- 0xResearch

- Posts

- 🟣 Happy HYPEgiving Day

🟣 Happy HYPEgiving Day

Plus, understanding perp dex dominance

Brought to you by:

Welcome back to 0xResearch. Here's what we’ve got for you today:

Hyperliquid airdrops

Chart: The evolution of perp dex volume

Recent Research: Arbitrum DAO grants

Hyperliquid airdrop hype

Hyperliquid, the largest perpetuals DEX by trading volume, launched its HYPE token today to (nearly) wide acclaim.

The HYPE airdrop stands out for two reasons.

For one, 31% (310 million) of the HYPE token supply is being airdropped, far higher than the average airdrop of a 5% to 15% token supply range. Secondly, Hyperliquid is unique as a non-venture-backed team which means there are no private investor allocations.

In what seems to be the most successful airdrop of the year thus far, HYPE is currently trading at a $1.7 billion market cap, and a $5.1 billion FDV. For comparison, dYdX, which was early to the dedicated DEX chain game, has a valuation of $1.1 billion.

Not everyone is happy about the airdrop, which required advance agreement of Terms and Conditions.

Source: Hyperliquid Discord

Thanks to seamless onboarding, gas-free trading, a sleek user interface and lightning-fast token listings, Hyperliquid has cemented its reputation as the premier perps DEX of 2024.

But Hyperliquid’s success comes from more than product innovations around its orderbook exchange.

Though Hyperliquid was originally a perps application on Arbitrum, it subsequently introduced a spot orderbook exchange and migrated its DEX onto a proof-of-stake layer-1 in March 2024.

The Hyperliquid L1 chain is powered by the HyperBFT consensus protocol and claims to support about 100K TPS. Unlike most other perps DEXs, Hyperliquid’s orderbook is fully onchain, earning a nickname of “onchain Binance” among its community. Others, such as Aevo, use an offchain or hybrid approach.

HYPE will likely be used for L1 staking and governance, adding to its positive perception as a “utility” token.

Since then, Hyperliquid has sought to leverage its DEX liquidity to bootstrap an entire financial ecosystem around its prized perps product.

Hyperliquid L1 features a general purpose parallelized EVM that is secured by the same consensus protocol as the L1, letting applications interact and build off the liquidity pools in its flagship perps and spot order books (this is still in testnet).

To let developers on Hyperliquid chain tap into its $2 billion+ in DEX liquidity, the team introduced “builder codes”, an onchain identifier that “lends” liquidity to applications under a fee-sharing agreement.

Taking a page out of Ethena’s book, Hyperliquid also introduced its own Hyperliquid Liquidity Provider (HLP) vaults that allowed users to participate in market making by depositing USDC and earn trading fees. As of November 2024, Hyperliquid’s HLP vaults have net a 25% annualized return. Outsized returns on USDC (with some risks) are also available in dYdX’s similar MegaVault launched earlier this month.

In the past few years, dozens of perps DEXs have come and gone, but no one player since dYdX in 2022 has monopolized the sector. The perps crown subsequently rotated to GMX to Vertex and Hyperliquid today, who controls the largest market share but still fairly low at less than 30%.

The reigns are short-lived, and usually comes due to fall in interest post-airdrop, yet Hyperliquid has managed to sustain usage since the conclusion of its primary six-month points campaign on May 1.

Source: Hyperliquid

Despite being one of DeFi’s most cutthroat competitive sub sectors, crypto derivatives trading is still largely dominated by centralized exchanges like Binance, with only about 3-5% of trading volumes in onchain DEXs.

For more on Hyperliquid, tap into 0x Research podcast’s episode with Hyperliquid co-founder Jeff Yan.

— Donovan Choy (X: @donovanchoy | Farcaster: @donovan)

P.S. We’re looking to improve the 0xResearch newsletter and make it more relevant to your interests. Help us out by giving us your feedback in this 2-minute survey.

Brought to you by:

Enter the Unlimited Era: Instant Market Creation, Automatic Liquidity.

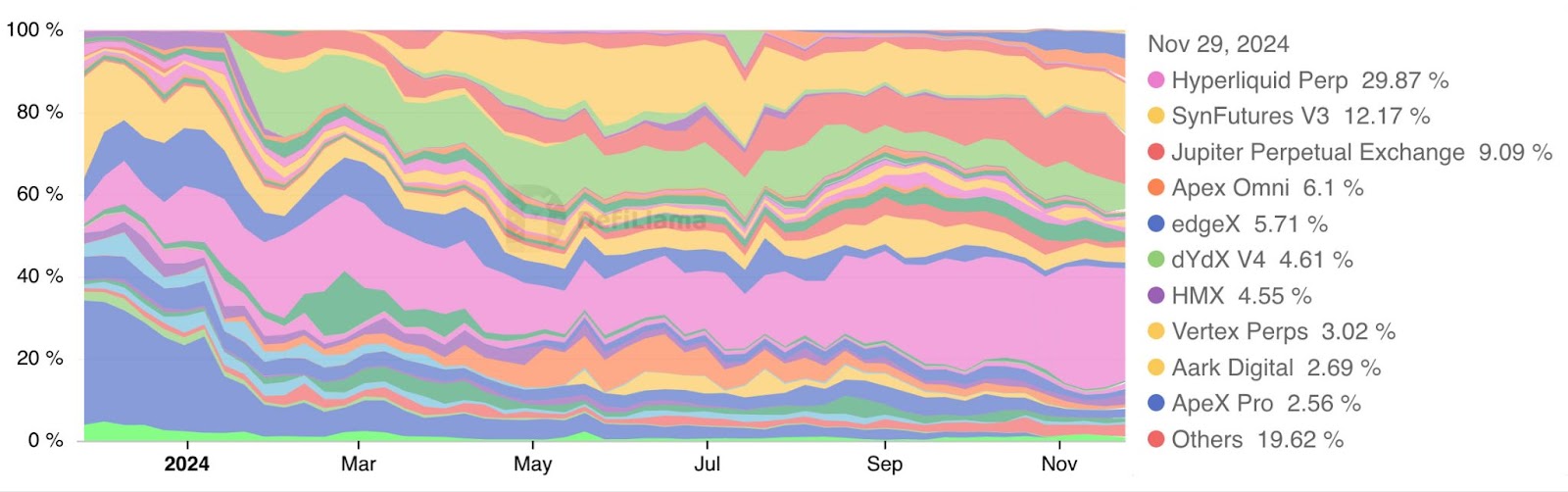

Perp dex dominance:

Source: DefiLlama

The chart illustrates the shifting dominance among perpetual decentralized exchanges (perp DEXs) throughout the past 12 months.

Hyperliquid emerged as the leading platform, commanding 29.87% of the market by November. SynFutures V3 and Jupiter Perpetual Exchange followed, with 12.17% and 9.09% respectively, reflecting growing diversity in user preferences. Apex Omni and edgeX maintained notable shares, though smaller, at 6.1% and 5.71%.

No doubt some of the ebb and flow in volumes is attributable to incentives for airdrop hunters seeking to maximize their token allocations.

The decline in dominance of early players like dYdX (V4 now at 4.61%) — which conducted an airdrop in August 2021, a year before announcing the pivot to its own chain — highlights increasing competition. Newer entrants like Vertex Perps, Aark Digital, and Apex Pro captured smaller but meaningful shares, while "Others" persistently occupied between 20-30%, signifying continued fragmentation.

Arbitrum: LTIPP Analysis:

The Arbitrum DAO’s Long Term Incentives Pilot Program (LTIPP) allocated 30.65M ARB to drive ecosystem growth, primarily in lending, DEX, and perpetuals (perps). Key takeaways include:

Success in DEX and Lending: LTIPP increased lending TVL by $38.64 and borrow TVL by $12.08 per dollar spent, stabilizing sequencer revenue and boosting Arbitrum’s L2 revenue share to 12.58%.

Challenges with Perps: Incentives failed to boost perps, with a 5% decrease in TVL market share, showing unsustainable impact and suggesting perps’ incentives are prone to gaming (e.g., wash trading).

Effective Strategies: Partnerships, enhancing LP returns, and responsive marketing boosted outcomes. Simple, focused incentives with measurable goals yielded better results.

Inefficient Approaches: Complex schemes (e.g., Gravita’s vesting ARB) deterred users. Incentives for larger, established protocols like Uniswap showed diminishing returns.

Recommendations: Target DEX incentives with focus on liquidity efficiency, foster ecosystem partnerships, and align programs with upcoming Timeboost upgrades to maximize revenue.

LTIPP insights highlight the importance of tailored, ROI-driven strategies for future programs.

You’ll find the full detailed analysis by magicdhz and Carolina on Blockworks Research.

Brought to you by:

Today’s sponsor is Bitkey, a hardware wallet for bitcoin created by the team behind Square and Cash App.

Effortless Security: Bitkey makes managing your bitcoin absurdly simple with a secure and easy-to-use setup.

Integration with Top Platforms: Connect with partners like Cash App, Coinbase, Robinhood, and Blockchain.com to easily compare prices before buying or selling.

Familiar and Intuitive App: The Bitkey app works like popular money apps, making sending, receiving, and tracking bitcoin value seamless.

Award-Winning Innovation: Recognized as one of TIME’s Best Inventions of 2024, Bitkey simplifies self-custody with a three-key approach, eliminating the need for complicated seed phrases.

Perfect Gift for Bitcoin Enthusiasts: Simplify self-custody for yourself or a bitcoin-loving friend.

For a limited time, get Bitkey for just $99 (save $51). Available on Amazon, Best Buy, or bitkey.world.

Geodnet is the world’s largest RTK network by both the number of base stations and coverage area, providing hyper-precise positioning data to Web2 customers. RTK networks are critical to enabling a world of ubiquitous autonomous drones, vehicles, and industrial robots.

In this unlocked research report, Blockworks Research’s Ryan Connor explores why the GEOD token enables both a cost and product advantage for the GEODNET RTK network, which will allow it to out-compete multibillion-dollar incumbents Trimble and Hexagon.

Coinbase notified customers in European Economic Area (EEA), Thursday, that it will end USDC rewards program or on Dec. 1, citing new EU crypto regulations under the EU's Markets in Crypto-Assets Regulation (MiCA). MiCA prohibits issuers of e-money tokens (EMTs) and crypto-asset service providers (CASPs) from offering interest or other benefits based on how long holders retain their tokens. This measure aims to prevent these entities from functioning like banks. USDC holders outside the EEA are unaffected.

Glow, a decentralized solar funding project, tripled its power capacity to over 22MW with the onboarding of a 16MW solar farm in Rajasthan, India. This groundbreaking move generated a record $13.6M in protocol fees, pushing Glow’s 30-day revenue to $17M. The protocol’s solar projects now aim to offset 300,000 tonnes of CO2, accelerating the renewable energy transition through DePIN innovation.

Coinbase’s recent decision not to support Celo migration to an Ethereum layer-2 optimium network has sparked disappointment in the crypto community. CELO holders on Coinbase exchange are required to withdraw funds before the January migration, to avoid risk of loss. Critics argue the move undermines Ethereum’s layer-2 scaling vision and decentralization efforts. Some view it as anticompetitive, noting Celo’s significant trading volume, although Coinbase rebuts the claim. Rival US exchange Kraken meanwhile made a point of signaling support for the migration in an effort to woo disgruntled Coinbase users.