- 0xResearch

- Posts

- Hyperliquid's Next Move

GM, and happy Monday!

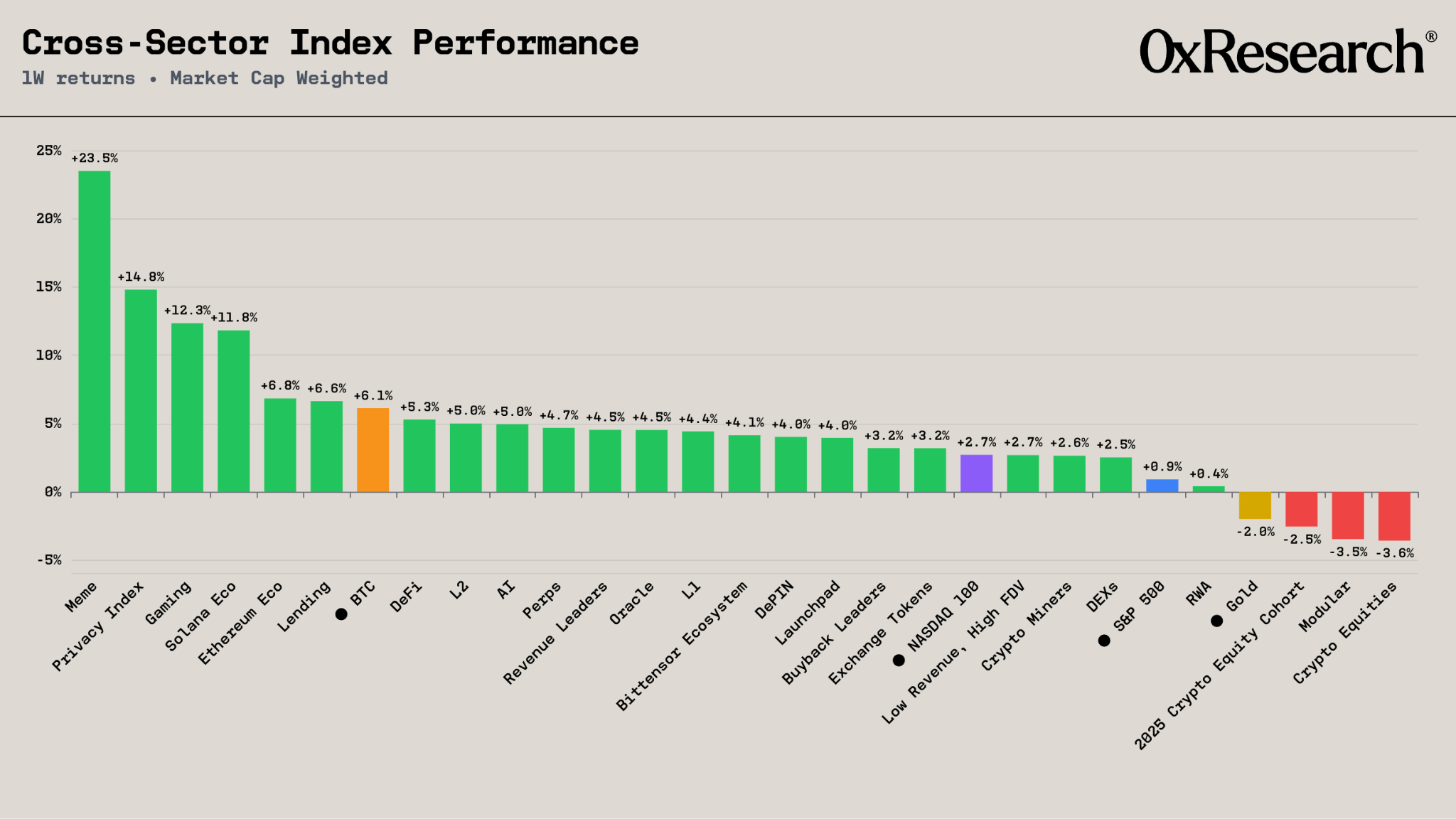

While traditional equities saw a risk-off weekend and oil caught a bid due to renewed Hormuz disruption risks, the past week was broadly green across crypto. The Meme and Privacy sectors were the clear standouts, leading the market alongside gains in Gaming and the Solana ecosystem.

In today's edition, we explore Hyperliquid's strategic evolution. We break down the shift from outsourcing new market creation under HIP-3 to its updated approach with HIP-4, where the platform aims to internalize and capture the economics of high-volume, canonical markets.

The last week was broadly green across crypto, with privacy and memes as the standout sectors. Memes led at 23.5% and the Privacy index put up 14.8%, with Gaming and Solana Eco clustered behind in the low double digits. BTC tracked the rally at 6.1% while TradFi grinded higher, with the NASDAQ up 2.7% and the S&P 500 up 0.9%. Crypto equities and modular were the sectors meaningfully down on the week.

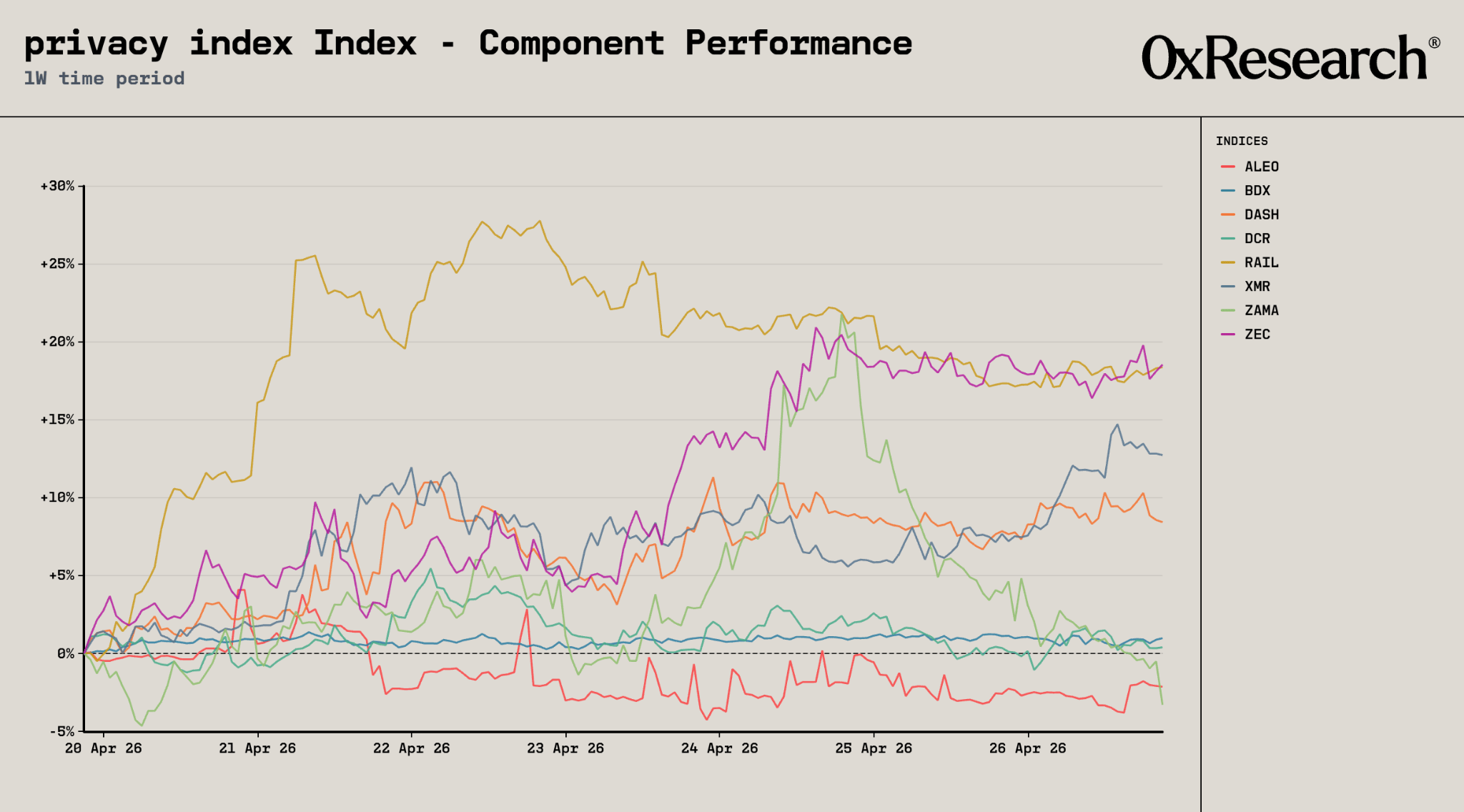

Inside the privacy index, ZEC and RAIL led the pack at roughly 18%, with XMR and DASH posting double-digit and high single-digit gains behind them. ZEC is typically a high-beta play to BTC moves, and BTC's 6.1% week amplified through the name, coupled with a Robinhood listing on April 24. RAIL rode the broader privacy bid without a specific catalyst, as sentiment lifted after Ethereum’s draft EIP-8182 was discussed, putting protocol-level privacy back in focus across the category.

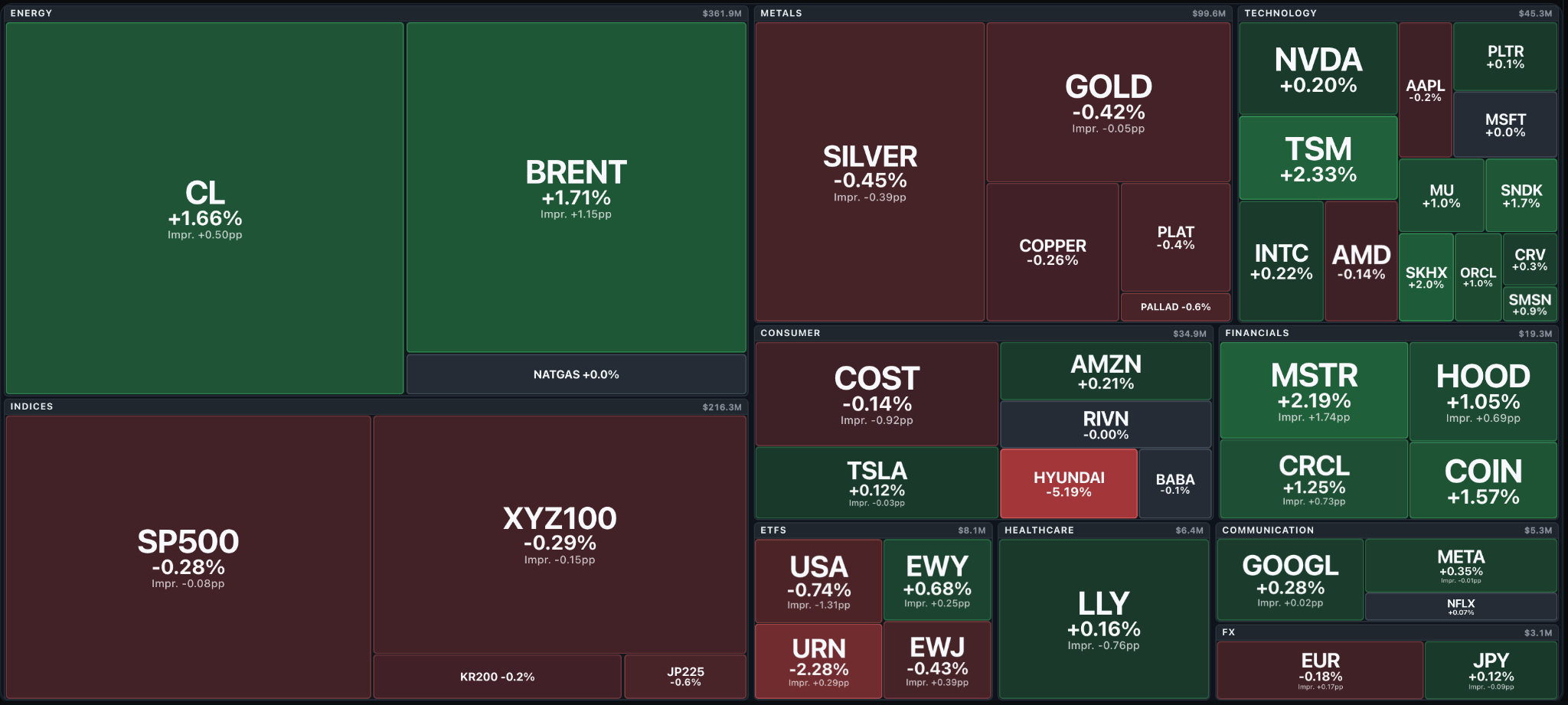

It was risk-off in equities and bid in oil over the weekend, with Brent and WTI both up around 1.7%, while the S&P 500 and tech-heavy benchmarks ticked modestly negative. The energy bid traces to renewed Hormuz disruption risk: Brent has held above $105 as the Strait of Hormuz remains effectively closed amid stalled US-Iran peace talks, with the IEA describing the disruption as the most severe oil supply shock in history. Crypto-adjacent equities were the bright spot in financials, with MSTR up 2.2%, COIN 1.6%, and CRCL 1.3%.

— Sam

Is Hyperliquid Reclaiming Value From Deployers?

Following HIP-3, Hyperliquid largely outsourced new market creation to third-party deployers. This shifted Hyperliquid from a fully integrated exchange model, closer to Binance or Coinbase, toward a more modular exchange stack, closer to Nasdaq’s position within the broker / market / clearing infrastructure.

The result has been a rapid migration of listing activity to deployers. Of the 104 new markets listed in 2026, 98 came from HIP-3 deployers, leaving Hyperliquid-operated listings at only 5.8% of new market supply. HIP-3 markets now represent 37.5% of total Hyperliquid volume. As Hyperliquid expands beyond crypto into equities, commodities, indices, and other RWA markets, that share should continue to rise.

However, while HIP-3 deployers have been effective in expanding market coverage, they are also expensive. Under the HIP-3 model, deployers earn 50% of fees generated by their markets. Is that value justified, or is it being leaked?

Hyperliquid still owns the exchange infrastructure, settlement layer, collateral base, and most of the flow, with only 3.75% of volume coming from third-party frontends (builder codes). The deployer role can be reduced to two functions: 1) identifying relevant markets to list, and 2) managing oracle / mark-price infrastructure safely. For niche markets, both functions matter. But for obvious high-volume assets, such as gold, silver, crude oil, the S&P 500, Nasdaq, or top equities, market selection is less differentiated. Oracle setup remains critical, but it is not obvious why Hyperliquid could not internalize that function for the largest and most standardized markets, rather than share a material portion of future non-crypto perp economics with third-party deployers while retaining complete ownership only over its existing crypto products, which should become a smaller share of total volume over time.

The obvious counterargument is that this is necessary for Hyperliquid to allow organic competition, since the exchange layer must remain neutral. However, Hyperliquid has already shown it is willing to adopt a dynamic role: provide exchange infrastructure while competing in vertical layers, as we saw when it added HIP-3 markets to its own frontend, removed staker discounts for builders, and launched a mobile app to prioritize its native frontend versus builder codes. HIP-4 looks like the same vertical-integration logic applied to deployment.

Unlike HIP-3, where new market creation was outsourced from the start, HIP-4 begins with Hyperliquid-led canonical markets. The stated initial mainnet release is 1-day binary markets on BTC and HYPE, and Hyperliquid has said that canonical markets based on objective settlement sources will be deployed first, denominated in USDH, with permissionless deployment extended later pending user feedback.

This gives Hyperliquid the opportunity to internalize the most obvious, high-volume, objective markets first, including BTC/HYPE binaries and potentially other standardized price-linked outcomes, before opening the long tail to third-party deployers. The strategy is straightforward: keep canonical markets in-house to capture blue-chip economics, and outsource niche or subjective markets to deployers who add real value through curation, oracle design, liquidity coordination, and settlement credibility.

Hyperliquid's recent moves all point one way: capture more revenue, pull users onto the native platform, and act as the dominant market layer while still letting others build on top. The upside is more revenue capture for Hyperliquid; the cost is sharper competition for deployers and builders.

— Shaunda

Blockworks researchers break down the mechanics and systemic fallout of the recent bridge hack. The panel explains that the attacker exploited KelpDAO's vulnerable 1-of-1 signature scheme to mint unbacked rsETH, which was then weaponized on Aave V3 to borrow $193 million in WETH. The researchers assign shared blame across KelpDAO's poor bridge setup, LayerZero's default configurations, and Aave's failure to flag the underlying collateral risk. Moving forward, Kelp DAO must decide whether to socialize the losses (a ~17% markdown across all holders) or isolate them to Layer 2s, while Aave's $50M Umbrella module remains vastly undercapitalized to cover the bad debt. Attributing the exploit to the North Korean Lazarus Group, the panel concludes that this crisis will force the DeFi industry to shift away from accepting complex collateral in unified pools and move toward vertically integrated, battle-tested platforms like Maple and Sky.

Jarry Xiao, co-founder of Phoenix, announced the public launch of the team's Solana perp DEX, framed as "Act I" of a longer roadmap. The trade page consolidates five elements (position, limit orders, liquidation price, funding/volume/OI, and orderbook depth) into one view, with Phoenix claiming the highest SOL liquidity of any Solana perp DEX at launch.

The architectural pitch is making a fully on-chain perp feel like a CEX through three abstractions: Privy embedded wallets remove browser extension signing, a sponsorship server pays all gas so users never have to think about holding and spending SOL, and the Phoenix contract supports native wallet delegation so traders use their primary wallet without plumbing. Deposits and withdrawals settle instantly, with explicit visualization of how liquidation prices shift on both sides.

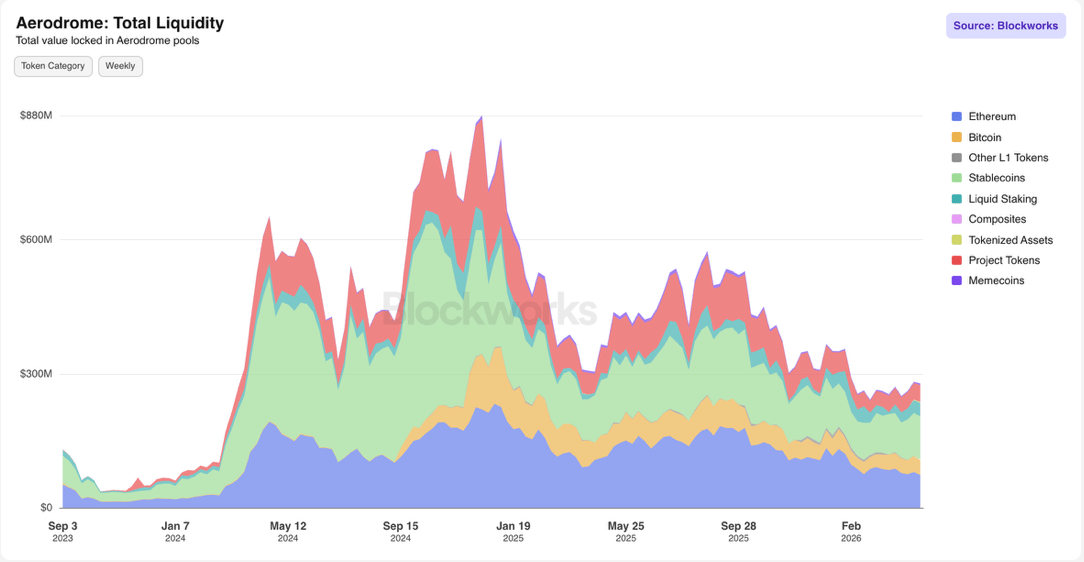

Aerodrome Finance is the dominant DEX on Base. Launched in August 2023 by Dromos Labs, the protocol was designed from inception to serve as Base's primary liquidity layer. Its product suite spans a constant-product AMM for stable and volatile asset pairs, and Slipstream, a concentrated liquidity module closely derived from Uniswap V3 that allows LPs to deploy capital within defined price ranges for improved capital efficiency.

Aerodrome holds ~$240M in TVL, with cumulative fees since launch exceeding $322M.

The protocol is preparing a major architectural upgrade, Aero/MetaDEX03, targeting a Q2 2026 launch that will merge Aerodrome and Velodrome into a unified cross-chain DEX and introduce MEV internalization as a new revenue stream.