- 0xResearch

- Posts

- 15-minute markets

GM, and happy Monday!

Today we unpack what’s actually driving volume in prediction markets, and why short-duration contracts are starting to look more like microstructure products than directional bets.

We also zoom out to assess the macro backdrop and the broader capital cycle, which are shaping risk appetite across crypto and equities.

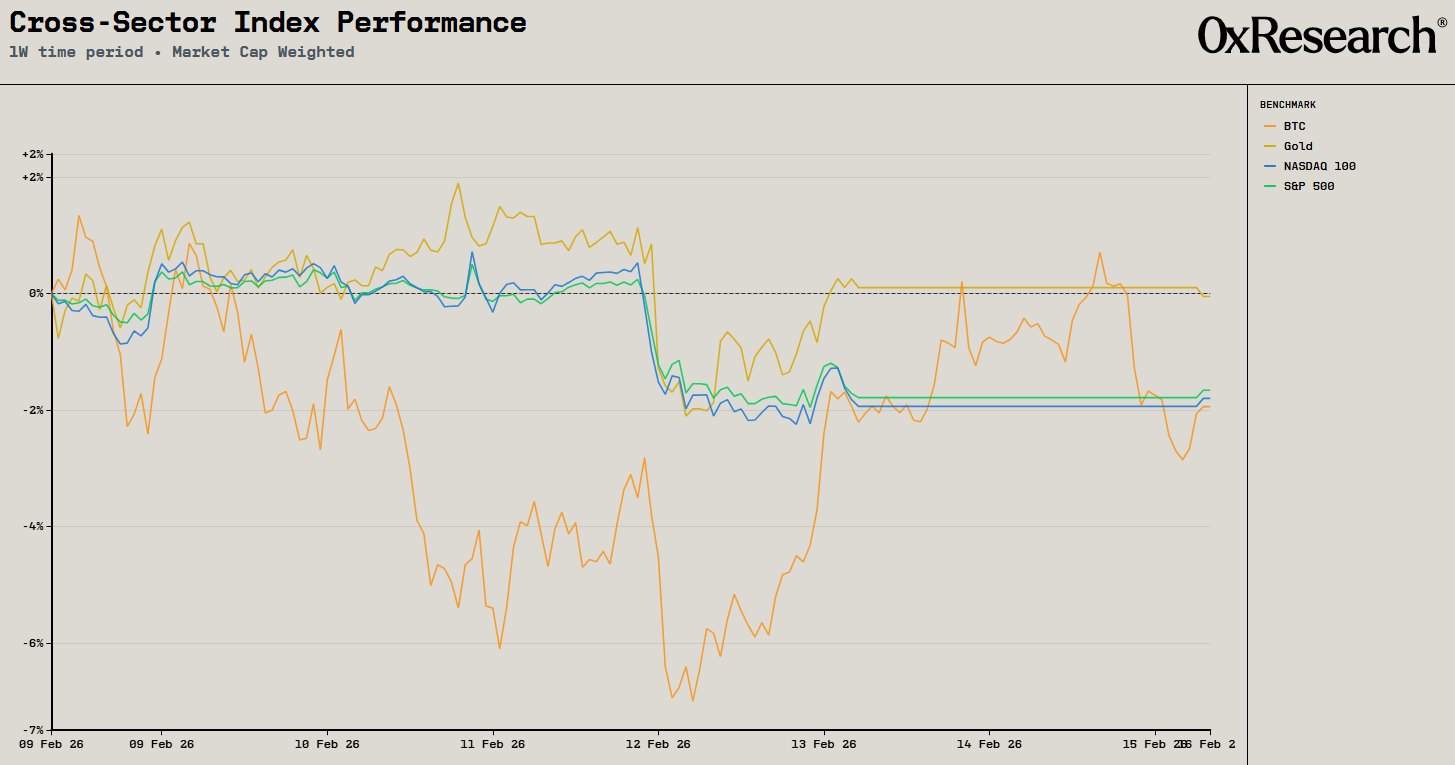

Another tough week for risk assets, with all major benchmarks finishing in the red. Gold slipped just −0.05%, while the S&P 500 fell −1.7%, the Nasdaq declined −1.80%, and BTC dropped −1.9% on the week.

Macro data sent mixed signals. CPI came in lower than expected, suggesting inflation remains contained for now, while nonfarm payrolls beat consensus by a wide margin, pointing to a resilient labor market. That strength has dampened rate-cut expectations. The odds of no cut in March rose from 82% to 92%, while the probability of no cut in April climbed from 66% to 70%. A stronger economy means the Fed has less urgency to ease.

Beyond rates, broader risk sentiment has been weighed down by rising anxiety around AI disruption. What began as a selloff in software names has now spilled into financial brokerages, real estate services, insurance, and even trucking and logistics. The market appears to be in “sell first, reassess later” mode.

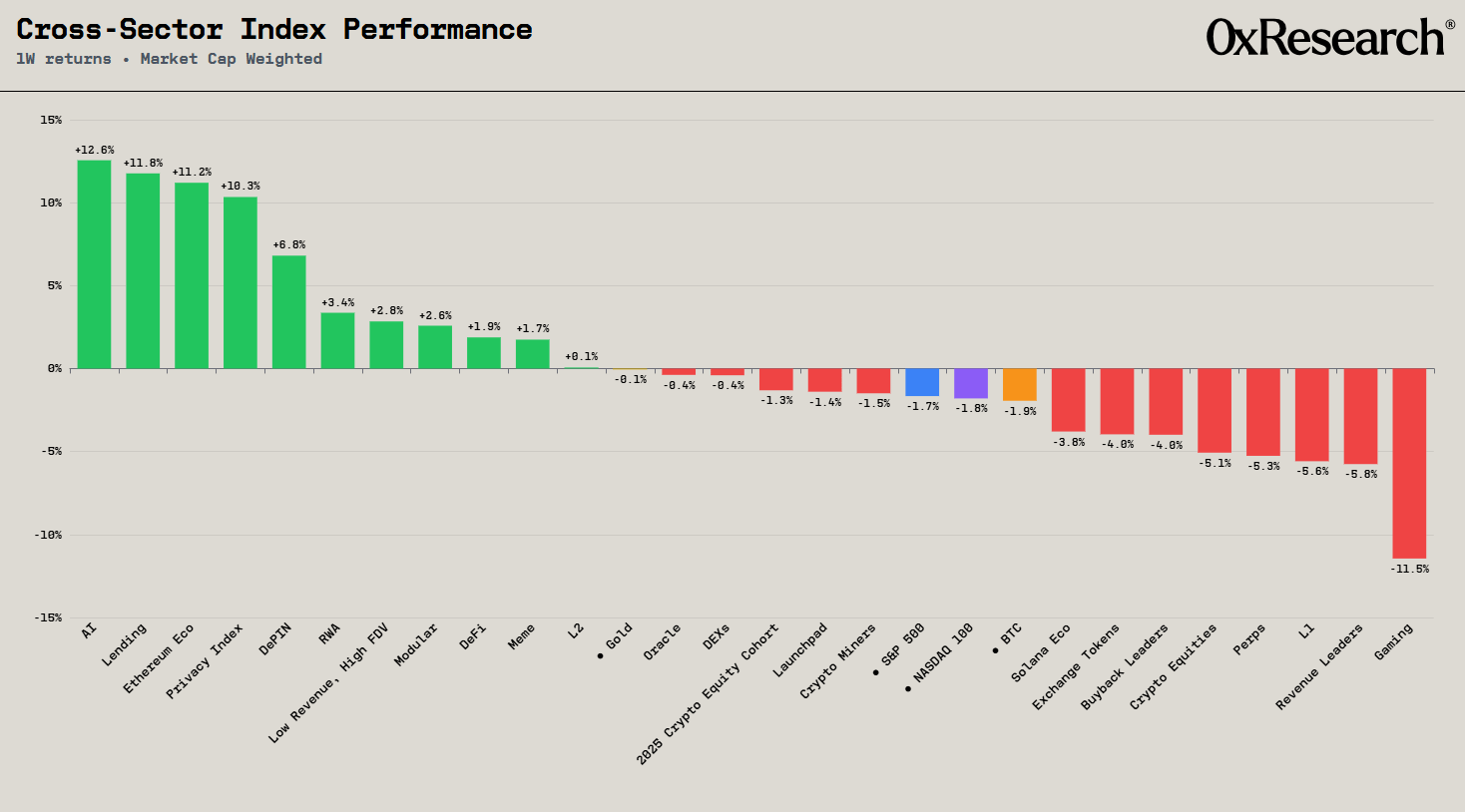

In crypto, performance was more nuanced. The standout sectors were AI and Lending, up 12.6% and 11.8% on the week. AI strength was broad-based, with TAO and VIRTUAL leading at 12.8% and 9.8% respectively. Interestingly, developers are now wiring OpenClaw AI agents to mine Bittensor subnets, allocate stake, and query network stake. The company Virtuals continues to roll out updates aimed at attracting more and higher-quality agents to its Agents Commerce Protocol ACP. Last week, the team introduced a new revenue-incentive program that will allocate up to $1 million per month to agents generating real economic value. This marks a clear shift away from a purely trading-driven fee model toward rewarding actual revenue creation within the agent ecosystem.

Lending was driven by AAVE and Morpho, which gained 11.7% and 15.4%. AAVE rallied following the announcement of the Aave Will Win Framework, which directs 100% of product revenue to the DAO. Morpho benefited from Apollo Global Management’s agreement to purchase up to 90 million tokens over four years to support lending markets built on its infrastructure.

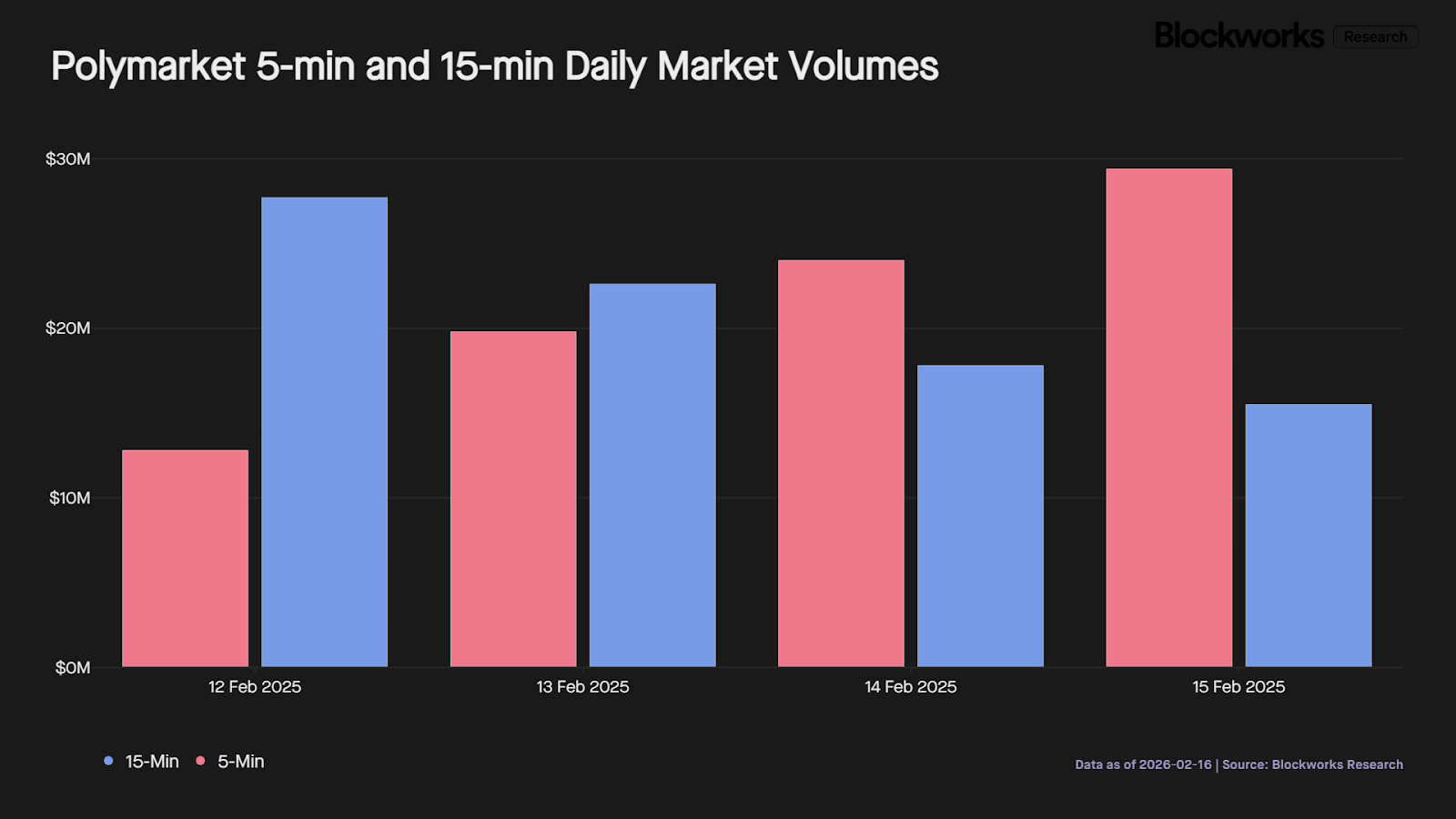

Outside price action, prediction markets continue to heat up. Polymarket’s new five-minute BTC up/down markets have already generated $86 million in volume within just four days, surpassing their 15-minute equivalents. Fast resolution markets are clearly resonating.

— Kunal

DAS NYC's lineup is bringing the biggest names in finance to the stage.

Don't miss the institutional gathering of the year — this March 24−26.

Polymarket’s edge, Kalshi’s opportunity

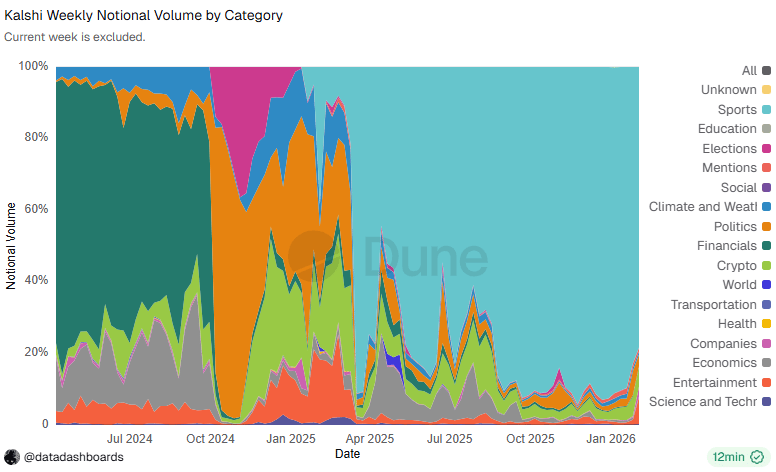

While Kalshi and Polymarket are now running at similar weekly volumes, their volume profiles differ significantly.

Kalshi remains heavily concentrated in sports, which drives roughly 80 to 90 percent of weekly volume. Crypto contributes just 3 to 5 percent. That vertical dominance is real, but so is distribution concentration. An estimated ~50 percent of Kalshi’s volume flows through Robinhood. With Robinhood’s prediction-market revenue up 3.8x quarter-over-quarter in Q4 and now ~8.5 percent of total revenue, the incentive to internalize that flow over time is obvious. When distribution sits upstream, platform risk increases.

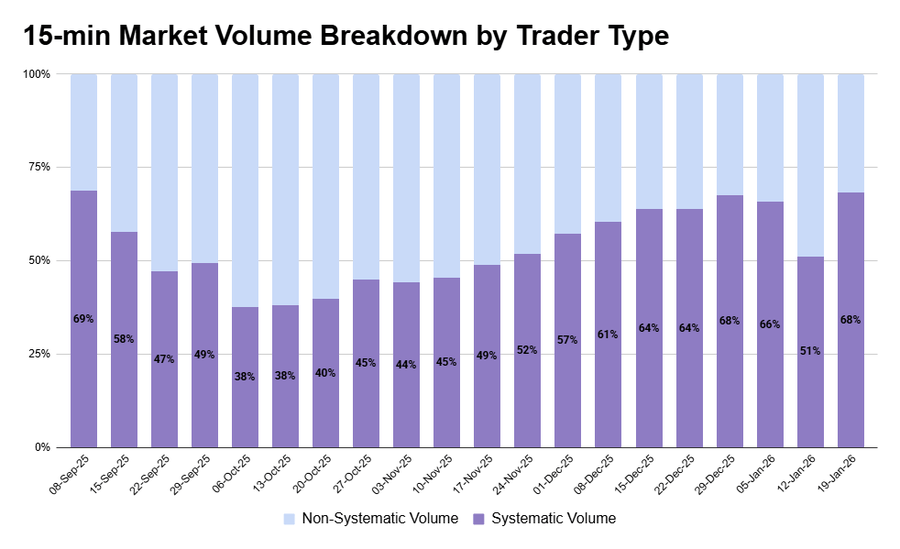

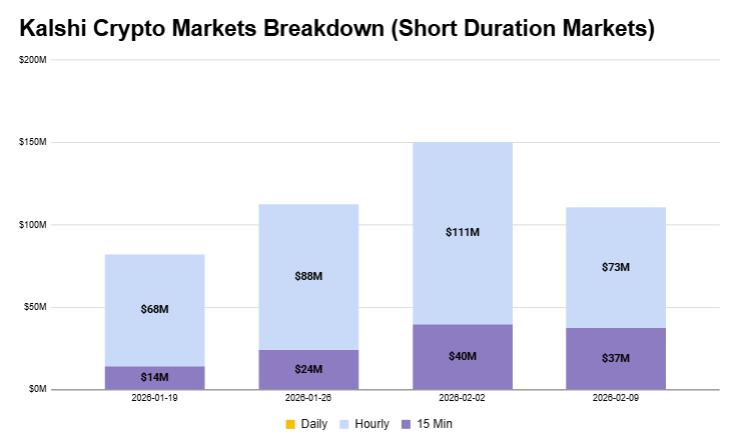

Polymarket’s mix is more diversified, spread across sports, politics and crypto. Crypto has grown from roughly 5 percent of weekly volume at the start of 2025 to nearly 30 percent today. Inside crypto, one product now dominates: 15-minute up/down markets. These have expanded from ~5 percent of crypto volume to roughly 60 percent in early 2026, far outpacing hourly or premarket contracts.

Interestingly, trading behavior shows systematic participation rather than retail conviction. A meaningful share of addresses repeatedly buy both YES and NO within the same 15-minute window, often dozens or hundreds of times. Roughly 8 percent of these addresses account for up to 70 percent of 15-minute volume. More than half of YES/NO pairs execute below $1 combined, with a median around $0.988, producing consistent arbitrage spreads. Since September, this cohort has generated ~$16 million in net PnL.

Importantly, these traders are not pure takers. A large share post meaningful maker volume, contributing to tighter spreads and improving displayed depth. Over time, maker participation has become more symmetric, reducing one-sided order book imbalances.

The deeper structural driver appears to be supply injection. A single address accounts for over half of 15-minute volume and is a 100 percent taker that predominantly sells. Its execution profile is consistent with mint-and-distribute behavior: Deposit collateral, mint YES and NO, immediately sell into bids. That mechanism seeds inventory, enabling arbitrageurs to recycle capital at scale.

The result is reflexive: More supply enables more arbitrage, which tightens pricing, increases turnover, and attracts further volume.

Kalshi has launched similar short-duration contracts and is seeing early uptake. The demand signal exists — the open question is whether replicating format is sufficient, or whether liquidity architecture, inventory design, and microstructure engineering are the real competitive moat.

In short, 15-minute markets are less about prediction and more about market design. Understanding who is supplying inventory and how arbitrage capital recycles is key. Kunal breaks down the wallet-level dynamics and PnL flows in his X thread.

— Shaunda

This proposal argues that Aave should double down on alignment and allocate $50 million per year to expand into fintech, targeting a multitrillion-dollar market where customer funds in Europe alone dwarf current DeFi TVL.

With loans growing rapidly and acquisition costs in traditional fintech already high, the budget is framed as competitive and sustainable given Aave’s revenue trajectory and treasury runway. The real edge is not competing on simple yield but leveraging composability — such as borrowing against tokenized stocks — to unlock use cases traditional banks cannot offer.

While concerns remain around transparency and treasury concentration, the strategic bet is that reinvesting in growth over buybacks positions Aave to capture long-term fintech scale rather than remain a backend protocol.

Stani Kulechov lays out a long-horizon thesis: The next multi-trillion-dollar opportunity for Aave is not tokenizing existing financial assets, but financing “abundance” technologies, starting with solar and battery infrastructure.

He frames finance as the historical catalyst behind major economic transformations and argues that the coming energy transition, potentially requiring $15−50 trillion in capital through 2050, is structurally a better fit for onchain lending than traditional scarcity-based assets like sovereign debt or real estate. With solar costs down ~99% since the 1970s and global annual investment already above $600 billion across solar and storage, the bottleneck is no longer technology but scalable capital formation.

The proposal is to tokenize solar equity and project debt, use it as collateral within Aave, and create liquid, stablecoin-denominated yield tied to real-world productive assets. If even a small share of global bond capital migrates onchain, Aave’s collateral base could expand into the trillions, positioning the protocol as a financing layer for energy infrastructure rather than just crypto leverage.

Raydium’s Q4 2025 reflected Solana’s broader cooldown, with net revenue down 73% quarter-over-quarter to $7.3 million, and volume falling 53% to $24.5 billion, largely due to memecoin contraction.

Despite this, margins held at 91%, infrastructure costs fell 66%, and ~80% of operating cash flow was allocated to buybacks and treasury, reinforcing capital discipline. CLMM proved structurally resilient (−26% QoQ) and now drives 58% of swap revenue, while Raydium maintained leadership in AI agent tokens (92% share) and tokenized assets ($206 million volume, 54% share).

With $126.4 million in treasury assets and the launch of Raydium Perps — plus renewed LaunchLab momentum via Winner’s Arc — the 2026 focus shifts to revenue smoothing and diversification beyond spot-driven cycles.