- 0xResearch

- Posts

- 🟣 EigenLayer’s top operator shares profits

🟣 EigenLayer’s top operator shares profits

Plus, Q3 crypto VC funding lags behind

Brought to you by:

Welcome back to 0xResearch. Here's what we’ve got for you today:

P2P.org’s revenue distribution

Chart: Crypto VC funding levels

Listen & Read: Are memecoins fair play?

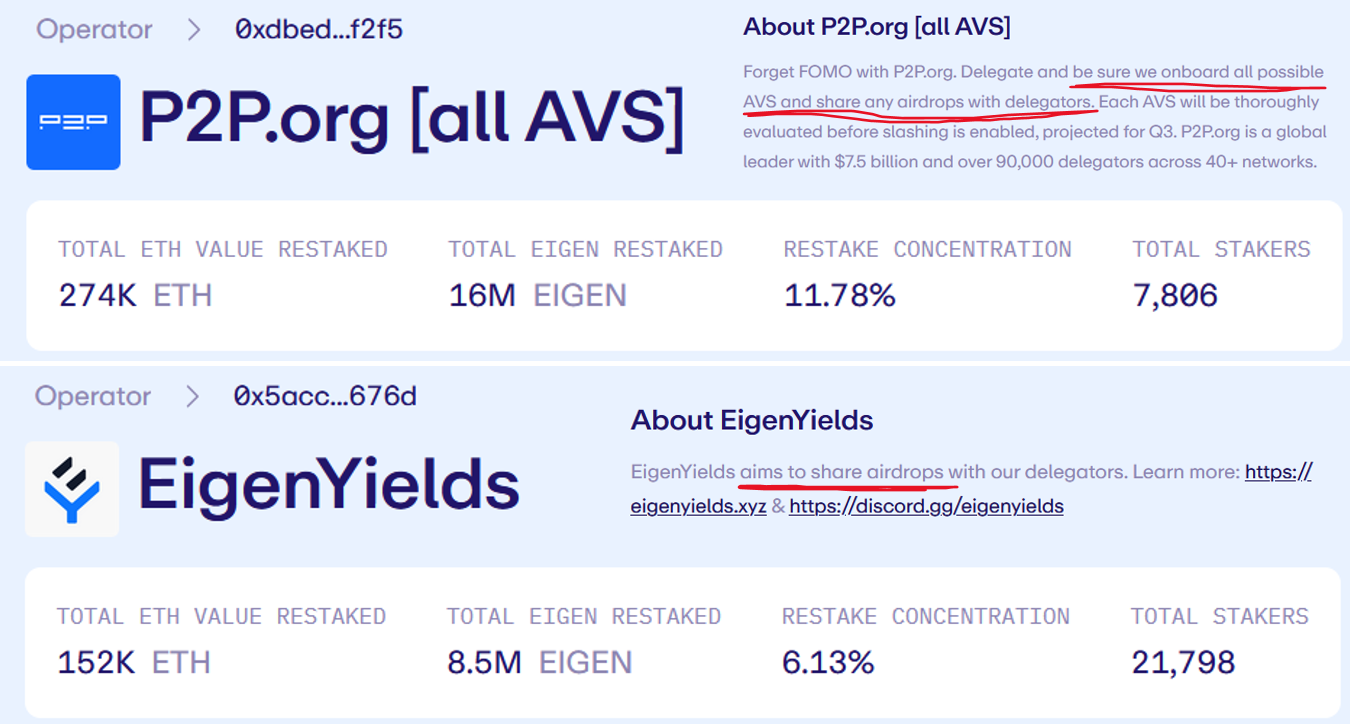

P2P.org to offer revenue distribution to EigenLayer delegators

Here’s a simplified explanation of how restaking works today:

Bob deposits ETH/stETH into a liquid restaking protocol like Ether.Fi, Puffer, Eigenpie or Renzo.

The liquid restaking protocol delegates Bob’s assets to an EigenLayer operator.

The EigenLayer operator uses Bob’s asset to secure one or many AVSs to return some yield to Bob.

Bob is happy because his ETH is a yield-bearing productive asset, and he enjoys a liquid ETH derivative that he can use to dabble in other degenerate DeFi activities.

About 299 active EigenLayer operators compete for $11.2 billion in TVL in EigenLayer, so competition is pretty stiff.

EigenLayer operators compete for user attention in one of many ways.

Technical competency is one obvious factor, namely keeping a consistent uptime and fulfilling specific responsibilities for the AVSs they validate.

Operators also try to validate as many AVSs as they can so as to compound yield returns to users (and slashing risks), or promise to share any potential airdrops with delegators. You can see many such explicit advertisements on the EigenLayer operator page.

Another way that EigenLayer operators could compete, of course, is to simply promise more of their cut to delegators. That has not been the case, until today.

P2P.org, the largest EigenLayer operator by total ETH restaked (at 274,000 ETH), announced Wednesday that it would launch revenue distribution to users delegating ETH to them.

As part of a “new structure [to] reward long-term trust and engagement,” all delegators staking with P2P.org prior to Aug. 15 will be eligible for the revenue share.

It’s a bold move — and not one you’d typically expect from a leader at the top.

It’s not clear how much revenue that actually translates into for P2P.org delegators, but here’s some napkin math from Blockworks Research Analyst Marc Arjoon.

With ~8K stakers on @P2Pvalidator this equates to ~$1,500 pp (at today's prices with no commission and excluding additional AVS revenues)

— Marc Arjoon 🟪 (@marcarjoon)

2:22 PM • Oct 16, 2024

P2P has about 274,000 ETH and 8.53 million EIGEN staked on EigenLayer across ~8k stakers.

As part of its “programmatic incentives” program, EigenLayer is allocating 67 million EIGEN through the first year, with 3/4 going to ETH stakers and another 1/4 to EIGEN stakers and operators.

For P2P, that comes up to about ~3.63 million of EIGEN incentives (worth $12 million today).

Assuming today’s EIGEN price of $3.3, each staker would receive about $1,500, excluding any AVS yield.

Not a bad reward.

— Donovan Choy (X: @donovanchoy | Farcaster: @donovan)

Brought to you by:

Obol Collective, the distributed validator ecosystem scaling and decentralizing Ethereum, and Liquid Collective, the trusted and secure staking standard, are collaborating to build the world’s confidence in ETH staking and risk-adjusted participation.

Empower yourself to stake confidently with Liquid Collective and Obol’s staking research and resources.

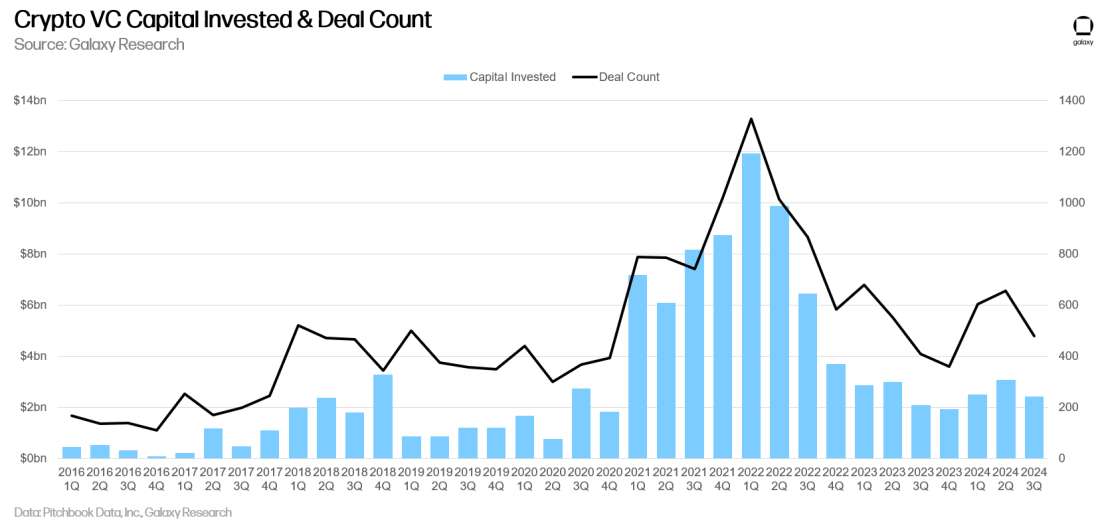

Crypto VC funding still lagging:

According to Galaxy Research, crypto venture capital funds invested about $2.4 billion across 478 deals in Q3 2024. That’s 20% capital invested and 17% fewer deals than the previous quarter.

Within Q3, companies in the “trading/exchange/investing/lending” category raised the most, at $462 million. Cryptospherex and Figure markets raised $200 million and $73.3 million, respectively.

In a sign that the L1 trade isn’t going away, the second-largest raise came from L1 projects — about $341 million in total.

— Donovan Choy

Unichain aims to establish a liquidity layer, potentially addressing fragmentation issues across L2s. The chain could significantly impact asset issuance dynamics and liquidity distribution across Ethereum and L2s. While Unichain offers potential benefits for UNI token holders through MEV revenue and staking, it could face challenges in attracting liquidity and competing with established L2 solutions. The success of the chain will depend on its ability to attract activity, volumes and liquidity onto the chain and navigate potential security risks associated with its architectural design.

EigenLayer's shift to permissionless AVS onboarding and token support promises enhanced flexibility but introduces new risks. Dynamic stake allocations create a fluctuating security landscape, requiring vigilant monitoring. The move towards an “ETF-like” restaking model opens doors for diverse, tradable portfolios. However, token volatility and a challenging vesting schedule loom large, threatening potential dilution. As EigenLayer navigates these waters, its success hinges on achieving exceptional adoption to offset supply expansion.

Are memecoin trades fair play now?

Ryan Connor: I think memecoins are increasingly fair play. The longer they trade, the longer historical time series data we have, the more palatable it becomes to quantitative traders and hedge funds. This propagates trader myths further and establishes these norms in the market. Every day the volumes increase, it becomes less and less illegitimate. The volumes will likely plummet 90% at some point, but so will general market volumes.

Can Sui and Aptos win?

Ryan Connor: It’s becoming increasingly clear that everything going forward is a business development game. It’s getting legitimate asset issuers to put their token on the chain. Polygon crushed it on the BD front two years ago, but none of them were issuing assets that people wanted to trade. This is in contrast to how Solana brought on Geodnet and many other DePIN projects, or LST issuers on Ethereum.

How should we value crypto tokens?

Boccaccio: If projects are going to play the narrative and speculation game, do it on something that you can’t value by cash flows. Like for instance, TAO, which is AI mumbo jumbo, instead of Celestia which is making 30 grand a year on a billion dollar FDV. That’s why I think the L1 trade has always been lucrative because it’s hard to do a proper cash flow business analysis on it.

Danny Knettel: Investors in TIA have a mindset that these networks will power billions of users transacting on them and will process gigabytes and terabytes of data availability and be worth so much. But then when you look at it today, the actual revenues and usage are nowhere near that. They're basically zero. It's like there's this kind of war being waged in between investors looking for real cash flows now and the people who are clinging to the idea that you can perform valuations on future cash flows.

Plus, would crypto be better out of the limelight?

Coinbase hired History Associates in 2023 to assist in retrieving records from the SEC and FDIC.

|

|

The insights, views and outlooks presented in the report are not to be taken as financial advice. Blockworks Research analysts are not registered broker/dealers or financial advisors. Blockworks Research analysts may hold assets mentioned in this report, further outlined in the Firm’s Financial Disclosures.