- 0xResearch

- Posts

- Betting on geopolitics

Betting on geopolitics

Polymarket volumes surge on Iran markets

Sam Schubert & Kunal Doshi

March 13, 2026

Hi, everyone. Crypto pushed higher today even as equities slipped, with AI once again standing out as the strongest sector. The move builds on a powerful weekly trend fueled by Nvidia’s agent narrative and growing conviction that AI systems will rely on crypto rails for payments.

Below, we break down the AI rally and explore how geopolitical tensions are fueling activity on Polymarket, which has quickly tapped into this trend.

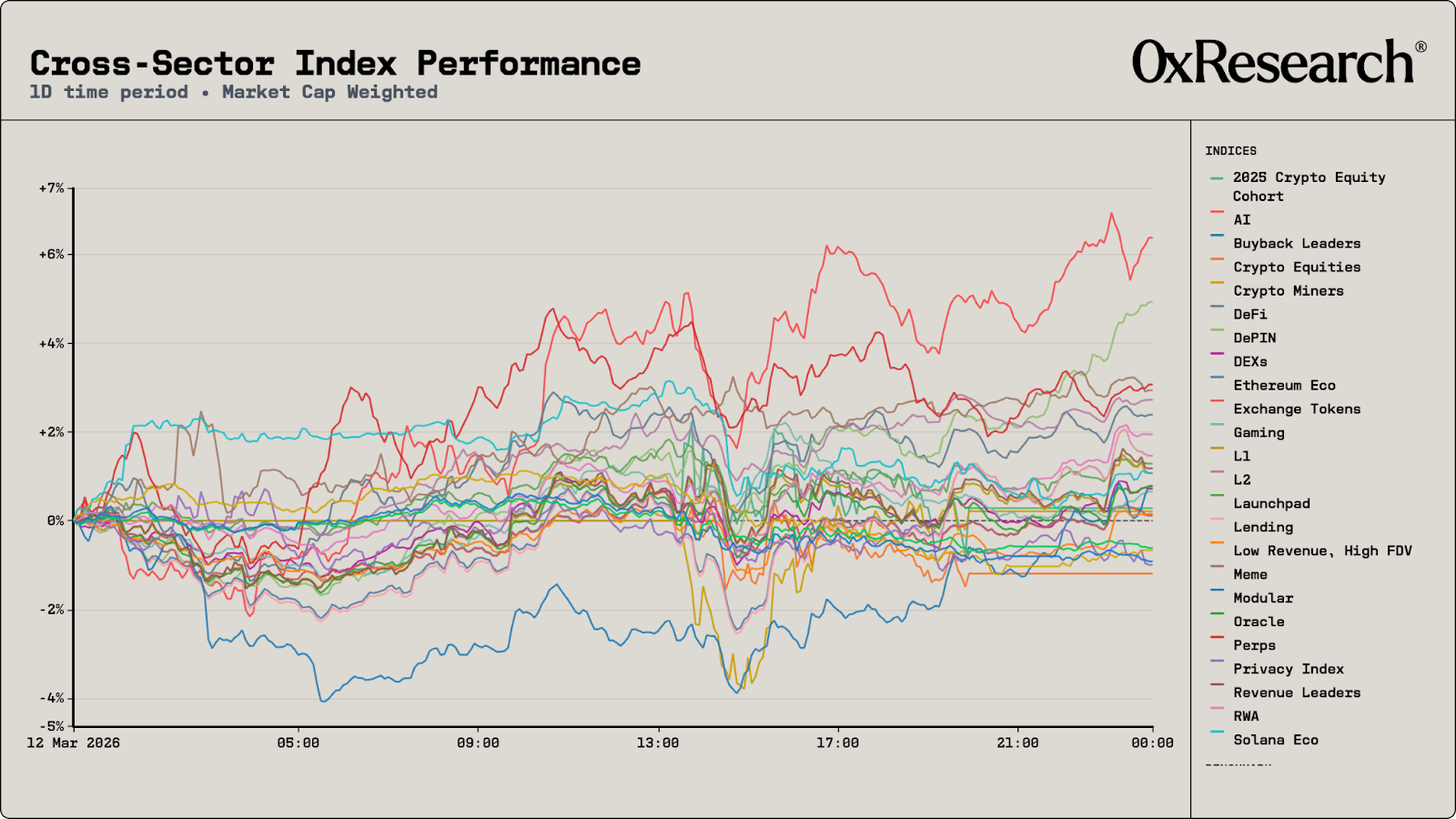

Today saw broad green across the board, with AI as the clear standout, even as the S&P 500 slipped 0.6%. Most sectors clustered in the 1% to 3% range, but AI pulled away decisively as the clear performer: AI was up +6.4%, DePIN +4.9%, Perps +3.1%, and DeFi +2.4%. Crypto equities bucked the trend in the wrong direction, down −1.2%.

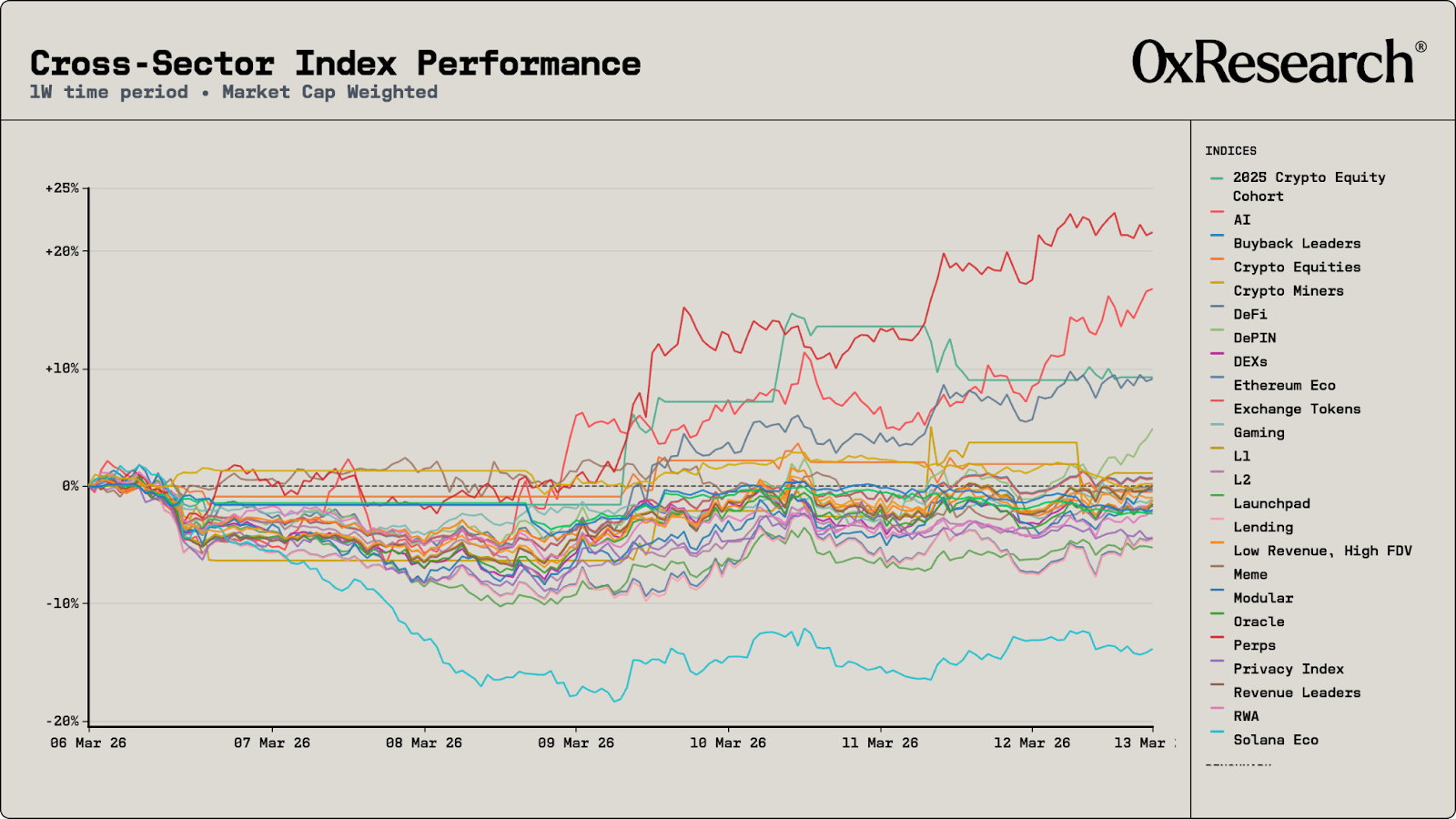

The weekly view confirms the trend. AI was up +16.8%, second only to Perps (+21.6%). The AI bid traces back to March 10 and Nvidia’s announcement of NemoClaw, an open-source platform for deploying autonomous AI agents that the company plans to debut at GTC (Nvidia’s GPU Technology Conference) next week. Coinbase’s Brian Armstrong and CZ both argued this week that AI agents need to transact via crypto, as banks cannot serve them — reinforcing the narrative that AI agents will need crypto rails for payments.

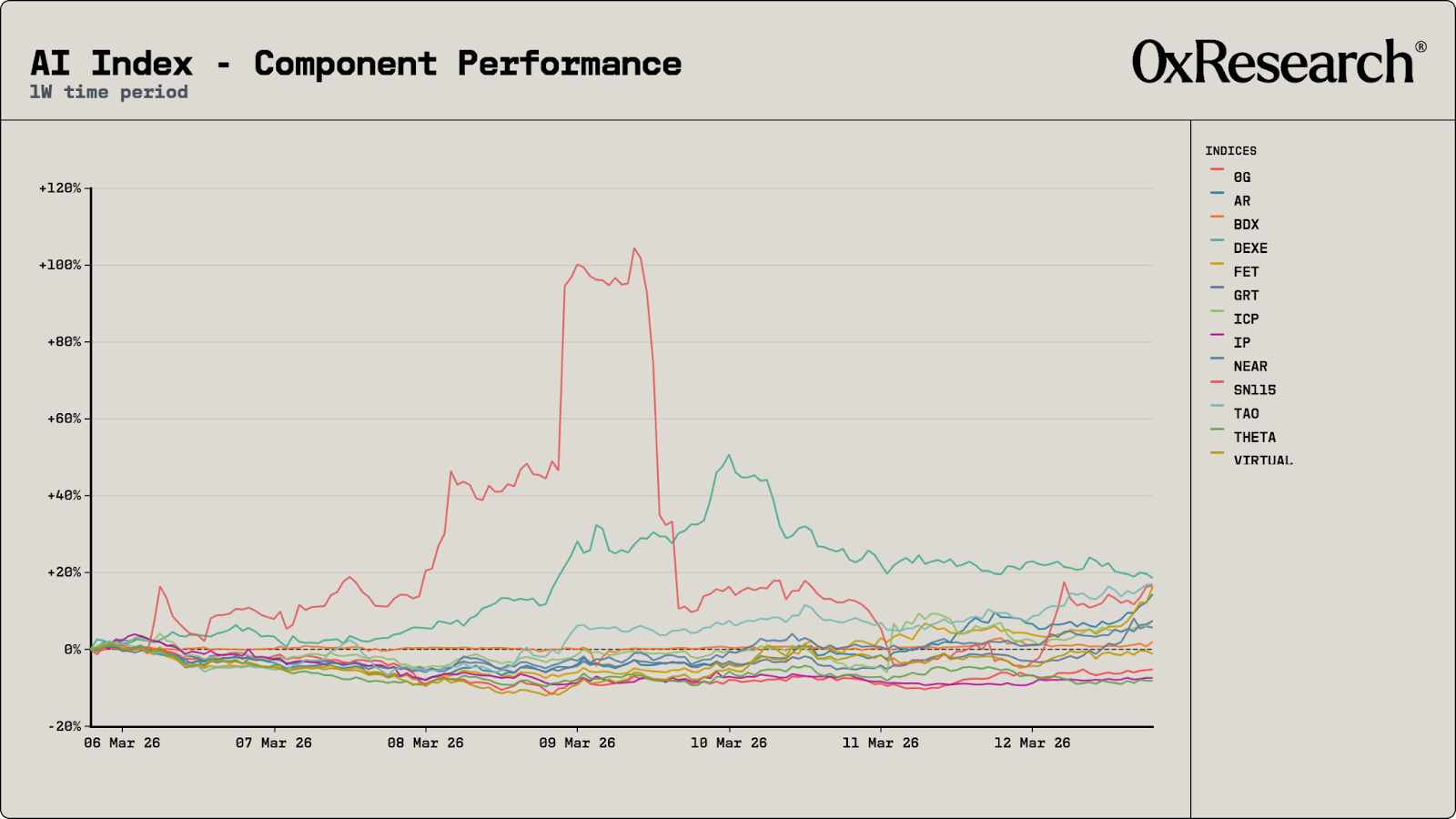

Inside the AI index, SN115 led the day at +19.0% with FET close behind at +10.7%. On the weekly timeframe, DEXE topped at +18.6%, TAO +17.0%, and FET +16.3%.

TAO continues to benefit from the post-halving supply squeeze (daily issuance cut from 7,200 to 3,600 in December) and a potential ETF on the horizon with Grayscale’s conversion filing. This week specifically, General Tensor closed a $5 million oversubscribed seed round on March 11, anchored by Good Morning Holdings (Goldman Sachs-backed), and TAO broke through $200 resistance.

— Sam

The rise of geopolitics markets

While much of the attention has been on Hyperliquid enabling traders to express views on traditional markets over the weekend, the Middle East conflict has also highlighted another prominent platform: Polymarket.

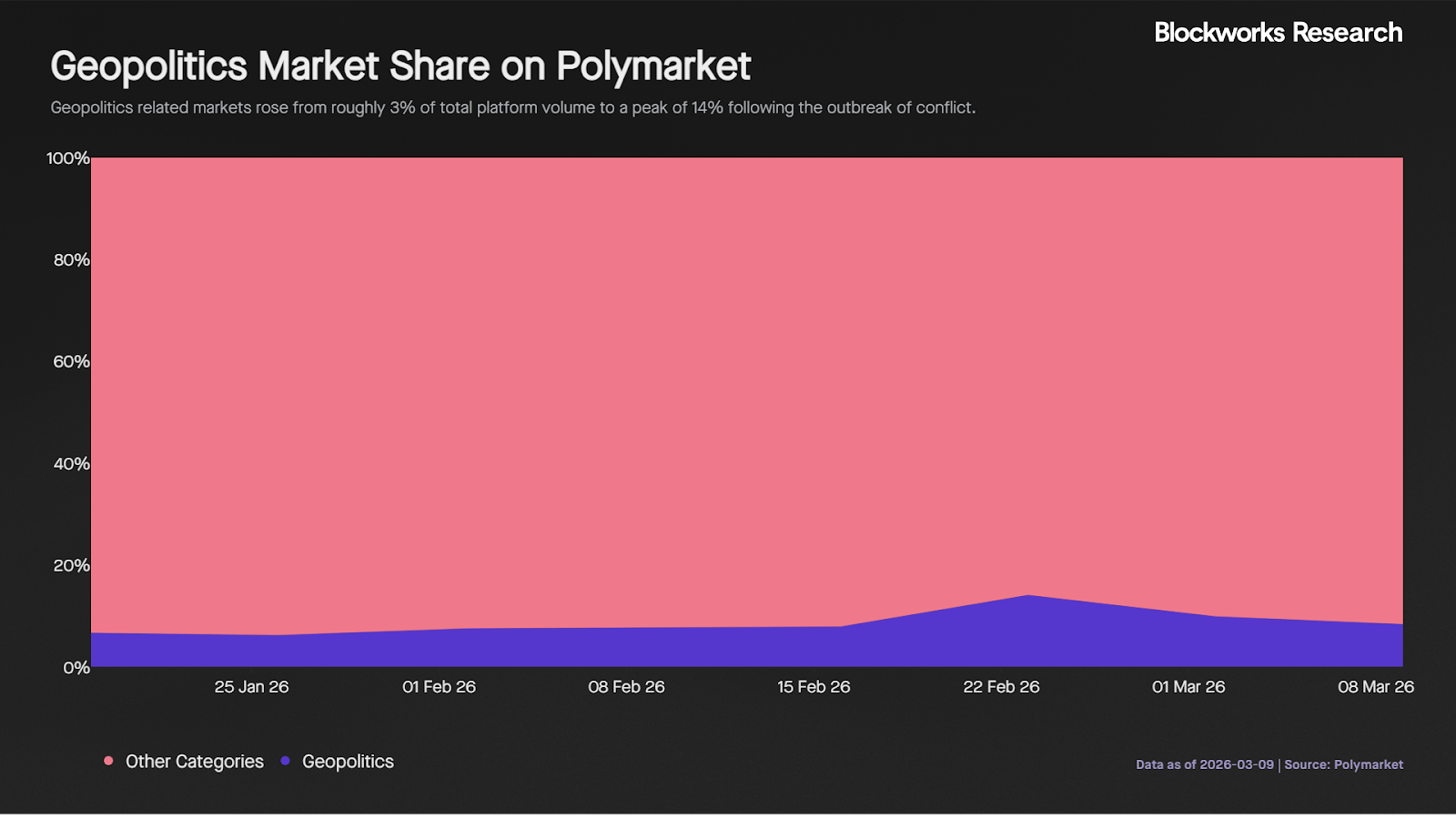

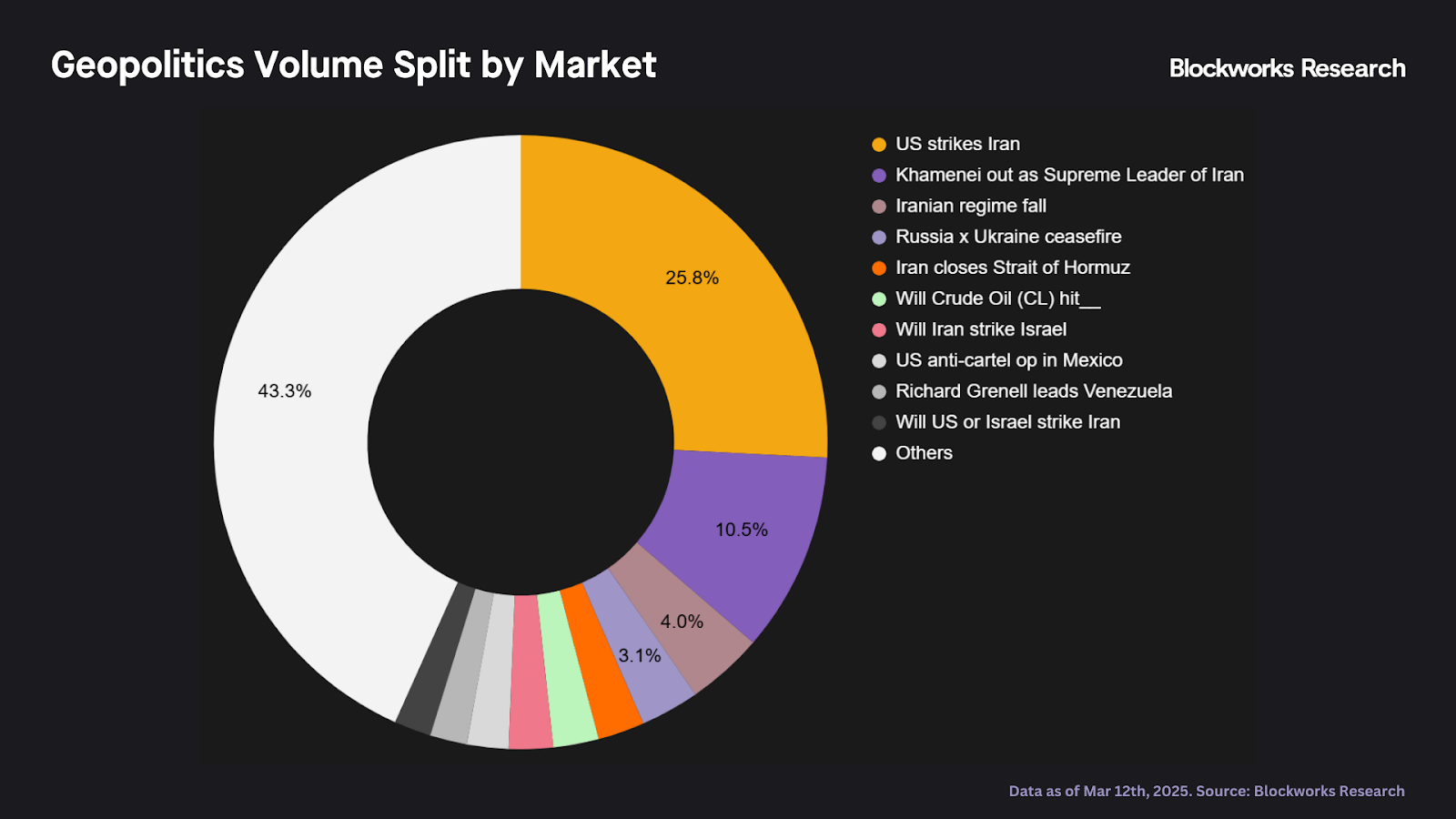

One thing that stands out is how quickly the platform launches relevant markets that gain immediate traction. Geopolitics-related markets have surged in activity since the conflict began, rising from about 3% of total volume before the escalation to a peak of 14%.

A closer look at the breakdown shows that the top ten markets account for 57% of total volume, with most of them tied directly to developments in Iran.

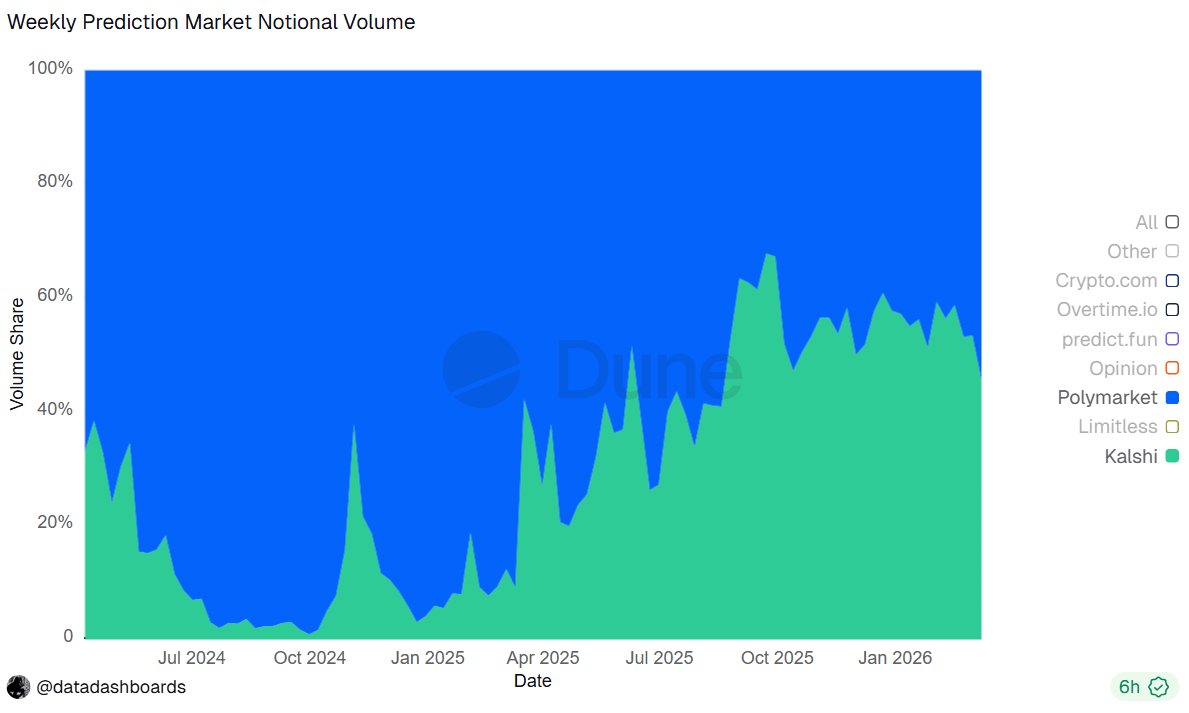

If the pattern we have seen so far in 2026 continues, geopolitics could become one of the dominant themes in prediction markets: Platforms that allow traders to place directional bets or hedge geopolitical exposure stand to benefit. This shift is already visible in market-share data, with Polymarket clawing back ground from Kalshi and increasing its share from about 40% to 55% of total volumes since early February.

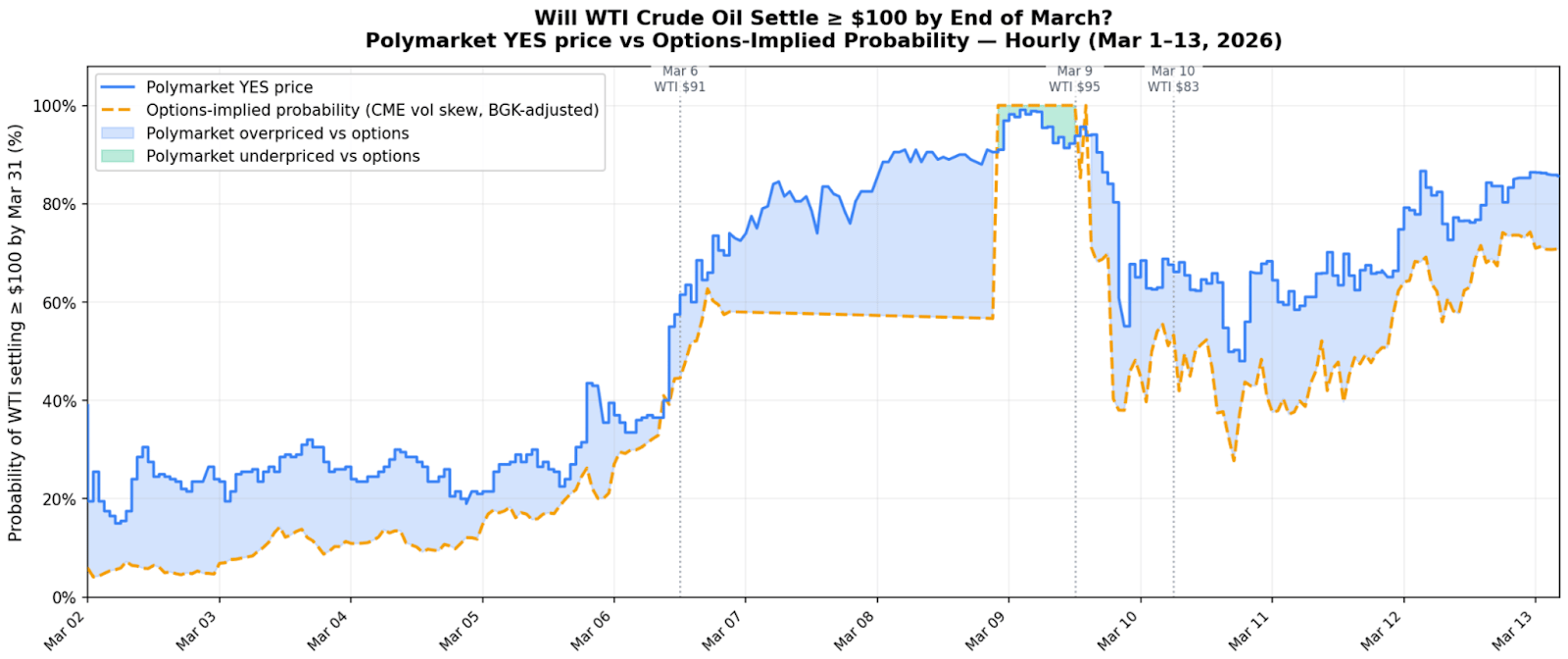

One notable new market is tied to crude oil, where traders can bet on whether WTI will reach certain price levels before the end of the month. Despite launching only in 2026, the market has already generated $34.5 million in volume and offers a simplified way for traders to express views on energy markets during periods of geopolitical stress.

With geopolitical tensions pushing WTI crude toward $100, we compared two markets pricing the same event: Polymarket’s “Will WTI settle ≥ $100 by end of March?” against the probability implied by CME crude oil options. To make the comparison fair, we converted raw option prices into an equivalent touch probability using the same barrier structure Polymarket uses.

The results are striking. For most of March, Polymarket priced the event 10 to 30 percentage points higher than the options market. When WTI surged to $91, options markets repriced almost instantly, while Polymarket lagged before overshooting as momentum traders piled in. When oil later fell to $83, options markets quickly adjusted, while Polymarket held elevated probabilities for nearly two days.

One caveat that explains part of this divergence is Polymarket’s resolution method. The market tracks the active month WTI contract, which rolls from March to April during the window. If April trades above March as escalation risk builds, the $100 barrier becomes easier to reach, which would push the true options implied probability slightly closer to Polymarket’s odds.

That said, most of the gap likely comes down to liquidity. Large traders can express commodity views in size on venues like Hyperliquid, but Polymarket books remain relatively thin. A $1000 trade currently incurs about 0.8% slippage, which is high for commodity markets. If deeper liquidity arrives through market makers or internal liquidity programs, volumes could scale quickly, and probabilities may begin to converge with traditional derivatives markets.

— Kunal

Blockworks Research examines the structural case for Canton as the coordination layer for institutional tokenization. DTCC, Nasdaq, and Broadridge are already deploying live workflows across treasury tokenization, repo financing, and collateral management, with Canton's architecture offering granular transaction privacy and cross-application interoperability that public and private chains individually cannot.

Weekly CC burn has increased 216% since TGE, with the burn-to-mint ratio at 0.90, approaching potential deflation. Canton generated the highest REV among major L1s in February at $74.7M yet trades at a discount, likely because the market prices it as financial infrastructure rather than a general-purpose chain.

Tushar Jain, Shayon Sengupta and Spencer Applebaum from Multicoin Capital join Lightspeed to lay out their updated crypto-investment thesis. The core argument centers on stablecoin-driven fintech as the next major adoption vector, with DeFi protocols serving as backend infrastructure for traditional-facing applications, what they call the “DeFi Mullet” model.

The conversation covers credible neutrality as a key blockchain design property, where Multicoin is actively deploying capital, and why the current market drawdown is a cyclical rebirth rather than a structural breakdown.

Josh argues that banking is being unbundled again, but this time at a deeper layer than the fintech wave that mostly changed distribution and user experience.

He sees stablecoins tokenization and smart contracts as the real shift because they let monetary assets and credit move on programmable rails, rather than through slow bank ledgers and batch settlement systems. That opens the door to more specialized financial products, more modular balance sheets, and a broader marketplace for lending and capital formation.

He also argues that AI agents will become key operators of this new stack, continuously routing and optimizing finance, while the biggest long term winners are likely to be the rail owners and the platforms that aggregate the user relationship at the top.

DAS NYC's lineup is bringing the biggest names in finance to the stage.

Don't miss the institutional gathering of the year — this March 24−26.