- 0xResearch

- Posts

- 💥 3 key 2024 onchain trends

💥 3 key 2024 onchain trends

Explosive growth, super users and quality challenges

Brought to you by:

As 2024 draws to a close, Flipside Crypto marked significant milestones in onchain user activity in its annual report released today. We took an early look. Plus, the Aave and Morpho feud has spread to Polygon governance choices.

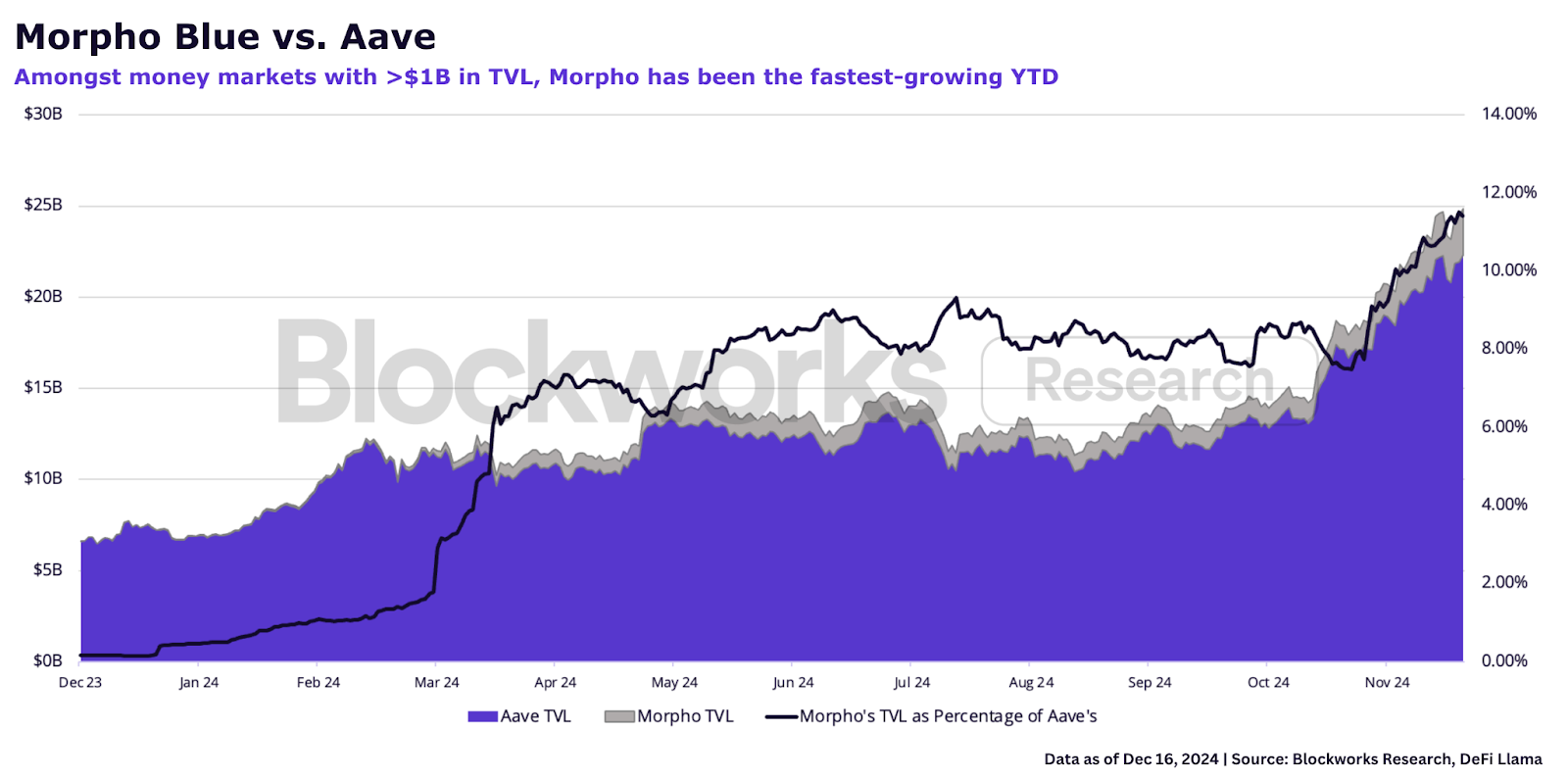

Borrow / lend heavyweights:

Morpho is the most credible competitor to Aave in the EVM ecosystem. Morpho Blue’s TVL has seen a 200x growth from $11m to $2.55b year to date. In contrast, Aave grew a little over 3x over the same period. This is expected given Morpho’s early stage in its lifecycle, but still a remarkable feat in the span of 12 months.

Morpho’s fast growth is thanks to its novel modular architecture, now adopted by Euler v2 and Kamino Lend v2. Multi-asset lending pools like Aave — deemed “monolithic lending platforms” — enable great UX and have a unified liquidity market, but they sacrifice capital efficiency and force all users into a one-size-fits-all profile, regardless of their risk appetite.

In contrast, modular lending platforms combine a base layer primitive with high flexibility in market creation with abstraction layers on top that handle complexities to improve UX for a wide range of users. Morpho has two core layers:

Primitive layer (Morpho Blue): Infrastructure for permissionless market deployment that is flexible, ungoverned and immutable.

Modular layer (lending vaults, public allocator): Built on top of the primitive layer, this specializes in UX and risk management, aggregating liquidity across markets.

Morpho’s approach contrasts to that of Aave, where risk management for new deployments is governed by the DAO, leading to reliance on centralized entities like the ACI. While Aave’s approach has enabled the protocol to grow securely over the years and dominate the lending landscape, it can inhibit open competition.

The Polygon bridge controversy this week is just the most recent example (more on this below). For instance, in April, Marc Zeller proposed to offboard DAI from Aave after Maker’s (now Sky) D3M allocated 500 million DAI to Ethena’s USDe, and sUSDe markets paired with DAI — a strategy that was carried out via Morpho’s infrastructure.

— Carlos Gonzalez Campo (X: 0xcarlosg)

Key trends from 2024

Focusing on EVM chains, the Flipside’s Onchain Users Report tracked both record growth and emerging challenges in maintaining engagement quality. Here are a few trends to watch in 2025.

Record user growth

Newly acquired users reached a record 19.4 million in October, with Base contributing 13.7m — “almost 8x the runner-up, Polygon,” the report notes. This explosive growth was attributed to Coinbase’s vast user base and Base’s focus on “trending sectors like memecoin trading and onchain AI via new initiatives like Based Agents.”

An “acquired user” is defined as a user who has conducted at least two transactions in 2024.

Ethereum also saw consistent user growth, averaging 1.56m new users monthly. Arbitrum peaked in May with 3.3m acquired users, fueled by GameFi and SocialFi.

Bitcoin usership, however, remained relatively flat despite BTC reaching its historic $100k milestone. This reflects speculative activity rather than meaningful onboarding.

Superusers: Base and Polygon dominate

Flipside terms “superuser” as those who executed 100 or more transactions on a chain, at any point.

Base led the way here with 15.1m wallets executing 100+ transactions, 38% more than Ethereum’s 10.7m superusers. Meanwhile, Polygon recorded 1.5m new superusers in 2024, underscoring its strength outside of DeFi. According to the report, “Polygon’s superuser activity also surpassed that of every other observed chain, with 867.7m monthly super-user transactions.”

Ethereum retained its position as the DeFi hub with 10.9m DeFi-related superusers, more than Arbitrum and Optimism combined.

Blast’s surge and sharp decline

Among newly launched chains, Blast made headlines with a record single-month peak of 134.9k acquired users in June. This was driven by its ability to incentivize “a wide range of gamified onchain activities.”

However, the chain experienced a significant user drop-off in Q4. Despite the evident exodus of points farmers from the chain, the report highlights Blast’s upside potential: “The remaining users are still active on multiple fronts, suggesting that the chain has the potential to outlive, and exceed, its initial hype.”

Uniswap’s DeFi dominance

Uniswap solidified its dominance, capturing 91.3% of DEX activity on Base and increasing its share on Ethereum by 27.72% compared to 2023. This points to a broader trend, “a ‘winner-takes-most’ DeFi market [that] disproportionately favors larger incumbent players with deeper liquidity and brand familiarity,” the authors said.

Meanwhile, LFJ (née Trader Joe) retained its lead on Avalanche, growing its market share by just over 6% from 2023, thanks to innovations like Auto-Pools.

The challenge

While 2024 saw record user acquisition, Flipside emphasizes the need for quality engagement. As the report notes: “Behind the headlines of record user growth lies a deeper challenge: building ecosystems that create meaningful, lasting engagement, not just fleeting speculation.”

For instance, despite Base attracting massive numbers of users, the report underscores the “narrow range of onchain actions its new user base is currently engaged in,” such as simply gambling on a memecoin or two. It’s not clear whether apps can execute on the opportunity to redirect users toward deeper activities like DeFi.

Brought to you by:

SKALE, the gas-free invisible blockchain, is “Built Different” for mass adoption: high-throughput, scalable, and fair. As a network of interoperable EVM-compatible L1s, SKALE’s user experience focus has accelerated a strong ecosystem across gaming, AI, and more. Due to SKALE’s gas-free nature, blockchain can be integrated invisibly, creating accessible Web2-like experiences for users and developers.

SKALE has:

Over 50M UAWs

9 Games on the Epic Games Store

Saved Users over $9.5B on Gas Fees

Polygon vs. Aave

What began as an early stage governance proposal is now a full-blown public spat between project figureheads.

Last week, Polygon governance floated a proposal to invest $1.3 billion idle stablecoin capital from the Polygon PoS bridge into Morpho’s lending vaults. A few days later, Marc Zeller of the Aave-chan Initiative proposed to effectively offboard Aave from the Polygon chain, citing risk vulnerabilities with the bridge.

In response, Polygon co-founder Sandeep Nailwal today accused Polygon of “extremely monopolistic and anti-competitive behaviour” and criticized Aave’s seeming hypocrisy for previously showing enthusiasm and “lobbying heavily” in the early stages of Polygon’s plans to invest bridged funds. Nailwal suggested that Aave’s reaction was one of “sour grapes” in response to the selection of their competitor (Morpho) over them.

Polygon CEO Marc Boiron went one step further to point out Aave’s governance was “captured.” Boiron then praised Morpho’s product as being superior to Aave, with “fewer attack vectors,” and its isolated lending pool model that boasts “significantly greater capital efficiency” than Aave’s pooled liquidity model.

Aave’s Stani Kulechov fired back hours later with two key points. Firstly, Aave’s infrastructure would’ve allowed Polygon to create an isolated lending market, akin to Morpho’s model. Second, contrary to Boiron’s point, Aave’s decisions were primarily motivated by the concerns of “inheriting the risk of a third party protocol” rather than being anti-competitive.

— Donovan Choy (X: @donovanchoy | Farcaster: @donovan)

dYdX has long been at the forefront of DeFi as one of the primary innovators of onchain perpetual futures.

With the launch of dYdX Unlimited on Nov. 19, 2024, the protocol has brought new functionality to the platform that aims to diversify their product suite.

Relative valuation metrics suggest dYdX could be undervalued compared to market leaders, analyst Daniel Shapiro writes in the most recent Blockworks Research report. This indicates that the market is not yet fully appreciating the impact of these recent developments.

Tether has invested in StablR to accelerate European stablecoin adoption. StablR’s MiCA-compliant EURR and USDR launched with a focus on liquidity and compliance. Using Tether’s Hadron platform, StablR plans to expand network compatibility, providing scalable and interoperable solutions for institutions and merchants.

Plume announced a $20m Series A fundraise today backed by Brevan Howard Digital, Haun Ventures, and others to advance its layer-1 "RWAfi" blockchain. Plume facilitates onchain tokenization and trading of real-world assets. The nascent Plume ecosystem touts more than 180 teams building on its testnet chain as of today.

ENS Labs and Linea Association are partnering to launch Namechain, a custom version of Linea's zkEVM solution, addressing the scaling needs of the Ethereum Name Service. Namechain will bring ENS identity services faster transactions, cost efficiency and decentralization, starting in 2025.

Ink, an Optimism Superchain-based layer-2 from Kraken, has launched its mainnet early, the team announced today. The platform enables token bridging, liquid staking and lending, with plans for permissionless fault proofs in 2025. Backed by a growing developer community, Ink is the latest L2 aiming to improve accessibility and scalability for Ethereum.