- 0xResearch

- Posts

- Gold breaks down

This week, we focus on a breakdown that shouldn’t be happening.

Gold is trading like a risk asset, not a hedge, while commodities and perps continue to dominate flows across both TradFi and crypto rails.

We also take a deeper look at weekend market structure on Hyperliquid, separating signal from execution reality.

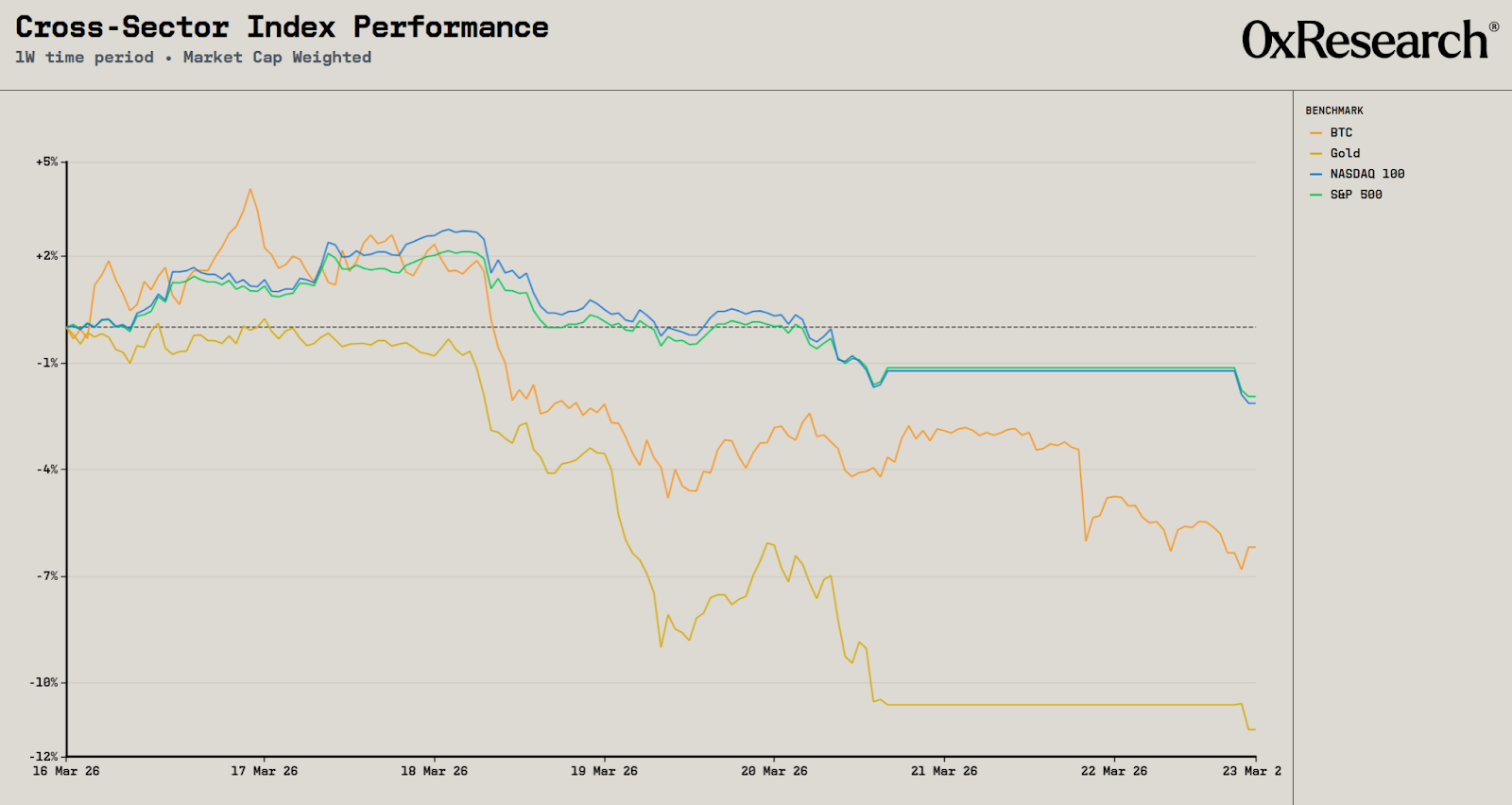

The past week has been brutal for markets, but what stands out is the sharp drawdown in gold despite its safe-haven status during periods of conflict and uncertainty. Gold is down −11.3% on the week, underperforming the S&P 500, Nasdaq and BTC, which are down −1.9%, −2.1% and −6.2% respectively.

Markets continue to be driven almost entirely by developments in the US-Iran conflict, with even minor signals of escalation or deescalation triggering sharp swings. As highlighted last week, oil remains the key variable. While prices have pulled back slightly, the earlier surge has already fed through to rates, with the 10Y yield rising 45bps since the conflict began — to 4.4%, levels last seen during Liberation Day last April.

Gold’s weakness, even as oil has eased, is particularly unusual. Historically, lower oil prices in this environment would have supported gold. The divergence suggests forced selling, likely from a large player being liquidated and needing to raise cash.

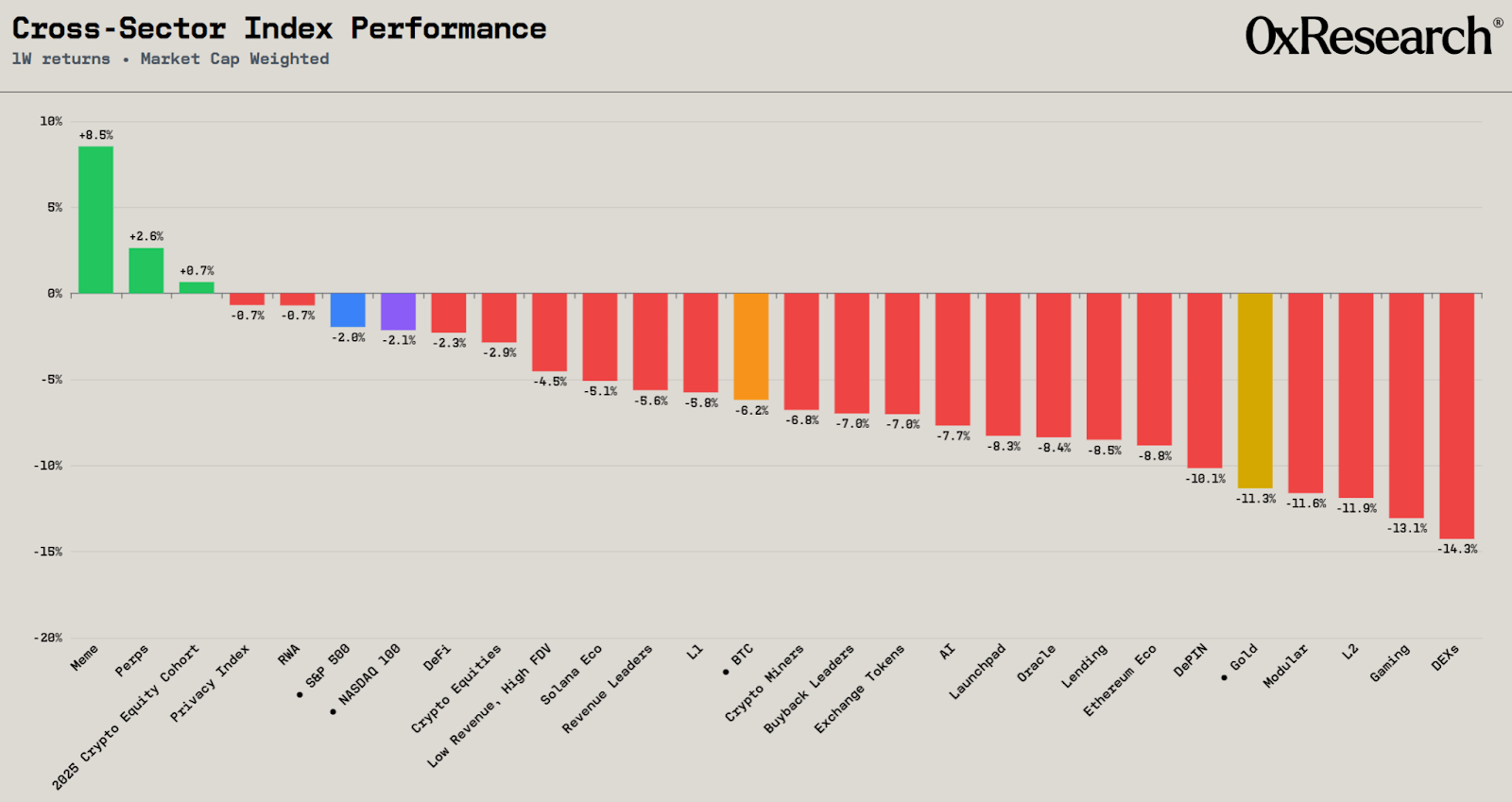

On the crypto side, performance was surprisingly led by Memes and Perps, which were up 8.5% and 2.6% on the week. The strength in Memes was almost entirely driven by Memecore, which is up 15.6% and accounts for 10% of the index. Outside of that, the broader sector remains weak.

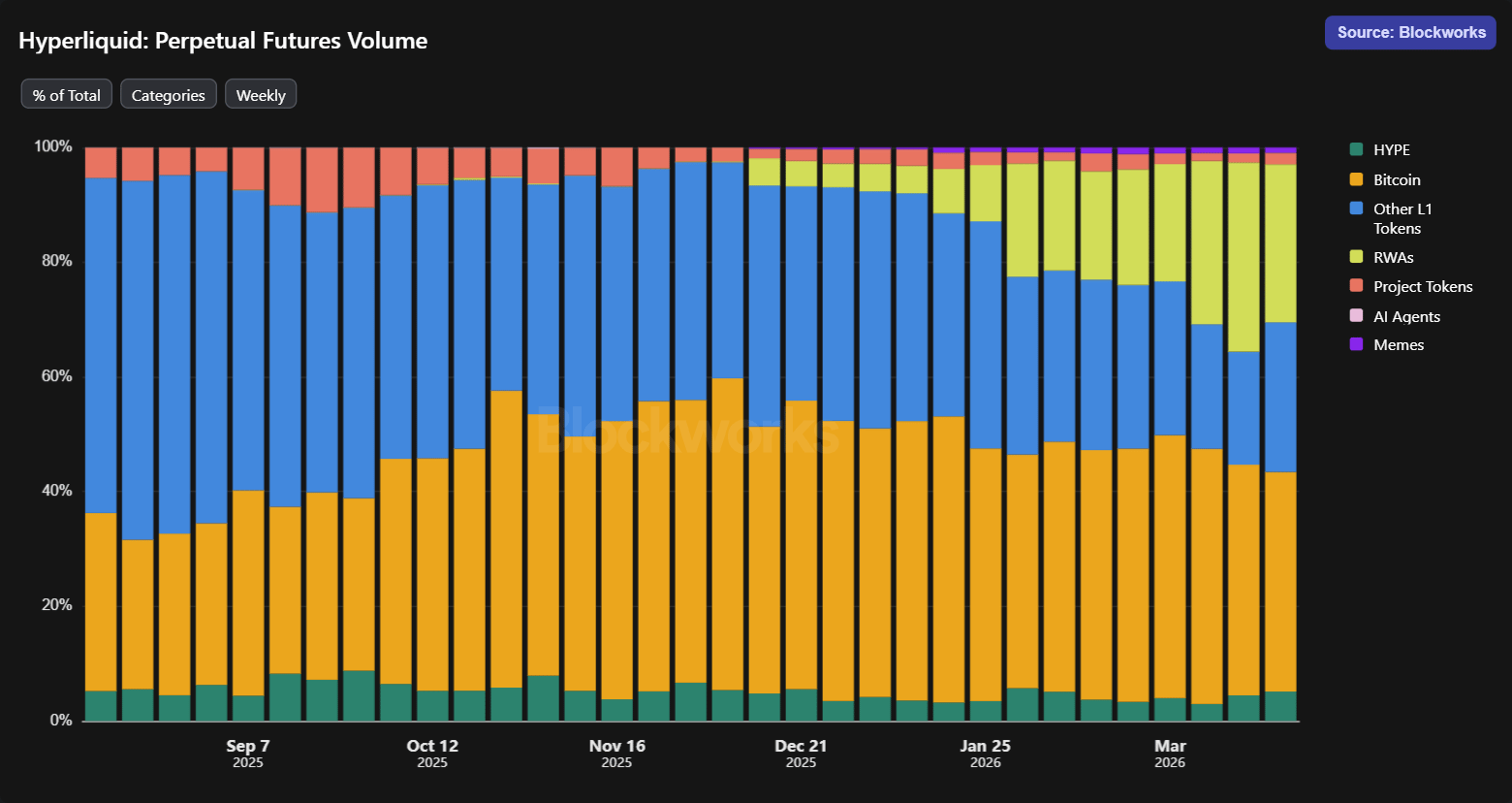

A similar dynamic is playing out in Perps, where HYPE was the only token in the green (up 2.7%) and accounted for 70% of the index. Open interest on Trade.xyz continues to hit new highs, with 40% concentrated in crude and Brent oil markets and another 20% in gold and silver. Commodities are becoming an increasingly important vertical, with RWAs now making up 33% of total perp volumes on Hyperliquid.

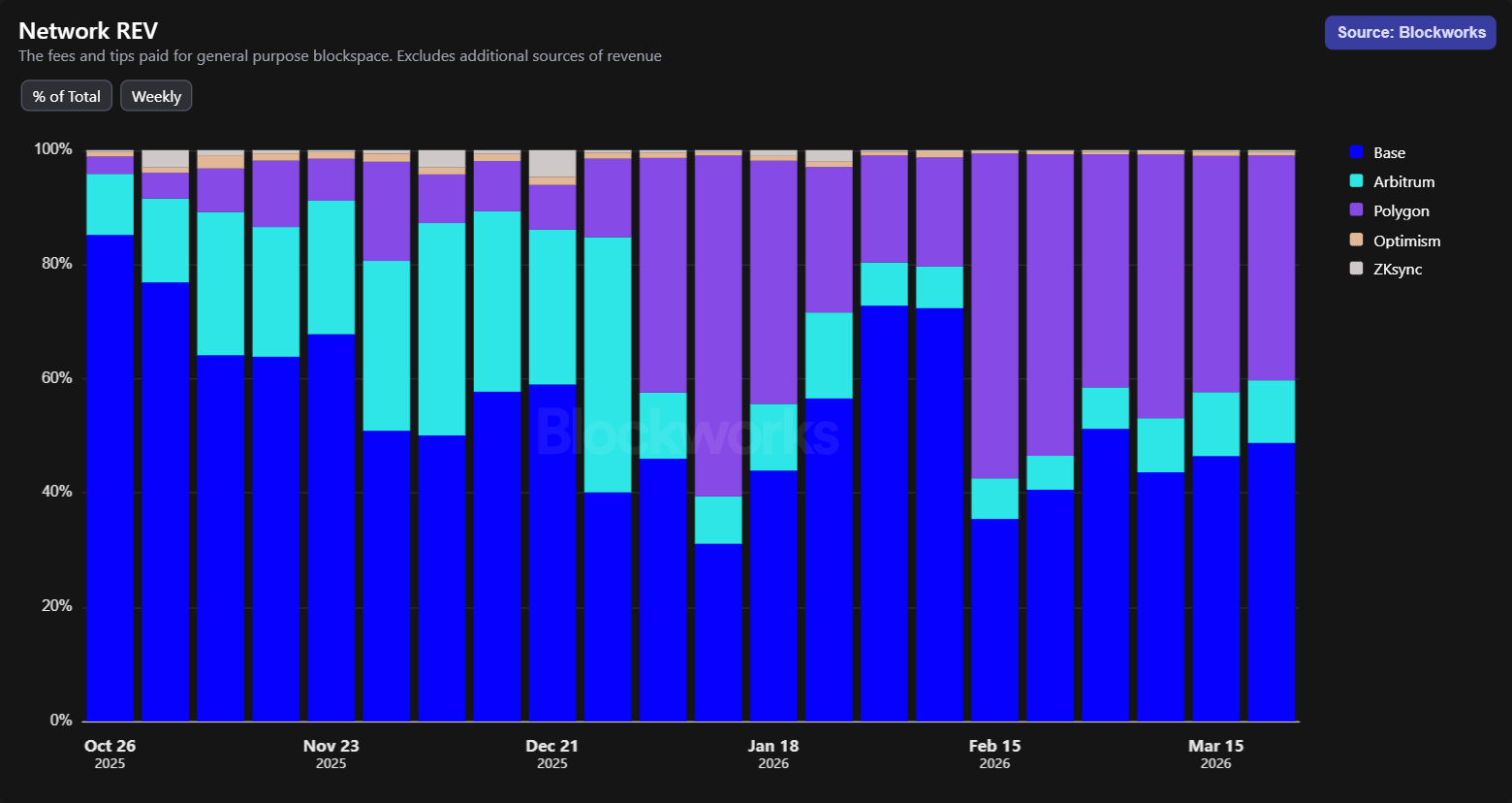

Elsewhere, Polygon has seen a sharp rise in REV in 2026 and is now matching Base on a weekly basis.

A large part of this appears to be driven by Polymarket activity, which contributes between 30% and 45% of network REV in most weeks. Over the last month alone, that translates to roughly $950K in revenue flowing through Polygon, raising an obvious question around whether Polymarket eventually launches its own chain to capture this value.

If it does, it would not only reshape Polygon’s revenue profile, but also mark the next phase in how successful applications think about owning their own infrastructure.

— Kunal

Are weekend markets efficient?

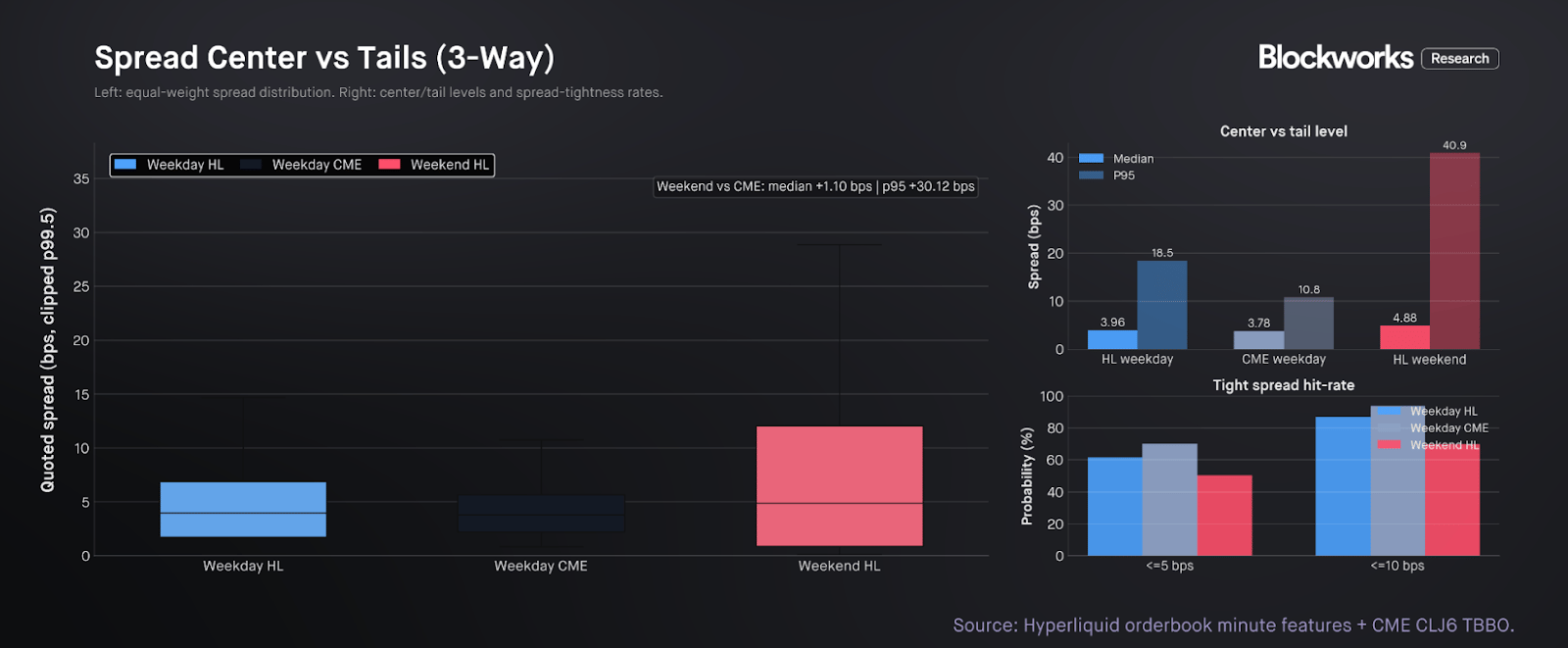

Recent events have made it clear that weekend markets on Hyperliquid are active and informative into the reopen, but the question of how tradable they actually are is a separate one. Across 21 XYZ markets and roughly 8.59 million weekday trades and 1.06 million weekend trades, the picture that emerges is more nuanced than a simple weekday-versus-weekend degradation story.

At the center of the distribution, the spread penalty is modest. Median quoted spread moves from 3.96 basis points on Hyperliquid weekdays and 3.78 on weekday CME to 4.88 on Hyperliquid weekends — a roughly 90 bps step-up that remains tradable for most participants. The real deterioration shows up in the tails: Weekend Hyperliquid reaches 23.43 bps at the 90th percentile and 40.90 at the 95th, versus 11.84 and 18.46 on Hyperliquid weekdays and 8.39 and 10.78 on weekday CME. In other words, the median participant pays a modest premium for weekend access, but hitting the book at an inopportune moment during a thin, fast-moving session can be meaningfully worse.

Depth is where the degradation becomes most structural. Median weekend depth retention sits at just 33.9% of weekday levels, and in 381 of 504 market-hour observations it falls below 50% of the weekday equivalent. The structural weakness of weekend trading is not stale or directionally wrong pricing — the constraint is materially thinner displayed liquidity and substantially less size behind the quote.

That weakness is not uniform. In the high-volume macro core — CL, XYZ100, EUR, SILVER and GOLD — flow concentration more than offsets the liquidity discount. The share of trades with absolute slippage within 10 bps rises to 89.7% on weekends from 77.7% on weekdays, the share above 25 bps falls from 8.5% to 4.0%, and notional-weighted slippage improves from 16.69 bps to 13.05. The main fragility of weekend trading is concentrated outside the most active macro products. Where off-hours risk transfer matters most, market quality is already strong enough to be economically meaningful.

— Shaunda

Plasma argues that global payments are being rebuilt around a new stack where banks handle fiat at the edges while stablecoins provide instant settlement in the middle. Traditional rails like ACH and SWIFT remain slow, opaque and batch-based, while stablecoins enable 24/7 transfers in seconds shifting the bottleneck to fiat on- and off-ramps. The key unlock is virtual-account infrastructure and automated conversion pipelines, which allow providers like Bridge to move from fiat deposits to stablecoin settlement and back programmatically.

Products like Plasma One abstract this complexity into a simple user experience, making payments feel instant even if underlying fiat rails still introduce some delay. The report’s core view is that stablecoins do not replace banking — they compress it, turning global payments into a faster, API-driven system with better capital efficiency and transparency.

Quinn Thompson and Felix Jauvin argue that the global macro landscape is being rebuilt around a new reality where central-bank policy is increasingly subservient to escalating energy shocks and geopolitical friction. While the Fed attempts to manage domestic rate expectations, the true bottleneck has shifted to the energy and agriculture complexes, where supply disruptions function as a form of “financial warfare” that bypasses traditional monetary transmission. This shift exposes a “policy paralysis” in foreign central banks, which are increasingly caught between the need for domestic growth and the structural reality of energy-driven inflation.

The key unlock is the concept of volatility transfer, wherein the U.S. maintains internal stability by effectively exporting its inflationary and liquidity pressures to the global periphery. The core view is that central banks haven’t just hit a pause; instead, they have reached their structural limits, meaning the traditional “Fed pivot” can no longer resolve the physical supply-side imbalances driving the market.

This turns the global economy into an increasingly fragmented system where geographic imbalances and second-order commodity effects — rather than mere interest rate changes — define the new macro narrative.

There’s one more day until DAS! NYC's lineup is bringing the biggest names in finance to the stage.

Don't miss the institutional gathering of the year — this March 24−26.