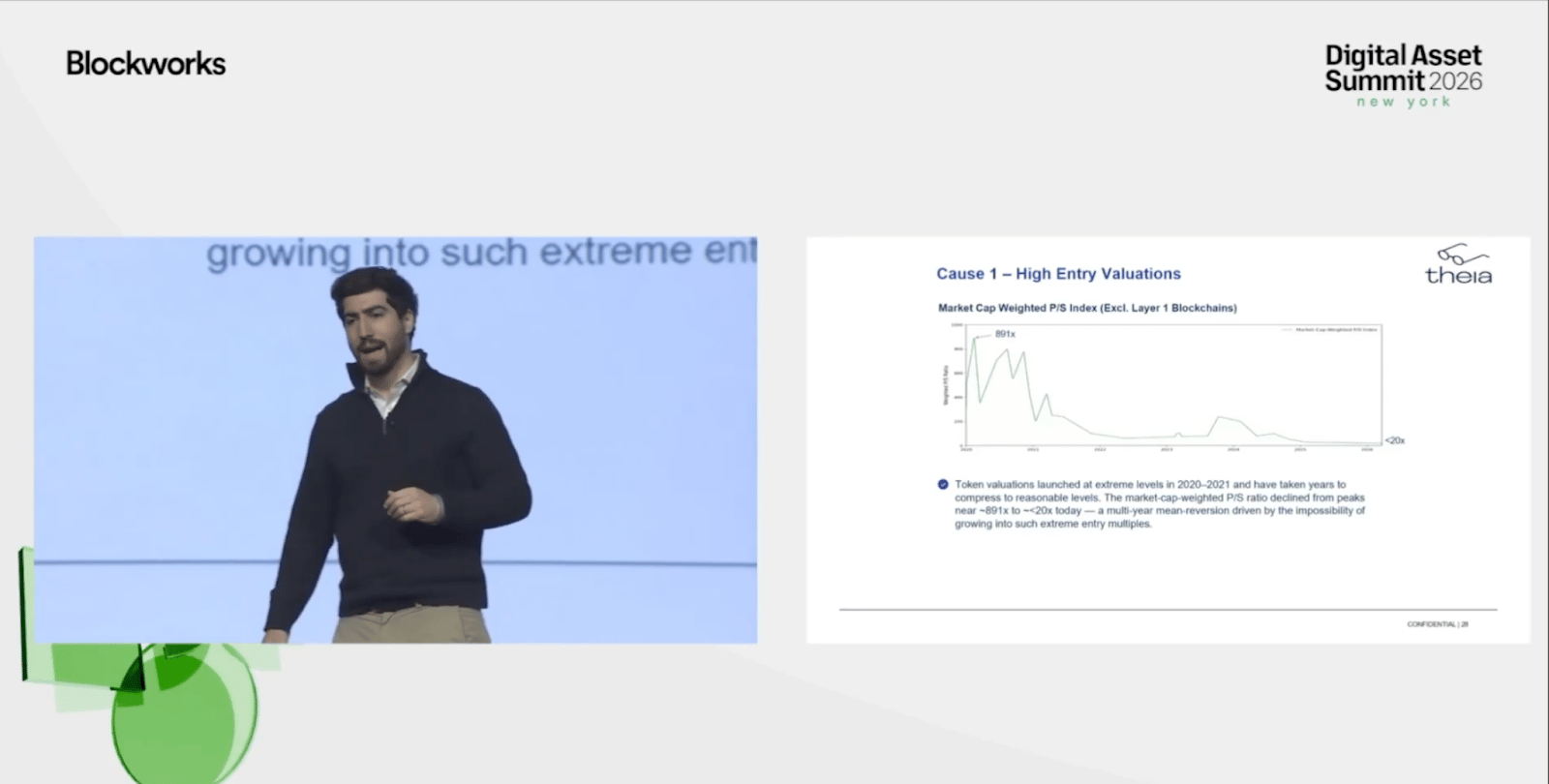

At DAS NYC, Felipe Montealegre argued that the prolonged token bear market was primarily driven by extreme entry valuations, with application tokens reaching ~900x price-to-sales at peak versus ~100x during the software bubble. He noted that while software compressed to 10−20x, crypto valuations remained elevated between 100−200x for years, delaying a full reset. As of 2026, multiples have finally normalized to sub-20x, marking the first structurally-reasonable entry point for the sector.

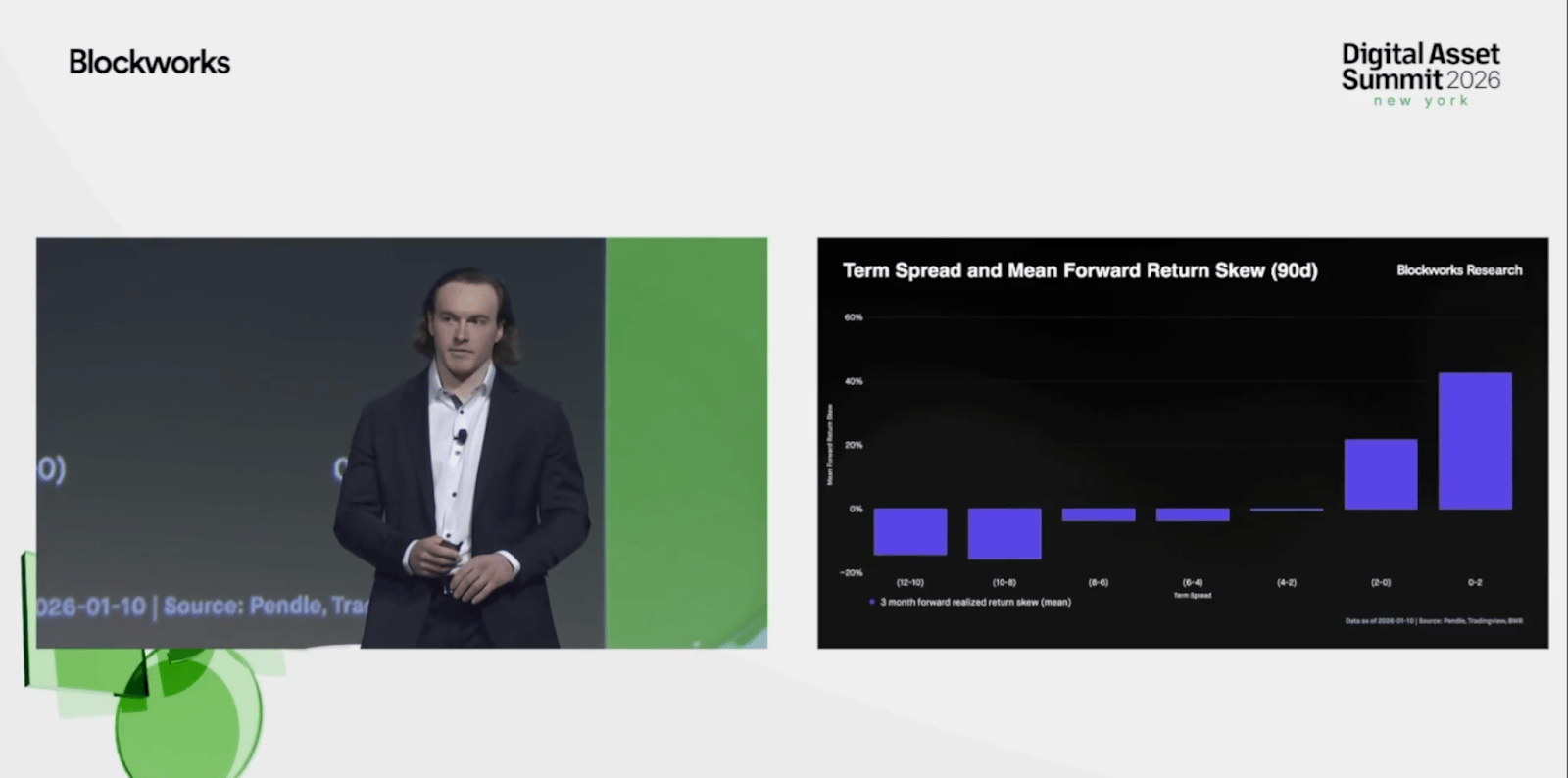

Blockworks Research analyst Luke Leasure analyzed the rolling term spread between back-month and front-month implied yields to track the slope of the onchain yield curve, showing a strong relationship with BTC forward returns. He noted that steep backwardation consistently preceded the weakest 90-day performance, while positive term spreads in contango regimes produced the strongest forward returns, with nearly all observations resulting in gains.

Luke also noted that sUSDe principal tokens exhibited the highest collateral utilization across onchain money markets, reinforcing their role as a core yield instrument and creating reflexivity between demand for carry and the shape of the curve, positioning the term structure as a forward-looking signal for BTC price, cost of carry, and broader market regimes.

Chase Barker of the Solana Foundation argues that while Solana has assembled the most complete onchain financial stack across spot trading, stablecoins, RWAs and users, it has failed to capture the largest revenue driver in crypto: perpetual futures.

He examined how perps consistently generate 4−6x spot volume, yet platforms like Hyperliquid still process 10-15x the volume of all Solana perps venues combined, with the gap driven less by demand and more by execution constraints, particularly around market microstructure, inconsistent ordering, and fee opacity that deters market makers, alongside a lack of competitive perps products to convert Solana’s existing retail base into sustained derivatives flow.

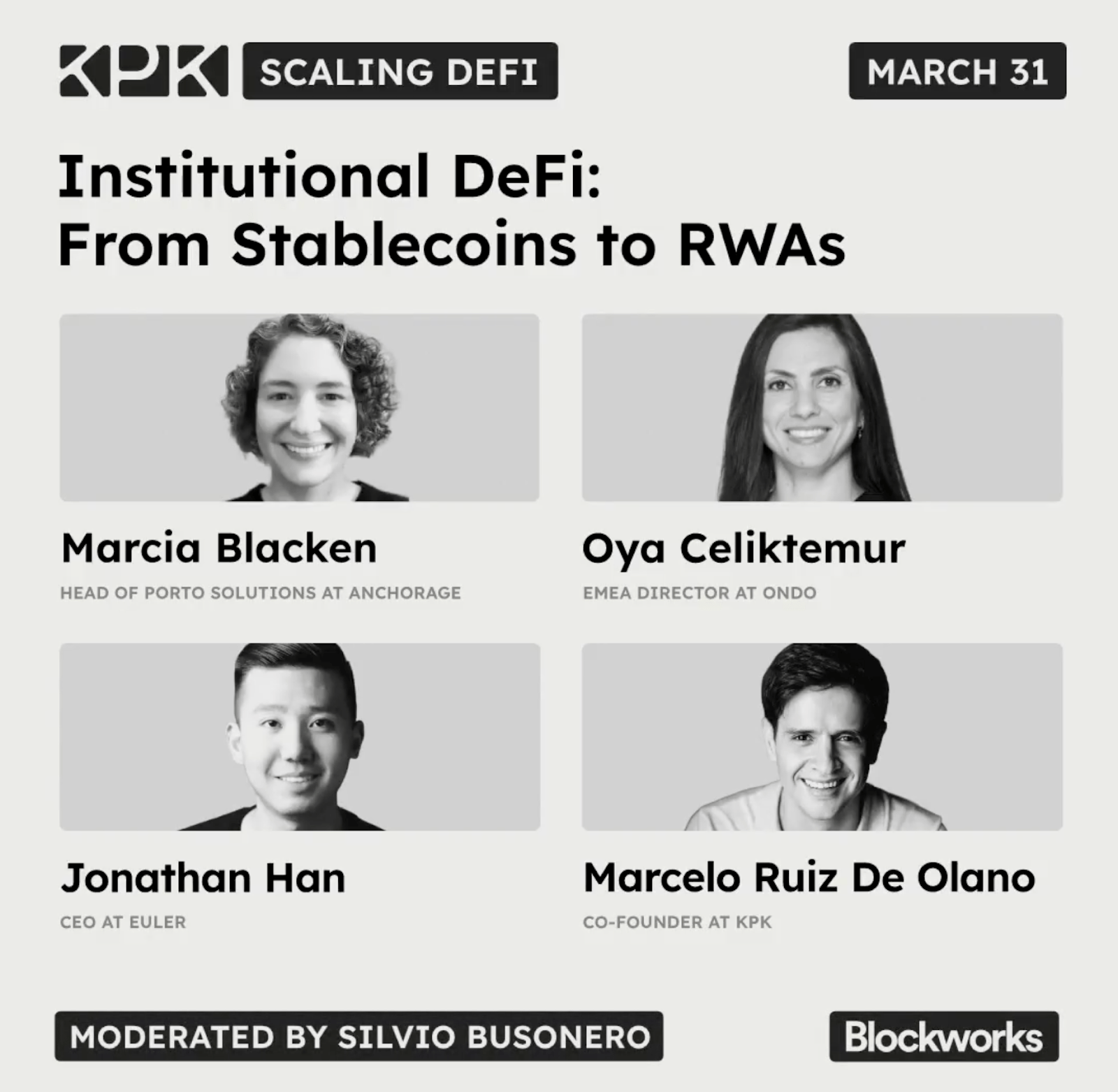

Join us for a live 0xResearch episode with the industry’s best and brightest from Anchorage, Ondo, Euler and KPK on March 31.

Our panelists will be diving into institutional traction, demand sinks, and remaining points of friction.