- 0xResearch

- Posts

- 🦄 Hello Unichain

🦄 Hello Unichain

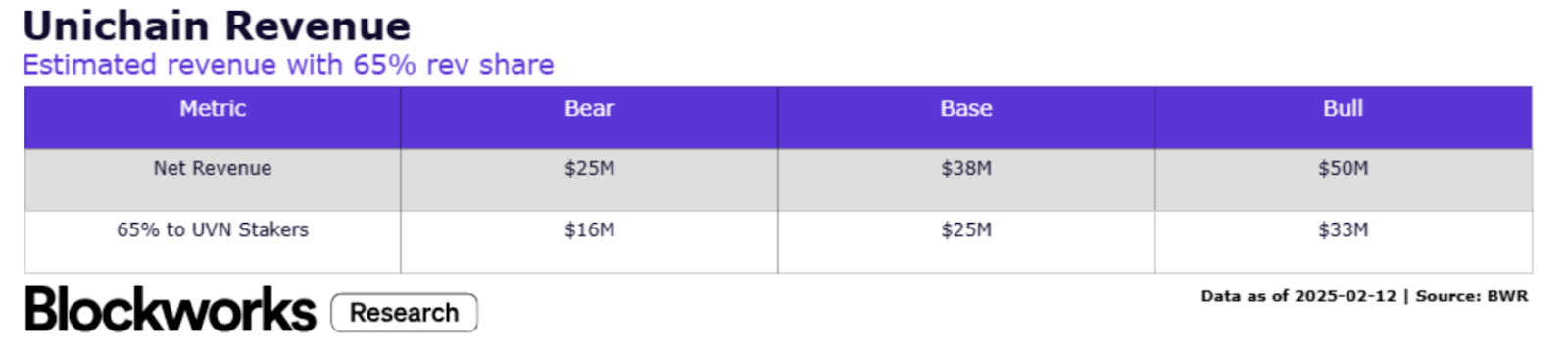

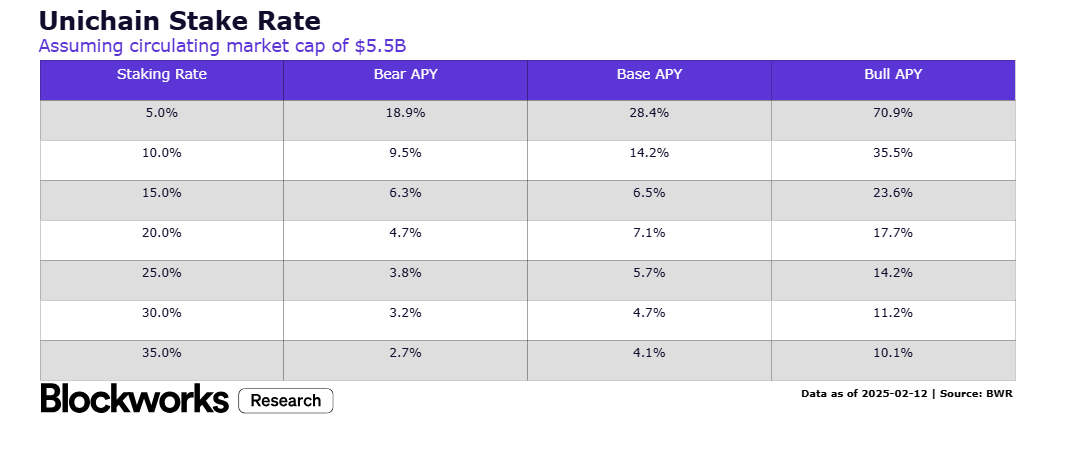

UNI holders accrue $33M in revenue

Brought to you by:

Does Ethereum need another L2? Unichain mainnet is here! Get excited for more interoperability problems UNI value accrual.

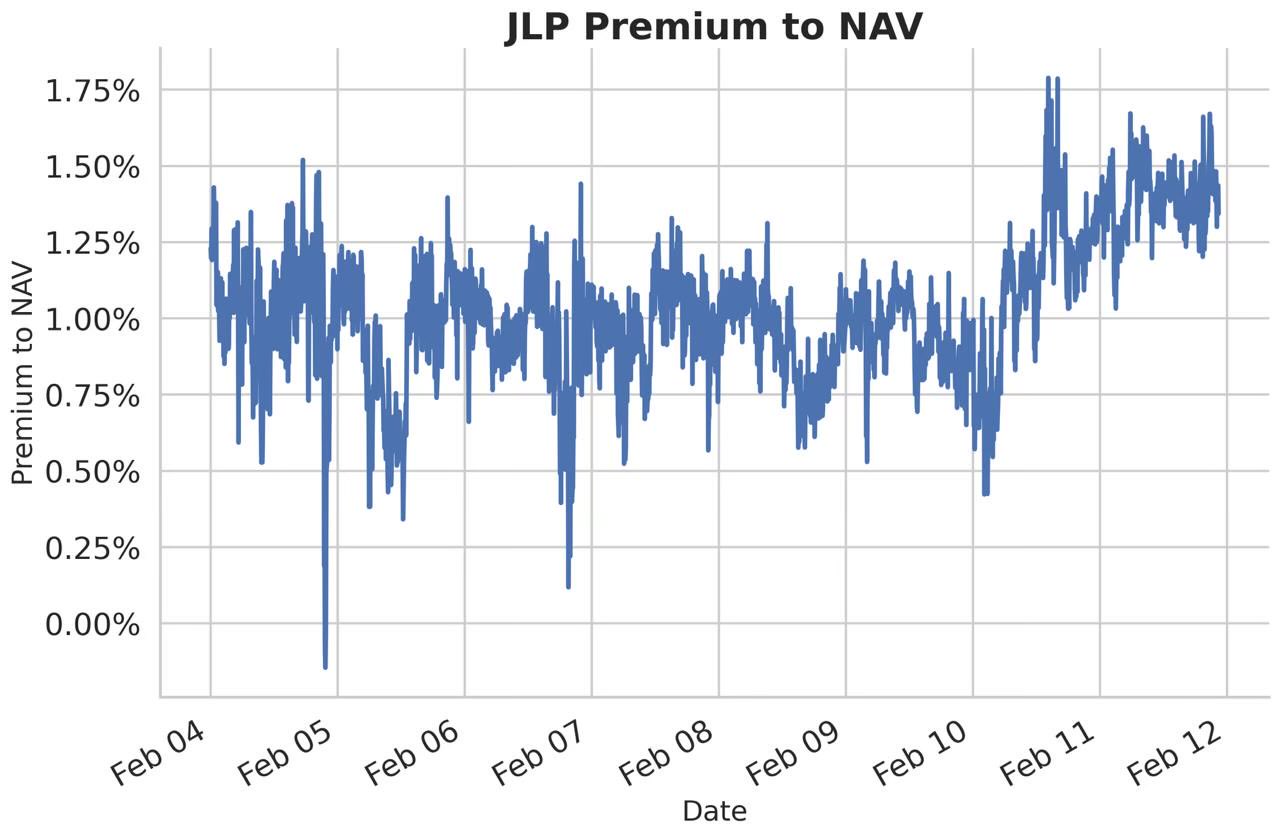

JLP trading at a premium:

Source: @y2kappa

With Jupiter’s Liquidity Provider (JLP) token minting currently paused due to the exceeded AUM cap ($1.77b TVL vs. $1.75b cap), demand has driven secondary market prices above net asset value (NAV). As shown in the above chart, JLP has consistently traded at a 1-2% premium over NAV in recent days, reflecting strong investor appetite.

The value of JLP is derived from a basket of assets in target proportions — 44% SOL, 10% ETH, 11% WBTC, 26% USDC and 9% USDT — along with profits and losses from traders on the Jupiter Perpetuals platform and 75% of the fees generated from trading activities.

Since new JLP tokens cannot be minted, the only way to acquire them is through the secondary market, where buyers are willing to pay a premium. However, burning JLP remains open and Kamino offers redemptions at NAV.

This dynamic will persist unless:

The AUM cap is raised.

Market demand cools.

More holders opt to burn JLP, increasing available supply.

For now, JLP holders benefit from strong market pricing, but those looking to buy should be aware of the premium.

Brought to you by:

SKALE, the gas-free invisible blockchain, is “Built Different” for mass adoption: high-throughput, scalable, and fair. As a network of interoperable EVM-compatible L1s, SKALE’s user experience focus has accelerated a strong ecosystem across gaming, AI, and more. Due to SKALE’s gas-free nature, blockchain can be integrated invisibly, creating accessible Web2-like experiences for users and developers.

SKALE has:

Over 50M UAWs

9 Games on the Epic Games Store

Saved Users over $9.5B on Gas Fees

Dive in to learn more.

Unichain mainnet is out

Four months after its initial announcement, Uniswap’s L2 rollup mainnet went live yesterday.

Despite its name, Unichain is a general purpose L2 rollup. At least a dozen applications have already been deployed on the chain, including Euler, Renzo, Morpho, Lido and more.

So it’s another L2. What makes Unichain different?

For one, Unichain has quicker finality at 200-250 milliseconds, a significant upgrade over Ethereum’s 12-second block time or most OP stack chains’ block time of two seconds.

Second, Unichain is a Stage 1 rollup right out the gate. This means a permissionless fault proof system has been deployed that allows anyone to verify or challenge transactions independently, unlike Stage 0 rollups such as Base.

When Unichain was first announced late last year, it threatened to exacerbate ETH’s value accrual problem. Why? Uniswap is still one of the largest gas guzzlers on Ethereum L1, which contributes to a higher burn rate of ETH i.e., value accrual.

The silver lining is that a significant number of v2 and v3 users will probably not migrate to Unichain immediately. Users are sticky. Uniswap v3 will have been live for four years in May and yet its v2 deployment still enjoys a deep moat of liquidity (~$1.5 billion in TVL).

Expecting Uniswap LPs and users to bridge to a rollup chain looks to be fraught with even more friction, let switching between frontends.

Peter Thiel famously said that customers accept switching costs when product innovation is at least a 10x upgrade from existing options, not mere incremental improvements.

Does Unichain, the L2 rollup, offer that tenfold improvement? I don’t think so. Perhaps Uniswap v4 and hooks do, but v4 is also already live on eight other chains.

After UniswapV4 launched, @base was the biggest adopter but now it appears most of the volume lies on Ethereum and @arbitrum.

We probably cross over $1B in (v4) volume traded in the next couple of weeks.

— Marc Arjoon 🟪 (@marcarjoon)

1:41 PM • Feb 12, 2025

Should the bulk of liquidity and users migrate to Unichain, however, it would at least appease one group of stakeholders: UNI token holders.

Last week, Uniswap Foundation announced a revenue-sharing structure that would allocate 65% of net chain revenue to validators and stakers on the Unichain Validation Network (UVN).

It’s hard to overstate the importance of this development.

For years, UNI token holders have lamented the lack of value accrual. The UNI airdrop was a “last resort” move that served to stave off the infamous SushiSwap vampire attack in 2020.

And it worked. Uniswap re-established itself as the top DEX. But then UNI existed as a meme token with no productive cash flows.

On a recent Bell Curve podcast, Felipe Montealegre of Theia Research likened UNI’s treatment as a “second class citizen” compared to Uniswap Labs equity.

So the UNI fee switch is finally here. How much should UNI stakers expect?

About $16 million to $33 million in annualized net revenue, Blockworks Research analysts Luke Leasure and Daniel Shapiro told me.

“Estimating the fees and APY that will accrue to UNI stakers on Unichain’s UVN requires a few assumptions. Firstly, the 65% of net earnings that accrues to the UVN are a function of base fees, priority fees and MEV paid to transact on the L2, less the expenses of posting data to the L1 and the Optimism Collective’s take rate on gross and net chain revenue. With this, the Base L2 may be the most appropriate comparison to estimate Unichain’s financials,” Leasure and Shapiro said.

“DEX activity is the largest driver of fees by a significant margin. Over the trailing 30 days, Uniswap did ~$100b in trading volumes, whereas Base is around $50b with around $100m in annualized net revenue. Assuming Unchain captures 9-25% of Uniswap’s volume, this would put Unchain L2 activity at 25% to 50% the activity of Base.”

Is the cycle over?

That’s the question on everyone’s minds. A significant chunk of market participants have either sold or derisked — or wishing they had. But is this the end, or just a period of exhaustion before the next leg up?

On the latest 1000x podcast, Avi and Jonah break down recent price action, sentiment shifts and key market dynamics. Bitcoin has barely moved, recently closing within a $100 band for multiple days — an unusual consolidation at the highs. Meanwhile, altcoins have suffered brutal selloffs, with many down 50-90% from their peaks. Even so, bitcoin’s resilience in holding its 100-day moving average suggests something different may be at play.

Avi challenges the traditional market cycle framing: It’s not just about "up or down" anymore, but asset-by-asset dispersion. Some alts continue to bleed out, while others, like LTC (on ETF speculation), show relative strength. ETF flows, particularly from BlackRock’s IBIT, continue to inject steady capital into bitcoin, potentially underpinning its price.

“Nobody really wants to touch altcoins right now, which could actually be a pretty good opportunity for the ones which have catalysts coming up,” Avi said.

Jonah concurred that “everybody’s super disenchanted…there’s really bad sentiment and pain and anguish out there about the alt market — I don’t think that’s bearish.” He looks to a stablecoin-focused bill in Congress as an upcoming catalyst to reignite interest.

Aside from sentiment in the dumps, Avi and Jonah see an asymmetric upside with traders sidelined in cash. If selling exhaustion sets in, the next move could catch many off guard. The big question: Are we in a slow grind higher, or is this just the calm before another storm?

— Macauley Peterson

|

|