- 0xResearch

- Posts

- 🟣 EigenLayer tokenomics under fire

🟣 EigenLayer tokenomics under fire

When ‘locked' tokens aren’t truly locked

Brought to you by:

Welcome back to 0xResearch. Here's what we’ve got for you today:

The FUD around EigenLayer tokenomics

Research: Uniswap and Across Protocol’s ERC-7683

Chart: USDS tops a billy

Degen: P2P.org bitcoin staking API

The FUD around EigenLayer tokenomics

Here’s how private investor allocations into pre-launch tokens generally work:

You are a reputable name or a KOL with many Twitter followers, and projects want your clout.

A project offers you a percentage of locked tokens at a favorable price, so you agree to invest.

On the day the project launches its “token generation event” (TGE) and tokens become tradable, your locked allocation of tokens enter a “cliff” period.

That cliff is typically about a year (though in bull markets has been known to drop to six or even three months), during which your tokens are effectively locked up.

Once that cliff is up, your tokens enter a “vesting” period — typically two to four years — during which your locked tokens begin to slowly unlock and become liquid and tradable.

Things are set up this way to create long-term incentive alignment between investors and projects to build a successful product, and ultimately deter predatory dumping on retail investors.

EigenLayer finally made its native EIGEN token transferable yesterday, amid a barrage of criticism around the opaqueness of EIGEN’s true float (circulating supply).

That is pretty important to know because low-float tokens are more volatile and subject to less market price discovery, and are therefore predatory for the unsuspecting retail investor eyeing them hungrily on the Binance mobile app.

After accounting for unclaimed EIGEN and the 73 million EIGEN already restaked on EigenLayer, Kairos Research estimated that the real float of EIGEN was about 2.42% — a float even shockingly lower than Worldcoin’s (WLD) ~4.9% — though EigenLayer disputed that number.

And it gets more complicated.

The “locked” EIGEN tokens by EigenLayer investors are apparently not entirely locked.

During the so-called locked cliff period, EigenLayer investors can already stake their “locked” tokens, receive rewards, and begin selling those rewards on the open market. As noted in their just-updated docs:

“*EIGEN staking: Eigen Labs Investors are not restricted from staking EIGEN on EigenLayer. As such, investors may choose to stake their EIGEN and receive staking rewards the same as any other user. EIGEN provided by Eigen Labs to investors is subject to the Lockup Schedule, but EIGEN investors receive from staking will not be subject to the Lockup Schedule.”

But if locked tokens are accruing a yield, then that is arguably not a “locked” token.

I was under the impression that this was a rare and frowned upon practice that Celestia started, but it’s apparently becoming a standard playbook with several L1 projects including Sui, Sei and Aptos.

Yield-generating “locked” tokens defeats the whole purpose of locking up private investor tokens for “incentive alignment,” and it’s also effectively a form of double-dipping. Worse still, it double-dips from a reward pool that could have been allocated to actual productive capital, e.g. restaking and securing an EigenLayer AVS.

In EigenLayer’s defense, there is at least a cap on those emitted rewards. Based on its docs, 1% of the total EIGEN supply ($60 million) is emitted as rewards annually, and 25% of that is reserved for EIGEN stakers, while the other 75% goes to ETH stakers on EigenLayer.

I guess when EigenLayer was talking about “restaking,” it had in mind its investors too.

— Donovan Choy (X: @donovanchoy | Farcaster: @donovan)

Brought to you by:

lpETH invites you to the on-chain Pool Party!

Built by Tenderize Labs, lpETH is an on-chain clearinghouse that reinvents liquidity for (re)staked ETH. Users can instantly unstake ETH and anyone can deposit ETH as liquidity to earn yield collected from swap fees, token bribes and lpETH native incentives. Pre-launch deposits are open for another 21 days, be sure to sign up through Turtle Club before depositing ETH to claim a 66% boost in incentives and a referral code.

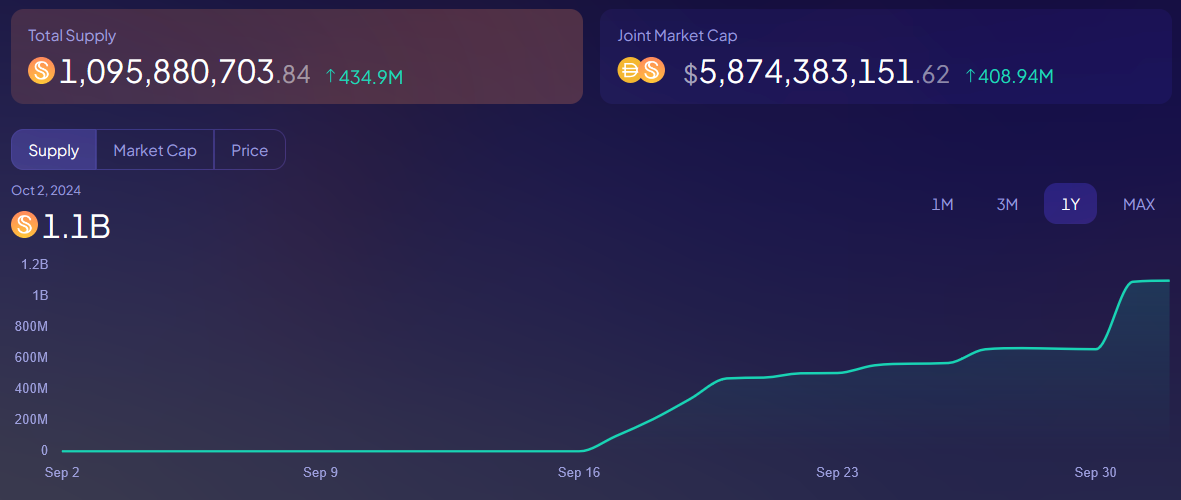

USDS heads skyward:

Sky’s USDS stablecoin has hit $1.1 billion since its inception exactly one month ago. In Maker’s rebrand to Sky, existing DAI holders have the option to convert DAI to the rebranded USDS.

The joint market cap of both USDS and DAI is now nearly $5.9 billion, the highest it’s been on a year-to-date basis.

— Donovan Choy

We previously looked at BOB Stake for the Bitcoin/Ethereum “hybrid L2” BOB, and Stroom, a liquid staking provider for the Lightning Network.

To further the theme of safe bitcoin staking for noobs, leading staking-as-a-service provider P2P.org today introduced a Babylon staking API to offer exchanges, custodians and wallet providers a way to integrate bitcoin staking directly into their platforms.

Instead of switching to a third-party interface, individual users and institutional investors can use the service to access bitcoin staking rewards through a familiar platform. Candidates include exchanges, wallets and LRT providers.

The API is designed to simplify the complex tasks of creating, signing and broadcasting bitcoin transactions, for instance by handling the RPC connection.

In terms of future updates, P2P plans to add features like batch staking — allowing users to generate multiple staking transactions from a single address. This will help institutions stake bitcoin efficiently before the Babylon BTC cap is reached.

Analyst Opinion on Uniswap and Across Protocol’s ERC-7683:

ERC-7683, developed in collaboration between Across and Uniswap, allows for a standardized application programming interface to settle cross-chain intents-based orders. This standard allows for the expression of a generic cross-chain order that contains the user’s intent, giving integrators the flexibility to define and be opinionated about the price resolution mechanism, as well as the ability to delegate a settlement contract to verify order fills and administer refunds to relayers.

Intents-based protocols have gained significant market share in settling volumes for cross-chain orders like bridging. Users express their intent, usually requesting a balance of funds on a destination chain, and lock their principal on the source chain, accompanied by a fee they are willing to pay a relayer to fill their order. Relayers listen to these orders originated through the protocols, and front users their capital from their own balance sheet on the destination chain to provide a fill. Subsequently, the protocol verifies that the fill occurred on the destination chain, and refunds the relayer with the user’s original deposit and the fee.

While these protocol designs can offer amongst the cheapest and fastest fills for cross-chain interoperability, they embed their own issues of liquidity fragmentation. Solvers must continuously subdivide their balance sheet across destinations and pay transaction costs to rebalance accordingly. Additionally, liquidity from one relayer network is not necessarily available to provide fills for multiple competitive intent-based protocols that are sourcing orderflow, as relayers run unique client implementations that are specific to fill orders from one protocol. These issues fragment relayer liquidity, which ultimately leads to higher costs and lower welfare for the end user.

— Luke Leasure (X: @0xMether)

Is AI x crypto overhyped? Permissionless is bringing you the highest signal conversations at the nexus of these two nascent technology sectors.

Bitwise took the initial steps for an XRP ETF Wednesday.

Plus, this election just isn’t about crypto.

|

|

The insights, views and outlooks presented in the report are not to be taken as financial advice. Blockworks Research analysts are not registered broker/dealers or financial advisors. Blockworks Research analysts may hold assets mentioned in this report, further outlined in the Firm’s Financial Disclosures.