- 0xResearch

- Posts

- Ethena's $1B Solana week

Hi all, happy Tuesday!

Crypto traded in line with US equities on a quiet macro day, with sector dispersion driven by name-specific news.

Today, we cover Ethena’s rapid USDe growth on Solana and what it says about Solana lending markets’ ability to scale new yield-bearing assets quickly.

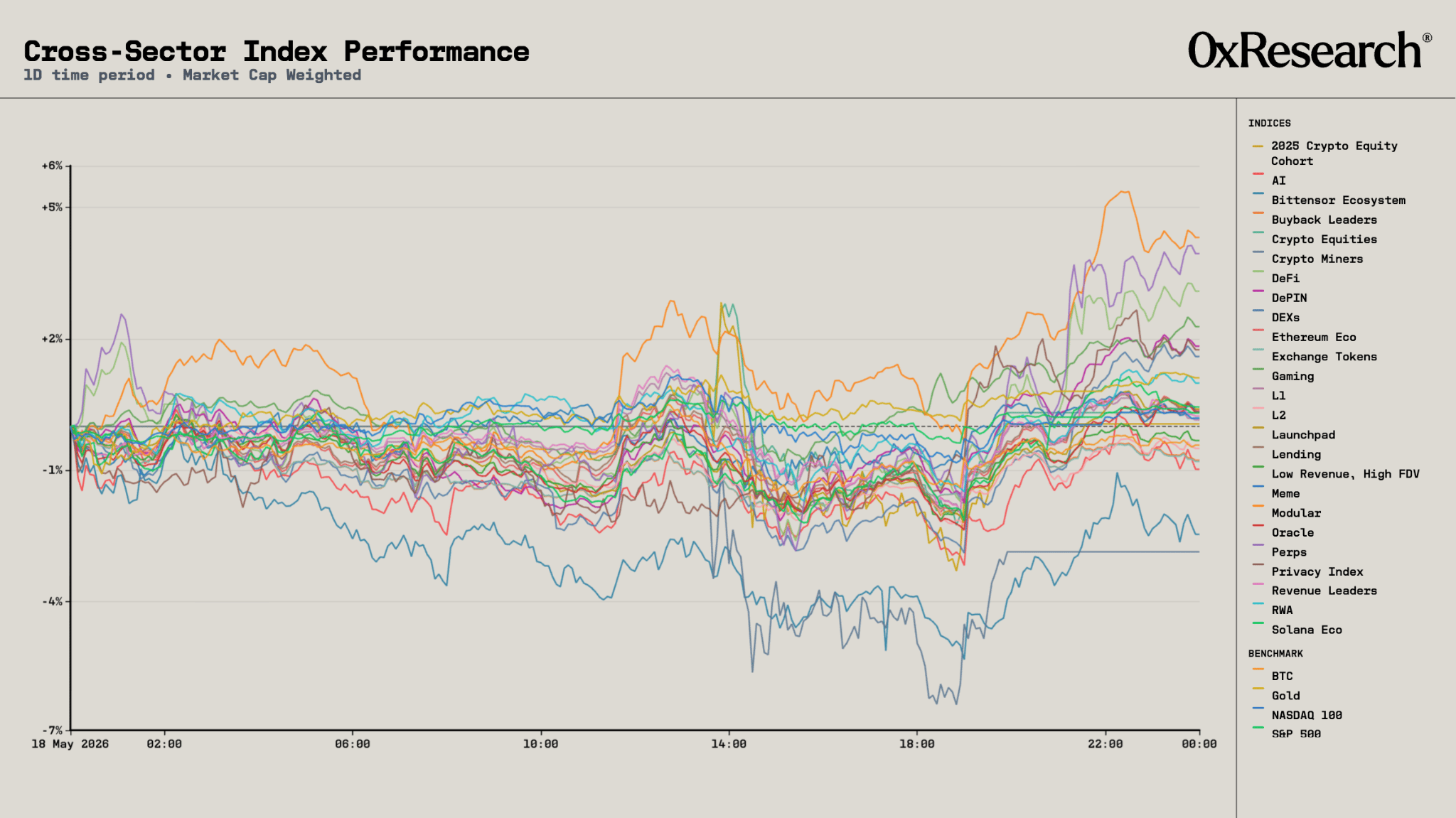

Markets seem befuddled by the Trump administration’s schizophrenic social media pronouncements on the Iran War, netting out to not much. The S&P 500 (+0.3%) and Nasdaq 100 (+0.2%) closed modestly higher Monday, with crypto-native sectors trading broadly in line. BTC finished -0.4% on the session, leaving the major beta indices clustered tightly around flat — L1s +0.2%, L2s -0.5%, Solana Ecosystem +0.4%, Ethereum Ecosystem +0.4%. A quiet tape, with the action concentrated in two idiosyncratic moves at the top of the leaderboard.

Modular (+4.3%) topped the cross-sector table, but the move looks idiosyncratic. DYM was the primary driver, and I wouldn't read this as a thematic signal for the modular thesis broadly.

DeFi (+3.1%) was another standout sector, driven almost entirely by Ondo. ONDO closed up roughly +11% on the day, breaking decisively away from the rest of the DeFi basket in the final four hours of trading (visible in the DeFi component chart).

The catalyst was SEC headlines on tokenization reported by Bloomberg, which Ondo could be uniquely positioned to capitalize on — the firm controls a substantial chunk of the tokenized equity market, has a no-action letter pending with the SEC since April, and is scheduled to begin production trades within the DTCC consortium in July alongside BlackRock and Goldman.

Other RWA-adjacent names participated more modestly — the broader RWA index was +1.0%, suggesting the move was a single-name re-rating rather than a sector-wide tokenization repricing. The Perps Index (+3.9%) and DEXs (+1.6%) rounded out the green, consistent with DeFi-adjacent strength rather than a directional crypto bid.

On the downside, Crypto Miners (-2.9%) and Bittensor Ecosystem (-2.5%) lagged, with AI (-1.0%), Exchange Tokens (-0.8%), and Buyback Leaders (-0.8%) also in the red. Miners diverging this hard from the broader Crypto Equities Index (+0.3%) is worth flagging, but I don't have a clean catalyst — could be Leopold Aschenbrenner FUD, as FinTwit pundits were reading too much into the March hedging behavior of Mr. “Ash burner.”

In sum, a relatively quiet day, punctuated by name-specific news (ONDO on tokenization, DYM on modular) rather than a directional bid or any clear thematic rotation.

— Macauley

USDe’s Solana Growth Loop

Ethena’s USDe growth campaign on Kamino and Jupiter Lend is proving how quickly Solana lending markets can scale new stablecoin products. As of May 18, roughly $530M is deposited into each market, for a combined $1.06B in deposits less than a week after launch.

Both markets enable users to loop USDG against USDe, with max yields currently around 20% and borrow capacity virtually maxed out. Ethena seeded both markets with roughly $200M of USDG liquidity, giving users immediate capacity to leverage the USDe carry trade.

The launch is also notable from a curation standpoint. Jupiter Lend’s market is being curated by Bitwise, likely the first example of an ETF issuer curating a DeFi lending vault, while Kamino’s market is curated by Sentora.

The early traction across both markets has been a tailwind for USDe supply growth on Solana, which has added roughly $560M since launch. Over the same period, USDG supply has fallen from $1.55B to $662M.

For now, demand appears constrained by USDG borrowing capacity rather than user appetite. We ran an hourly analysis on Kamino to better understand how the market has behaved.

Kamino case study

Our sample runs from May 12 at 19:00 UTC through May 18 at 18:00 UTC.

USDG supply was seeded at roughly $200M on May 12 at 19:00 UTC, but remained mostly idle until the public announcement on May 13 at 15:00 UTC. Demand appeared almost immediately: in that hourly bucket, USDG outstanding loans jumped from about $366K to $18.5M. By May 14 at 19:00 UTC, the reserve was near capacity.

Once the market became capacity-constrained, the next $50M of USDG liquidity on May 16 was absorbed far faster. USDG supply rose by about $50M at 12:00 UTC, and utilization was back near 100% by 13:00 UTC.

Overall, USDG utilization spent roughly 93 hourly observations above 99.9%, ending at 99.98% utilization with only about $46.3K of idle liquidity against roughly $250M supplied.

This has created very high gross leverage. Using USDG borrow divided by USDe deposits as a debt-to-collateral ratio, the market ended at 89.5%, implying roughly 9.6x aggregate leverage. The max observed ratio was 91.6% on May 13 at 18:00 UTC, implying roughly 11.9x aggregate leverage.

The market is effectively clearing on USDG borrow capacity. Demand to borrow against USDe collateral appears abundant, but the binding constraint is how much USDG can be borrowed. Once USDG utilization reaches 100%, new entrants cannot lever unless someone repays or new USDG capacity appears.

For Solana lending markets, this is a good early sign: liquidity showed up, users wanted to loop, and borrow capacity was filled almost immediately. But it is worth being clear about what is growing here. This is not broad, organic lending depth yet. It is highly efficient leverage formation around a specific stablecoin yield trade.

— Carlos

Alex McFarlane argues that modern DeFi lending is far safer than its reputation suggests: for EVM and Solana lending markets, excluding bridge-related incidents, the trailing 365-day hack/crime loss rate is only about 3 bps of lending TVL. It emphasizes that headline DeFi hack numbers are misleading because they lump together very different risk pools (bridges, wallets, DEXs, gaming, infra), while lending should be analyzed separately. The author shows exploit loss ratios have fallen sharply as lending markets matured, audits and monitoring improved, and recoveries have become meaningful, with lending-specific recoveries running higher than the broader DeFi average. The broader takeaway is that hack risk is now measurable, segmentable, and increasingly insurable, especially when paired with diversification, because most losses are isolated and small relative to TVL rather than existential to the whole market.

Euler published a note explaining that, after proving its markets can generate and transparently convert protocol revenue through Fee Flow, it is now setting protocol fees to 0% to prioritize growth. The post argues that Fee Flow served its purpose as a public proof of monetization — processing 838 onchain auctions across 14 chains, converting $3.39M of fee assets into $3.17M of EUL at 93.7% weighted clearing efficiency — but that protocol-level fees now risk becoming friction for curators, vault operators, integrators, borrowers, and suppliers trying to build on Euler. The core message is that Euler has shown fee capture works; the next phase is to remove that base-layer take rate so the market layer has more room to scale, compete, and expand the number of high-quality markets built on the protocol.